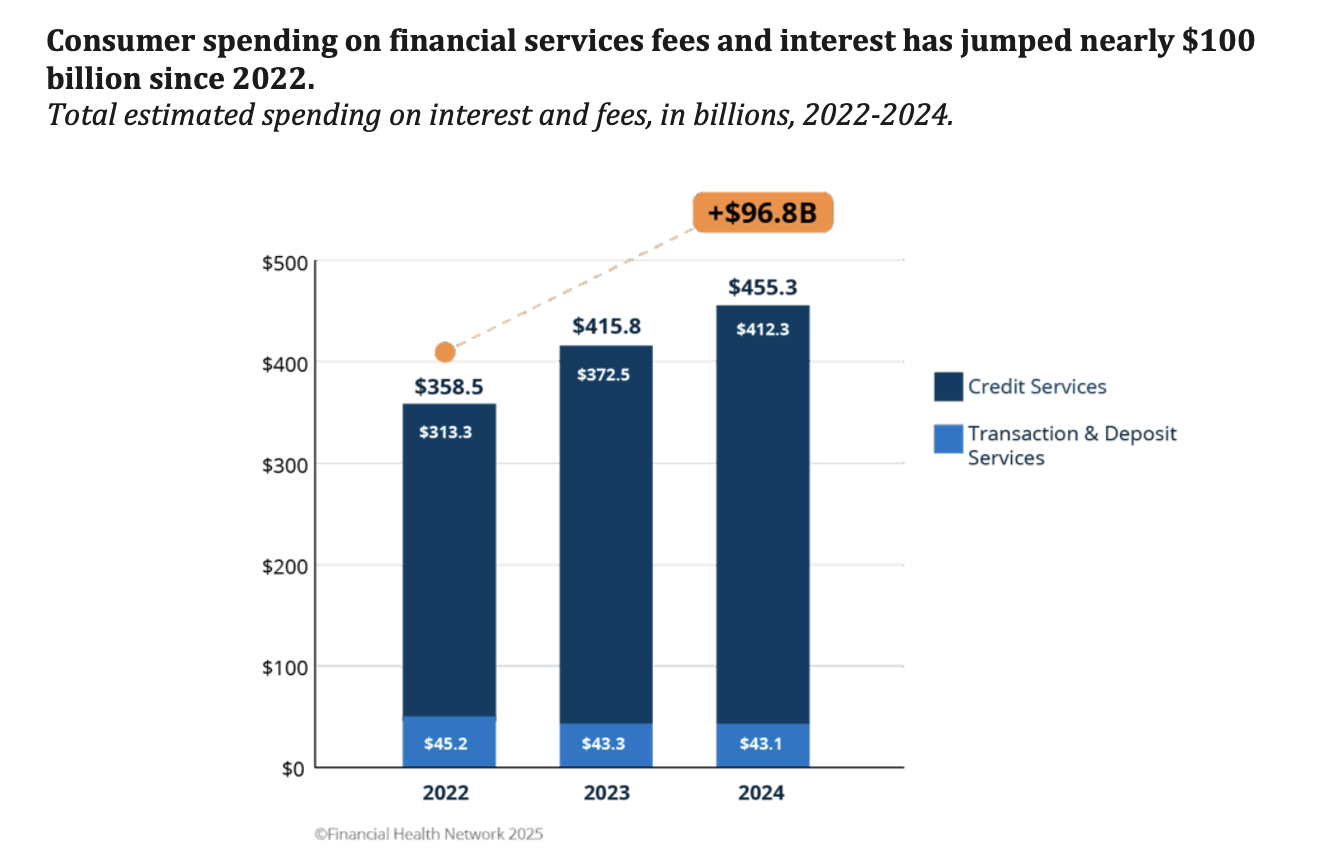

CHICAGO–New research reveals that Americans spent $455 billion in financial services fees and interest in 2024 as credit costs, student loans, and “deep inequities strain households,” according to a new report that offers some interesting insights across numerous financial products, including that overdrafters at credit unions reported higher frequency of fees than bank overdrafters.

As outlined below, the study breaks out financial services spending by credit cards, checking accounts/overdrafts, student loans, BNPL

According to the FinHealth Spend 2025 Report from the Financial Health Network, which conducted the research, that $455 billion is nearly $100 billion more than in 2022. Rising credit card balances and the return of student loan payments drove much of this increase, while overdraft fees ticked upward for the first time in years, according to Financial Health Network.

‘Bearing the Brunt’

“Disparities in financial services fees and interest also continued in 2024, with vulnerable populations – including households who are not Financially Healthy, Black and Latine households, and households without prime credit scores – bearing the brunt of these burdens,” the organization said. “At the same time, new data reveal shifts in bank account ownership and what it means to be ‘unbanked.’ Together, these trends underscore how growing costs and persistent inequities continue to shape financial health across America.”

About the Financially Vulnerable

According to Financial Health Network, when it comes to financial health and racial disparities in fees and interest:

- For Financially Vulnerable households, spending on fees and interest alone made up 17% of their income, compared with just 1% among Financially Healthy households.

- Black households spent twice as much of their income on financial services as white households (8% vs. 4%)

- Households with subprime credit contributed 14% of household income toward fees and interest for financial services, compared with 2% among households with prime credit.

Overall Key Findings on Financial Services Fees and Interest 2024

For households overall, the Financial Health Network reported:

- Debt manageability is declining for some households. Only 57% of households carrying credit card debt month to month reported their debt is manageable in 2024, down from 67% in 2020.

- Credit products continue to drive growth in estimated spending, led by credit card debt and student loans.

- Estimated spending on fees and interest for federal student loans more than doubled year-over-year, rising to an estimated $31 billion in 2024. Almost one quarter of borrowers in active repayment reported struggling to make payments.

- More than half of U.S. households hold multiple checking accounts, often across different institutions.

“The FinHealth Spend 2025 report comes at a moment of profound political and regulatory shifts,” the organization said in releasing the findings. “As policymakers, business leaders, and advocates seek to build financial health and resilience across America, transparent and trusted data is essential. Financial Health Network research shows that while innovation is growing across the financial services landscape, the costs of financial services continue to fall most heavily on the households least equipped to bear them.”

Among some of the key topics explored in the report:

Credit Card Debt The Big Driver of Spending on Fees and Interest

The analysis found that during 2024 Americans paid an estimated $165.1 billion in fees and interest on revolving general purpose credit card balances.

“Year-over-year growth in credit spending slowed as the growth in average credit card interest rate moderated, with interest and fees rising 10% in 2024 compared with 25% in 2023,” Financial Health Network reported. “Still, rising total outstanding balances and delinquencies indicate that credit card debt became harder to manage for many families, with vulnerable households significantly more likely to report incurring late fees. As balances have continued to grow over the past five years, households who carry credit card debt have reported less confidence in managing their overall household debt – underscoring growing strain among some borrowers.”

Card Spend Details

The report found spending on fees and interest for private label cards held relatively steady at $15.4 billion, essentially unchanged from 2023.

Overall,fees paid by households who carried a balance on general purpose cards were estimated at $25.8 billion, or 16% of fees and interest combined.

“Disparities were stark,” according to FHN, which found:

- 49% of Financially Vulnerable households paid a late fee, compared with 3% of Financially Healthy households

- Black (20%) and Latine (16%) cardholders reported higher late fee incidence than white households (9%)

- Only 57% of households with revolving credit card debt reported their debt was manageable in 2024, down from 67% in 2020.

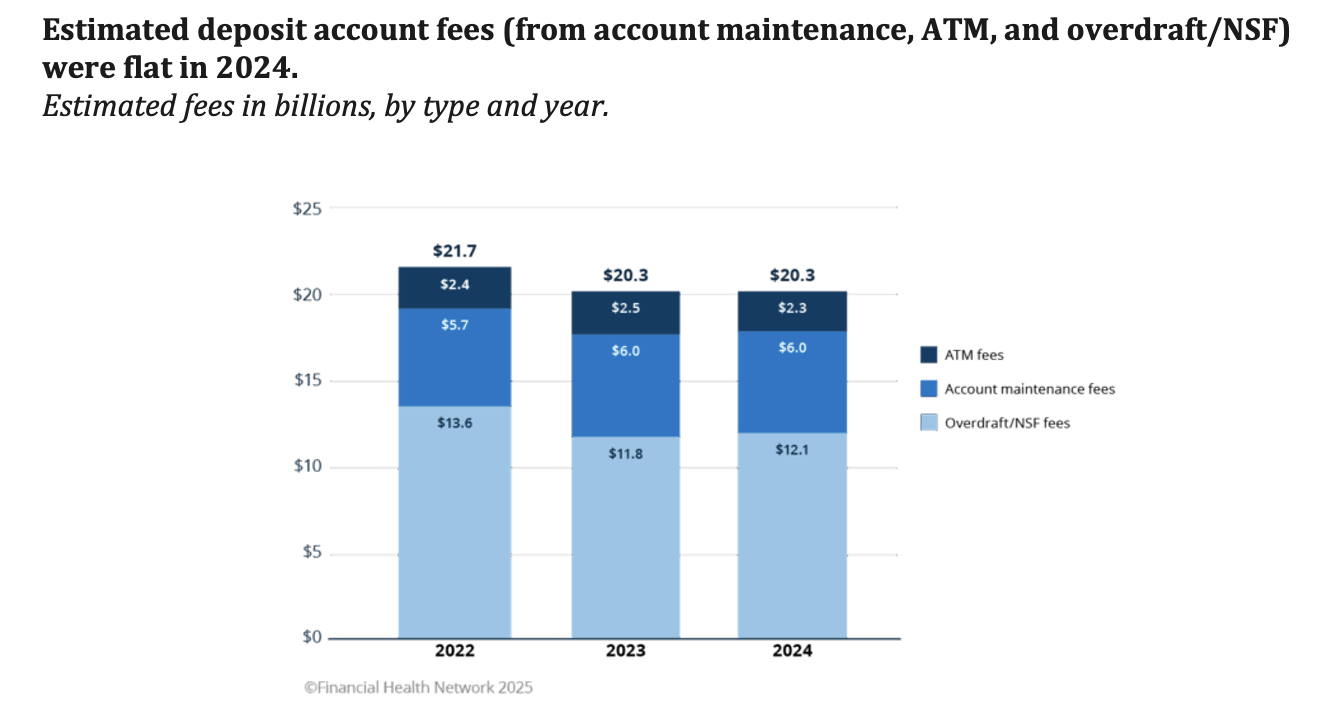

Transaction and Deposit Services: Persistent Costs, Shifting Behaviors

According to Financial Health Network, in 2024, households spent an estimated $43.1 billion on transaction and deposit fees – essentially flat compared with 2023.

“Despite this stability, some fee pressures persist, with overdraft fees rising slightly for the first time in several years,” Financial Health Network said. “The data also indicate substantial account fragmentation, as many households hold multiple checking accounts across institutions, reflecting the growing complexity of household banking relationships.”

The report added that overdraft/NSF fees rose slightly to an estimated $12.1 billion, ending a multi-year decline.

Of particular note, it added that credit union overdrafters reported higher frequency of fees than bank overdrafters.

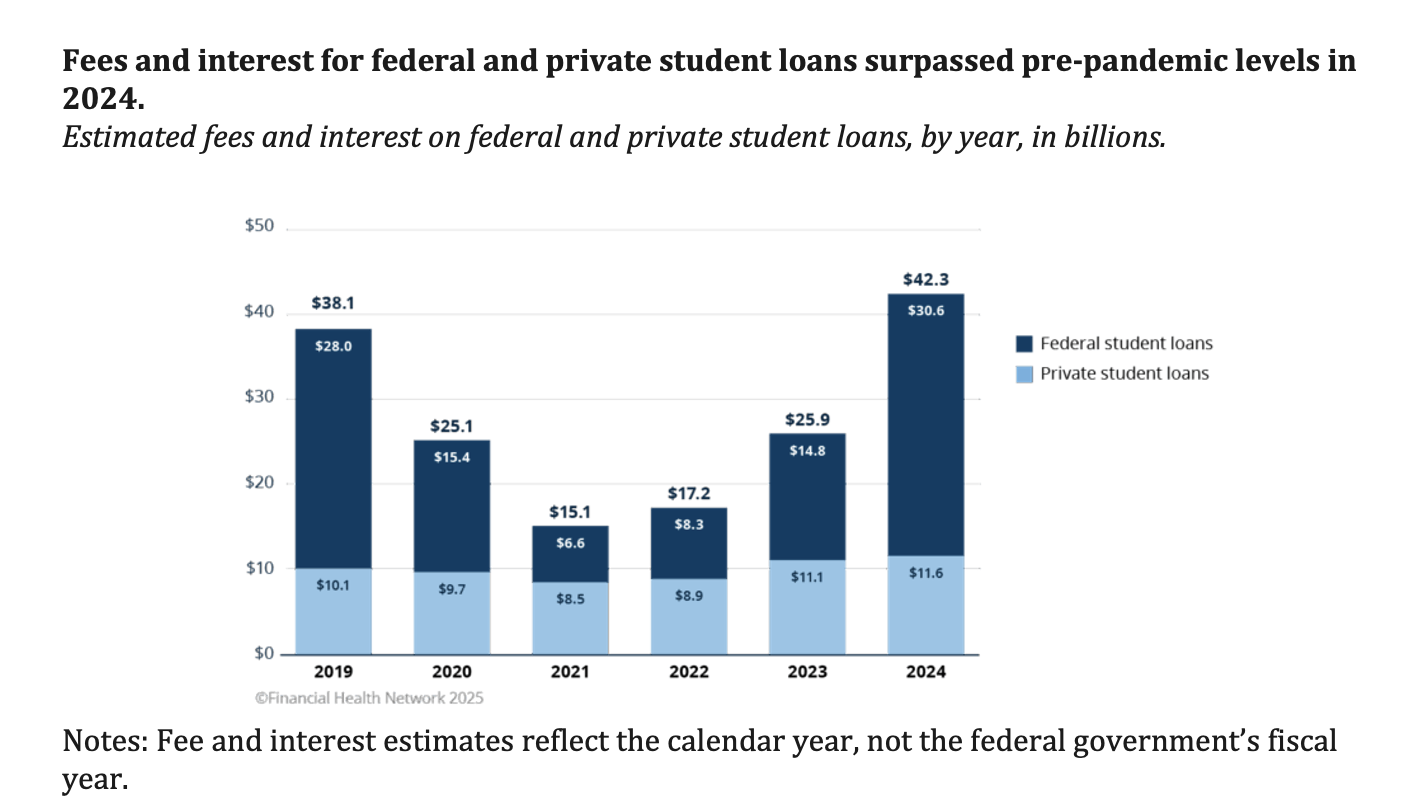

Student Loans in 2024: Fees and Interest Double, Borrowers Struggle

According to the analysis, estimated student loan spending rose sharply in 2024, following the end of pandemic-era forbearance programs.

“For the first time in years, many borrower households faced a full calendar year of payments, and fees and interest on federal student loans more than doubled to an estimated $30.6 billion, surpassing pre-pandemic levels,” Financial Health Network said.

The report found:

- Households spent an estimated $30.6 billion in fees and interest on federal student loans in 2024, more than double 2023 levels.

- Estimated spending on federal student loans exceeded pre-pandemic highs, marking a five-fold increase from the 2021 low

- 37% of households currently making student loan payments reported repayment challenges from missed or late payments to forgoing essentials to stay current.

- These challenges were most acute among Black households, lower-income families, and subprime borrowers.

BNPL: Loan Stacking and Affordability Concerns

While the overall share of households using buy now, pay later (BNPL) loans remained steady in 2024, households reported taking out more loans than in the past, according to the report.

“Sixty percent of BNPL users reported taking out three or more loans in 2024, compared with 53% in 2023 and 51% in 2022,” the report stated. “A persistent question about BNPL has been whether users are “stacking” multiple, concurrent loans from different institutions – a practice that may expose borrowers to unmanageable levels of debt and lenders to greater risk. One-third of BNPL users reported having taken loans multiple times in the past month, signaling overlapping payments. Among that group, 41% said their loans came from more than one provider.”

The BNPL Trends

Among the BNPL trends:

- 16% of households reported using BNPL loans in 2024, essentially unchanged from the 17% of households who reported using this service in 2023.

- Among BNPL users, 60% reported taking out three or more loans– up from 53% in 2023.

- Of those with multiple loans in the past month, 41% borrowed from more than one provider – suggesting “stacking” is taking place

- Reported spending challenges increased, with more BNPL users reporting difficulty affording payments

- The share of users reporting no issues declined from 61% in 2023 to 55% in 2024, a significant decline.

Consumer Sentiment Remains Low

“While overall growth in household spending on financial services moderated, research shows consumer sentiment around cost of living and the economy remained low,” Financial Health Network said. “Our analysis finds that aggregate household spending on fees and interest continued to rise in 2024, with vulnerable populations shouldering the brunt of these financial burdens. As in past years, the costs of financial services have the biggest implications for Financially Vulnerable households, subprime borrowers, and Black and Latine families.

“These findings underscore the need for sustained attention from policymakers, financial services providers, and advocates to better understand trends in consumer spending and spotlight new opportunities to advance equitable financial health policies. Without intentional action, the unequal distribution of financial costs will deepen – leaving millions of Americans exposed to debt stress and ongoing insecurity,” the report added.