NEW YORK–More than nine-million Americans could see “substantial declines” in their FICO scores in the months ahead as delinquent student loans begin showing up on credit reports for the first time since the pandemic, according to a new analysis by the Federal Reserve Bank of New York.

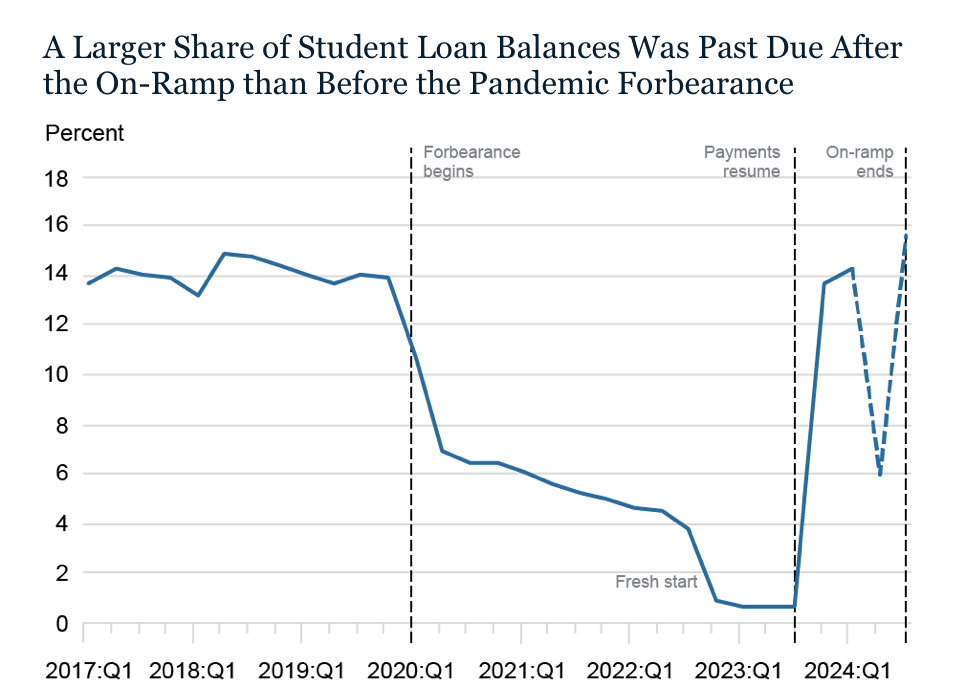

The Fed analysis has found that more than 15% of all student loan holders are likely now behind on debts, which is slightly higher than prior to the pandemic.

As the CU Daily has reported, borrowers have been required to make normal monthly payments on their student loans for well over a year, after the Biden administration ended the COVID-era pause on the program. Those borrowers temporarily benefitted, however, from a so-called “onboarding” phase, during which loan servicers were not allowed to report late or missed payments to credit agencies.

That grace period ended in September.

‘Rolling Window’

“Delinquencies will hit credit reports over a rolling window as borrowers with missed payments advance beyond 90 days past due,” the New York Fed said in its analysis. “As such, the 2025:Q1 Quarterly Report on Household Debt and Credit will likely reveal a significant uptick in the delinquency rate for student loans, but the size of this increase is difficult to pin down. In advance of this release, we attempt to estimate the scope of delinquent student loans at the end of the on-ramp by combining the most recent data (as of September 30, 2024) from Federal Student Aid (FSA) with data from the CCP from the same time.

The Fed Bank of New York added that is has estimated a “shadow delinquency rate” by summing the total volume of loans not owned by the federal government that were 30 or more days past due from the CCP with the total volume of loans 30 or more days delinquent from FSA in each quarter.

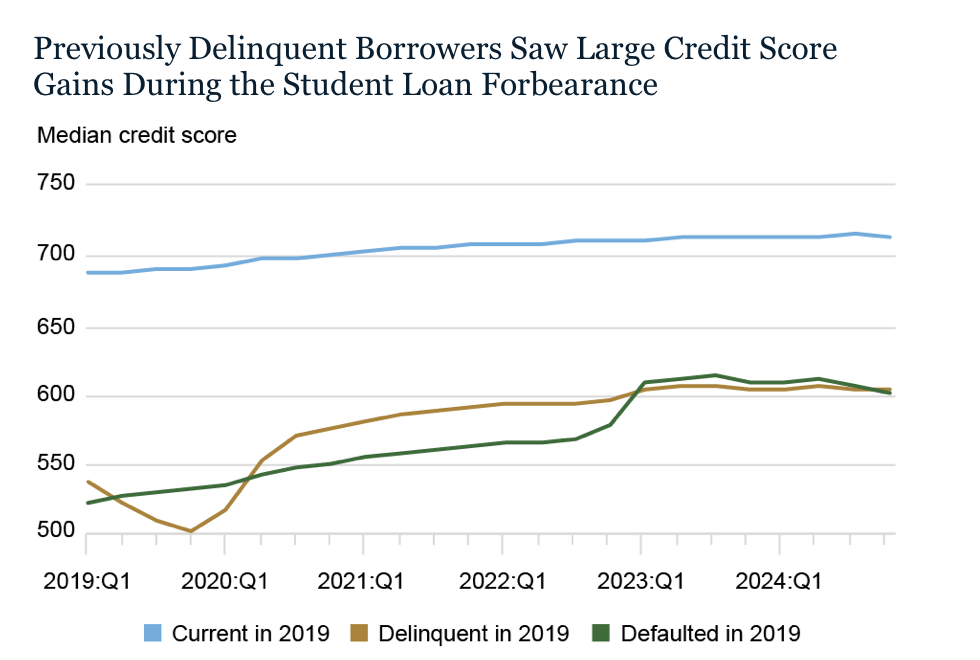

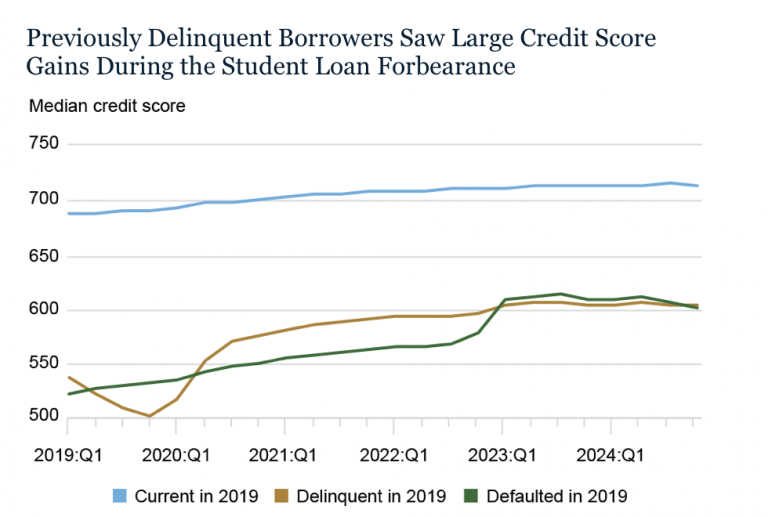

The New York Fed said its researchers found that a student loan delinquency can knock more than 150 points from the FICO score of someone with around average credit. For subprime borrowers — those with scores below 660 — it can subtract 87 points.

Confusion Reigns

In its analysis, Yahoo Finance noted that recent confusion around the state of the student loan program may not be helping matters.

“For the past month, for instance, the administration had blocked access to income-driven repayment plans, which cap what borrowers owe each month at a percentage of their earnings, in response to a court ruling, leaving many with fewer options to manage their debts,” Yahoo Finance stated.