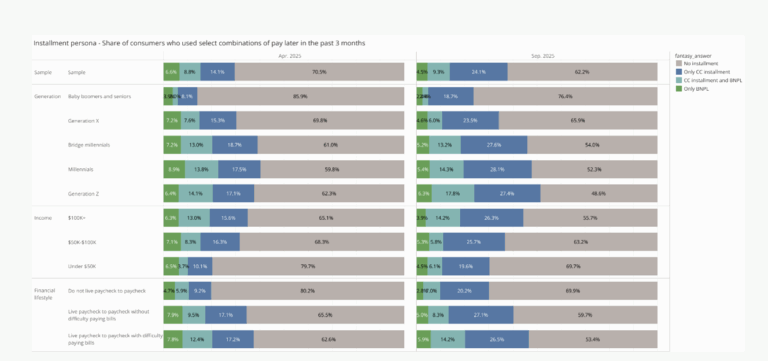

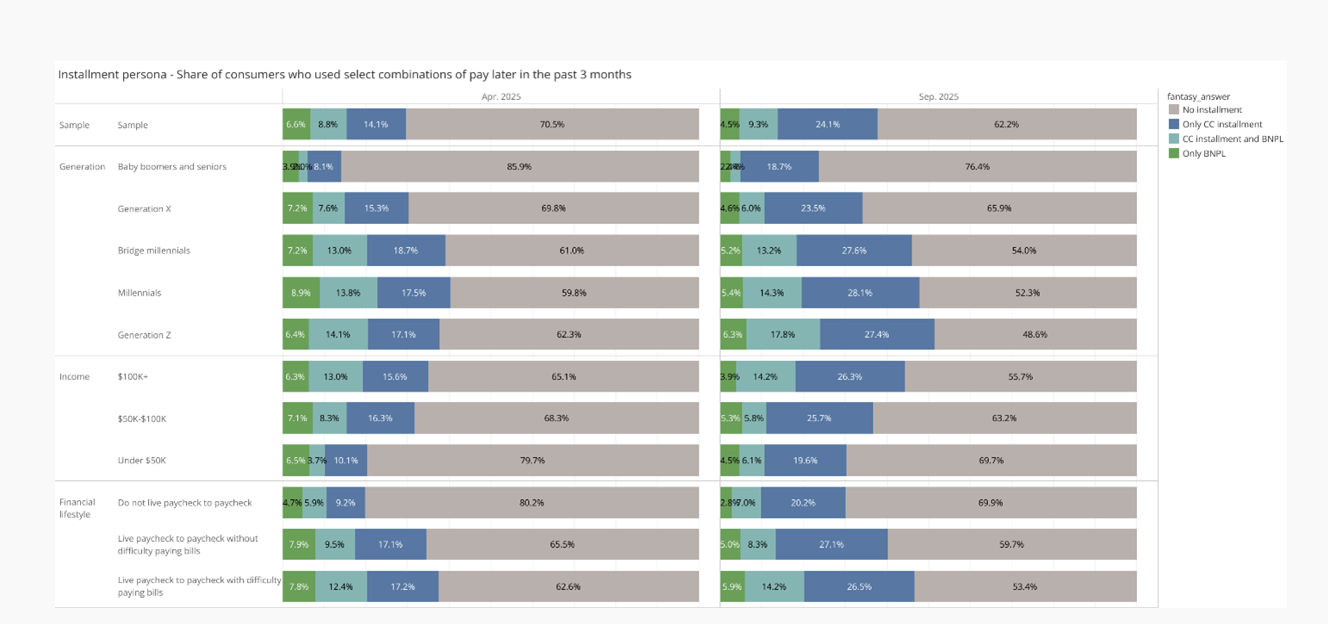

BOSTON–Younger consumers are leading the shift toward installment and BNPL options, with Gen Z and Millennials driving hybrid usage of credit card installments and pay-later plans, according to a new analysis.

“Financing options sway where consumers shop — particularly for experiences, services and big-ticket retail categories,” PYMNTS Intelligence said in a releasing the report. “BNPL’s ease of approval and budget-friendly structure positions it as a go-to payment option heading into the holiday season.”

The PYMNTS Intelligence report reveals installment programs have become commonplace, large segments of consumers still haven’t tried them as offered through BNPL options, suggesting considerable greenfield potential.

PYMNTS Intelligence said its “Installment Persona” data comparing April and September 2025 reveals meaningful growth in pay-later adoption.

The Findings

Among the findings:

- The share of consumers who reported using some form of pay-later option in the past three months climbed from 29.5% in April to 37.8% in September.

- Among Generation Z, only BNPL usage stood at 6.4%, while credit card use rose to 27.4%, up from 17.1% earlier in the year.

- Income also shapes behavior: 45% of Gen Z and 42% of millennials used installments, while 70% of households under $50,000 still avoided them entirely.

Budgeting & Liquidity Tool

“These trends underscore how younger consumers view BNPL as a budgeting and liquidity tool rather than a last-resort credit product, and they highlight the gradual normalization of pay-later methods within everyday financial routines,” PYMNTS Intelligence stated.

BNPL and Paycheck-to-Paycheck Consumers

According to PYMNTS Intelligence, the generational divide is further amplified by consumers’ broader financial realities. The company noted its research underscores that paycheck-to-paycheck households are among BNPL’s most active users, often turning to installments as a cash flow management tool rather than a borrowing mechanism.

According to PYMNTS Intelligence’s “How Struggling Consumers Use BNPL” report, 75% of consumers living paycheck to paycheck have used a pay-later plan through 2023-2024 across income levels, while those facing bill-payment difficulties are roughly four times more likely to use BNPL than their financially stable peers, the company pointed out.

It further noted a separate study, “Cash Flow Shortages Drive Consumers’ BNPL Usage,” found that cash-short consumers are 3.5 times more likely to rely on BNPL to navigate periods between paychecks.

“Together, these insights highlight BNPL’s growing role as a mainstream budgeting mechanism, especially for younger adults who are already predisposed to digital payments and installment tools,” PYMNTS said.

Financing Options and Store Choice

Data from PYMNTS Intelligence’s “Impact of Financing Option Availability on Store Choice” shows that the presence of flexible payment options strongly shapes where people shop, especially for discretionary or higher-value purchases, the company explained.

PYMNTS Intelligence further stated:

- Roughly 40% of consumers said financing options were “very or extremely influential” in choosing where to spend on events, travel, home services, and even grocery or food-delivery categories. The effect is particularly pronounced for events and experiences (40.3%) and food delivery (43.6%), where short-term financing enables more spontaneous spending, the company said.

- By contrast, everyday obligations such as utility bills (23.6%) and medical payments (26.5%) ranked lower in influence — yet even there, nearly one-in-five consumers said the availability of installments factored highly into their provider choice.

“The data suggests that as consumers grow accustomed to seeing BNPL options at checkout, the absence of financing can become a competitive disadvantage for merchants, particularly in discretionary categories where purchase decisions hinge on flexibility,” PYMNTS Intelligence said.

BNPL Aligns With Spending Motivations

PYMNTS Intelligence further said its companion data on payment methods matched with spending categories provides further insight into why consumers are adopting BNPL.

When asked which payment type best fits various scenarios, 21.7% cited BNPL as the “easiest to apply for,” compared with 14.7% for credit card installments. BNPL also scored high on approval likelihood, with 20.7% calling it “most likely to be approved,” PYMNTS Intelligence reported.

“Although traditional credit cards still dominate for rewards and larger transactions, BNPL appeals for its immediacy and accessibility,” PYMNTS Intelligence stated. “Nearly 17% said BNPL was ‘best for larger amounts’ over $3,000, and 13.8% favored it for smaller sub-$100 purchases — a sign that consumers are using the product across price tiers, not solely for big-ticket items.”

Positioned for Holiday Season

“Together, these data points outline a clear trajectory: BNPL has become an embedded part of how consumers manage spending,” the analysis continued. “Younger users are adopting hybrid installment behaviors that bridge credit cards and BNPL platforms, while merchants see measurable influence from financing availability on shopper conversion.”