SAN DIEGO–Four strategies for driving new organic growth — both large and small — at credit unions were shared by one person here, who challenged CUs to recognize that what they offer is a commodity but that there are still some “sexy” differences to be leveraged.

The lack of growth among CUs is evident in NCUA’s just-released Third Quarter 2025 NCUA Quarterly Data Summary Report, which shows that CUs in every asset category below $1 billion reported declining loans and membership, as the CU Daily reported here.

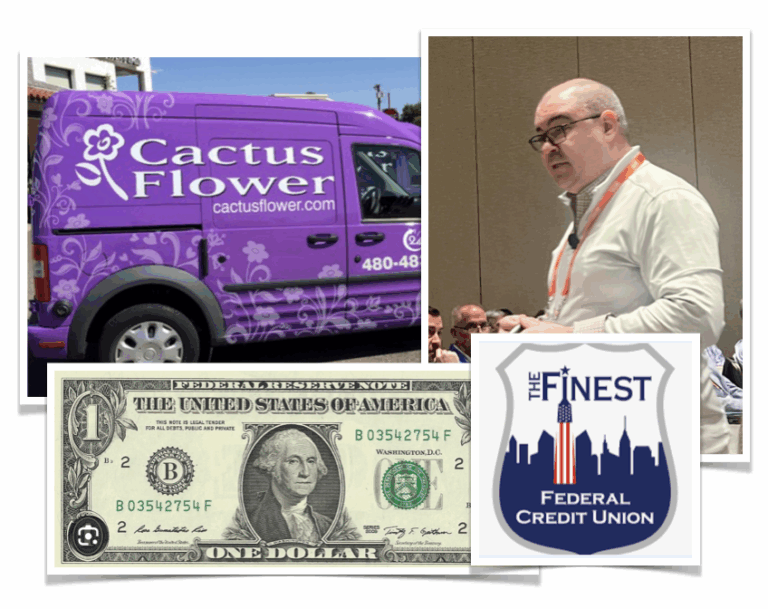

Sharing specific strategies for growth with the CUES Directors Conference was Cisco Malpertida Smith, a managing director with SRM, who began his career at BECU in Seattle, where he was the first person hired to identify strategies for organic growth. He then spent five years with GTE Financial CU in Tampa, was CEO of The Florist FCU, currently works as fractional CEO for one small credit union, and is working to start two de novo credit unions.

“The challenge right now is we seem to be growing pretty well when it comes to the M&A side, right? But that’s inorganic,” Malpertida Smith said. “A lot of credit unions are really struggling to grow organically…Most smaller credit unions are not necessarily growing, but it doesn’t mean that they don’t have the ability.”

CUs Have Loans — And So Does Everyone Else

That ability requires thinking about effective differentiation, said Malpertida Smith, noting that all financial institutions and credit unions offer the same products, all with the same great rates, with everyone saying “we have great service” as their differentiator.

“So, what differentiates us from the next institution? It isn’t the name on the wall. There may be a little bit of that loyalty to your brand, but is that all we have to hang our hat on?” he asked. “That’s the problem. We have become a bit of a commodity. How do we get new members? There are ways to differentiate in this sea of commodity.

“We need to grow membership. Membership is a pretty important KPI,” Malpertida Smith continued. “This is the canary in the coal mine. If we’re not viable to new members, that’s inherently a problem in our business.”

Some Real-World Examples

Malpertida Smith shared some examples of what he has done during his career to differentiate, offering both small-budget and larger-budget strategies.

He began by relating how, during his time at BECU, he found himself manning the typical table at an event, with the table covered in a credit union-branded apron and its surface covered in cheap branded tchotchkes as giveaways — the approach taken by most credit unions at such events.

“People really don’t want to talk to you, they just want the free stuff,” he said.

The ‘Sexy’ Stuff FIs Have

Malpertida Smith said he began thinking about the brands that do it right, and his first thought was of Apple, where the stores are always full even if the mall is empty. Why? What did Apple have?

“A lot of sexy hardware, well displayed,” he said, answering his own question. “This can be done in financial services, which is the opposite of sexy. We have something even sexier: we have money!”

And that became the BECU giveaway. It handed out $1 and $2 bills affixed with stickers about the credit union. Malpertida Smith said he got out from behind the table at events and instead gave away the currency, asking passersby, “Would you like a free sample? And if you like the sample, we can give you $25 more.” He called it “the most cost-effective and effective strategy.”

He said it might cost BECU $500 for the day, but it was already spending that on tchotchkes while now having 400 authentic conversations with potential new members.

He also shared two tips: $2 bills have the same effect at twice the cost, and the stickers need to be easy to remove.

An Idea Flowers for Making Loans

As a second strategy, Malpertida Smith shared how, while CEO of The Florist FCU in New Mexico — which has a national FOM, including not a single board member living in the state —

As an aside, Malpertida Smith observed that he believes, “There are opportunities in a SEG-based credit union. I almost want to go back to that, because we had definition. I think the community charter is one of the best and worst things to happen to credit unions. We can now serve everyone, but we don’t know who we serve.”

A Conversation Spurs a Program

While leading The Florist FCU, Malpertida Smith recalled speaking with one woman who was a member and a florist who had gotten a loan through another credit union for a delivery van.

She shared how just about every florist bought the same van and then would have the vans customized for their businesses. Malpertida Smith contacted Ford Fleet Sales and asked if he committed to purchasing 30 or 40 vans per year, could he get discounted pricing. Ford said yes.

That led to The Florist FCU creating a microsite on which florists could buy a van, get financing and upload their logo to have all the graphic work included on the van as well.

“We offered a floral delivery van loan that solves all their problems. Others just offer auto loans,” he said, before asking his audience, “What about plumbers and electricians and other businesses” that use work trucks?

No Longer a Commodity

“Now it’s not the commodity of an auto loan, it’s something that serves the needs of our market,” he said. “Do you think you might have needs in your market? Are you just offering what everybody else has? Is there a financial problem? Then think creatively about ways to solve that problem.”

He reminded the audience that BECU began as a CU chartered by a small number of Boeing employees with a purpose of helping each other buy work tools.

A Loan Made in the Line of Duty

A third example of finding organic growth opportunities that Malpertida Smith shared involves The Finest FCU, which serves the New York Police Department. It offers a “line of duty” insurance that will forgive up to $800,000 in loan balances if the member dies in the line of duty.

“It’s about $130 a policy. You think police officers valued that? What other financial institution is doing that?” he asked.

The Old College Try

As a fourth example of ways to drive organic growth, Malpertida Smith cited efforts he has overseen to attract college-age members. He noted most financial institutions compete for members ages 25-45, who are in their prime borrowing years. But that’s an extremely competitive market, he said, sharing how he had recently been offered $900 by Chase Bank to move his business.

“My argument is we can win the long game,” he said. “They have quarterly targets they have to meet.”

Malpertida Smith noted the average credit union member is 52 or older, and said the goal should be 45, if not younger.

“Where in the marketplace do we have an opportunity? Colleges are like manufacturing plants of young professionals. If we can go to this bottleneck point and develop a level of trust and expose them to what the positive value of a credit union is, I argue we can get them to carry that through their life stages,” he said. “It’s a good opportunity to indoctrinate and evangelize them while they are in school.”

Malpertida Smith said that while at GTE Financial CU, its college strategy drove 25,000 new members over about four years.

Rethinking Credit-Builder Loans

One specific approach it took was with so-called credit-builder loans. He noted that at most CUs and other financials, even though it’s a small amount of money, that $1,000 placed into a secured savings account can be expensive for many young borrowers.

At GTE, he said the program was interest-only, with the payments reported to the credit bureaus. That lowered monthly payments to around $15 from approximately $100, which he noted was “huge” to a young member.

“Are we growing or surviving?” asked Malpertida Smith. “Because surviving is dying.”

2 Responses

Best quote in the article “I think the community charter is one of the best and worst things to happen to credit unions. We can now serve everyone, but we don’t know who we serve.”

Agreed.