POIPU, Kauai–When it comes to driving growth at a credit union, it really all comes down to two things, according to one person, who also advised that removing a question from the digital sign-up process may pay dividends, while cautioning that one bias by board members may be preventing the CU from serving what can be a profitable market.

Speaking to Rochdale’s Volunteer Leadership Institute (VLI), Sam Brownell, CEO of CUCollaborate, used analysis of NCUA 5300 data to stress his point that spending money on marketing “is the biggest lever you can pull.”

It’s an investment he said credit unions must make.

“The reason for growth is it is a categorial imperative,” Brownell said. “Credit unions solve meaningful problems for people in meaningful ways, and I think its important that we extend that benefit to as many people as possible.”

But extending that benefit is challenging when most credit unions underinvest in marketing “almost as a rule of thumb,” he added.

It Pays to Pay, Although Not as Much

“The other driver of growth is higher deposit rates, but it is substantially less significant than spending on marketing,” said Brownell, who focused on both themes throughout his remarks.

He added that ROA, while often a focus of CUs, is not really correlated the growth, while cost-cutting is also an ineffective strategy for growing.

While solving problems for consumers is the ideal, there is a critical step that must come first before anyone can have their problems resolved, Brownell explained. “You need to tell people you exist,” he said.

‘It’s the Benefit, Stupid’

That is a step he defined as “It’s the benefit, stupid.”

“Credit unions exist to do better than banks. Now apply it. Really focus on delivering better loan and deposit rates,” Brownell told the meeting.

And while many CUs like to lean into their history or legacy, Brownell observed that “Your historical roots are nice, but non-members are the future.”

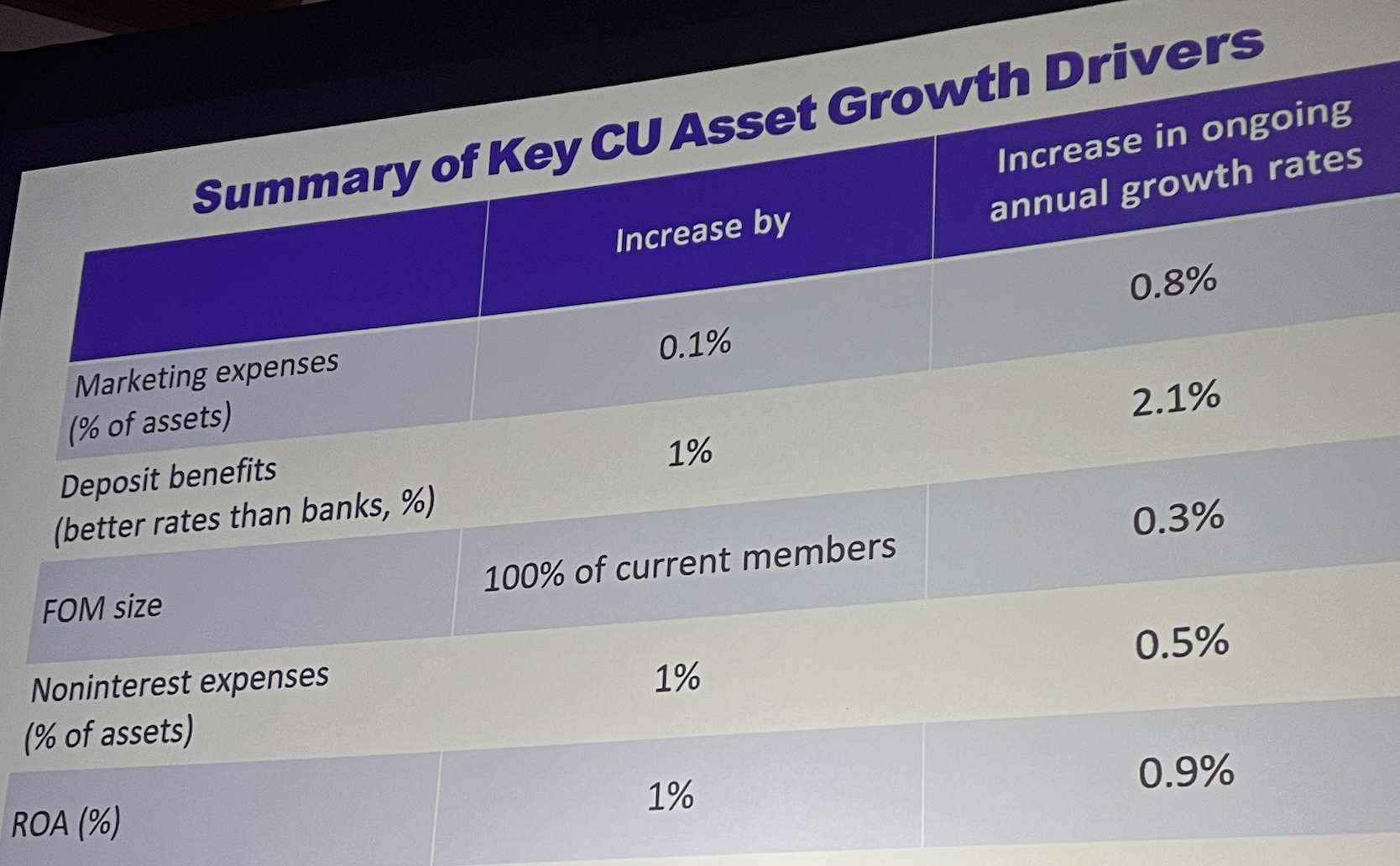

It all keeps coming back to investment in marketing, Brownell said, sharing the chart that is shown below.

“Business development and marketing are consistently very effective avenues for credit unions of all sizes,” he said.

Sustainable New Member Acquisition

One area in which credit unions are losing ground, Brownell told the meeting, is in gaining membership among younger generations, which has long-term implications. While the industry’s proportion of U.S. primary banking relationships has held steady, the share of new account openings has declined, he said. The reasons are not surprising.

“Digital convenience is critical to capture your younger members,” he said.

But members of any age aren’t likely to join a credit union if they don’t know they can do so, he said, citing research showing 40% of consumers don’t believe they are eligible to join a single credit union.

“This is a huge headwind,” Brownell observed. “Every consumer is eligible to join at least eight credit unions based on where they live and work. We are doing ourselves a disservice by not educating people.”

The Effect of One Big CU’s Advertising

Slightly complicating that perception, he suggested, is all of the national advertising by Navy Federal Credit Union that discusses its closed membership, which Brownell said helps to “perpetuate” some of these issues.

“And if you try to join a CU and are unsuccessful, why try to join another?” he asked.

It’s the question of membership eligibility that also gums up online membership sign-ups, according to Brownell, who noted that 84% of abandoned applications drop off on the FOM validation step when people are asked “how are you eligible to join?”

“It feels impolite to not put this at the beginning of the application and to put it at end, where they may find they are not eligible to join,” he said. “The amount of people who can’t figure out how they’re eligible is really high. I would encourage you to remove this step from the digital application and have your own staff figure out how this person is eligible on the backend. This is what makes the member acquisition cost for credit unions materially more than banks.”

The Other Growth Driver

Speaking to the second growth driver, deposit pricing, Brownell said the rates available from credit unions are an “advantage.” That’s especially true with certain markets, he stated.

“The monetary value credit unions offer to people with prime credit is much less than the value to people with subprime credit,” he said. “Credit unions that effectively lend to subprime borrowers actually make more money on it. Generally, credit unions have boards made up of people who are prime borrowers and who are uncomfortable with the idea of charging higher interest rates to lower tiers of credit, but you need to do because it has to make sense.

“The greater the financial benefit the longer the retention,” he continued. “A lot of the credit unions that struggle with retention are serving prime borrowers who are savvy rate shoppers. That’s how they found the credit union.”

An Oldie But a Goody

According to Brownell, many of the most successful and growing credit unions have a strong strategy to serve select employee groups (SEGs), something that has become lost for many CUs as they moved to community charters.

“Ultimately, you have a partner who is there doing your marketing for you,” he said. “They do it because you are solving problems for their employees better than anyone else would.”

Brownell said the larger the SEG—ideally, more than 10,000 employees—the more effective.

Additional Notes on Growth

Brownell shared a number of other observations when it comes to driving growth, including:

What Gets Measured, Gets…

Brownell said credit union need to measure and quantify the job being done internally by the business development team. They are often not invested strongly enough in the credit union’s growth, according to Brownell

Retention, Retention, Retention

Key points in retention, according to Brownell, include:

- Active cross selling and focusing on convenience

- Machine learning, including lifecycle marketing, next best product and personalization

- Persistent preapprovals

- Competitive digital banking solutions

- Ask your members and mine your/their data.

Indirect Members

Many indirect members do not know they are members, he reminded.

Don’t Just Solve Problems, Solve Big Problems

Brownell advised CUs to make it really easy for people to understand you can solve problems for them and know what those problems are.

“If you’re solving a discreet problem there are only so many people with that discreet problem.”

Consider LICU and CDFI Designations

Brownell said all credit unions should consider low-income and Community Development Financial Institution (CDFI) designations, saying both outperform credit unions in general.

“I have heard of credit unions that have turned down the low-income designation because they were afraid their members would hear about it,” Brownell said. “But it’s not a public thing and it creates a lot of benefits.”

Brownell explained the LICU designation allows CUs the:

- Ability to accept non-member deposits up to the greater of $3 million or 50% of the total shares

- Exemption from compliance with the MBL cap of 12.25%

- Ability to apply for technical assistance grants and low-cost loans from NCUA’s CDRLF

- Ability to include subordinated debt in the net worth ratio calculation

- Expand members to others affiliated with the community. Such as people who perform volunteer services and participate in associations located in the community