WASHINGTON–President Trump’s announcement that he will impose a credit-card interest rate cap of 10% for one year as a means of addressing the high cost of living has not just been met with strong pushback from credit unions and other FIs, and by members of Congress who say he lacks the authority, it has also raised alarms that the CU-opposed Credit Card Competition Act is about to be resurrected.

When Trump announced his cap on Friday the credit union trade groups were quick to issue statements, with the Defense Credit Union Council saying a 10% cap would have “serious unintended consequences” (the full statements from DCUC and America’s Credit Unionsappears below, as the CU Daily reported earlier).

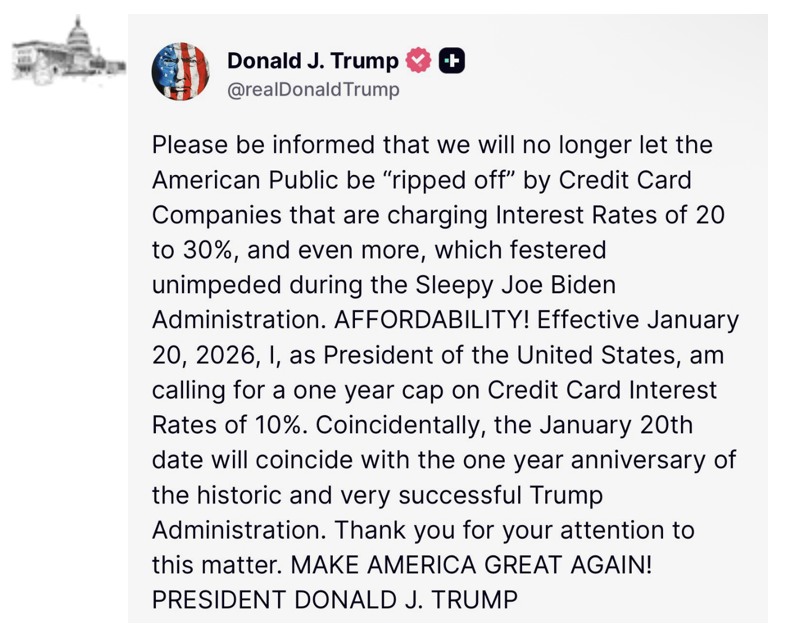

“Please be informed that we will no longer let the American Public be ‘ripped off’ by Credit Card Companies that are charging Interest Rates of 20 to 30%, and even more,” the president said in a post on social media, adding that he wants the cap to begin Jan. 20.

The average credit card APR in the U.S. is approximately 23%, but many are much higher, especially those issued by retailers.

Credit Card Competition Act 2.0?

Meanwhile, Sen. Roger Marshall (R-KS) issued a statement on X saying he had spoken with the president and will be leading legislation to “lower costs for American families and to reign in greedy credit card companies who have been ripping off hardworking Americans for too long.”

Marshall had co-sponsored the Credit Card Competition Act, which would limit interchange fees, along with Sen. Dick Durbin (D-IL) in prior sessions of Congress. As strongly as credit unions oppose the bill and its provisions, the nation’s retailers support it.

Helped and Hurt

“Borrowers in lower- and middle-income households who carry balances would benefit the most from caps on credit-card charges,” said the Wall Street Journal in its analysis. “They would also be the first ones banks would stop lending to if the caps were enacted, according to experts, and banks might impose fees to make up for lost revenue.”

Bank Groups Say Move Would be ‘Devastating’

The Consumer Bankers Association, Bank Policy Institute, American Bankers Association, Financial Services Forum and Independent Community Bankers of America issued a joint statement that said, in part, that a 10% interest rate cap would “reduce credit availability” and “only drive consumers toward less regulated, more costly alternatives” and would reduce the availability of credit.

In a joint statement the bank groups said, “…evidence shows that a 10% interest rate cap would reduce credit availability and be devastating for millions of American families and small business owners who rely on and value their credit cards, the very consumers this proposal intends to help. If enacted, this cap would only drive consumers toward less regulated, more costly alternatives.

Congressional Pushback

Almost immediately after Trump made his announcement, members of Congress said the president’s threat to impose a cap is meaningless without legislation passed by Congress.

“Begging credit card companies to play nice is a joke. I said a year ago if Trump was serious, I’d work to pass a bill to cap rates,” said Sen. Elizabeth Warren (D-MA).

Warren criticized Trump’s call for an APR cap to lower costs at the same time he has sought to eliminate the Consumer Financial Protection Bureau and has scrapped a credit card late fee rule from the era of former President Joe Biden that would have capped credit card late fees at $8. That proposal, which was ruled illegal by a court, was also opposed by credit unions.

Bipartisan legislation that would mandate a 10% rate cap had earlier been introduced in Congress by Rep. Alexandria Ocasio-Cortez (D-NY) Rep. Anna Paulina Luna (R-FL). In the Senate, Sens. Josh Hawley (R-MO) and Bernie Sanders (I-VT) introduced a bill in February of 2025 that called for a similar cap.

“Rates have DOUBLED in recent years. In 2022 alone, credit cards charged Americans $105 billion in interest,” Hawley wrote on the social platform X at the time.

Americans & Credit Card Debt

According to the CFPB, approximately 195 million people in the United States had credit cards in 2024 and were assessed $160 billion in interest charges. As the CU Daily has previously reported, Americans are now carrying more credit card debt than ever, approximately $1.23 trillion in all, according to figures from the New York Federal Reserve for the third quarter last year.

Moreover, Americans are paying, on average, between 19.65% and 21.5% in interest on credit cards according to the Federal Reserve and other industry tracking sources. That’s significantly higher than a decade ago, when the average credit card interest rate was roughly 12%, Inc. reported.

America’s CUs: ‘CU Card APRs Average 8-10 Percentage Points Lower’

In a letter to Trump, America’s Credit Unions said cards offered through CUs and smaller community typically have interest rates eight to 10 percentage points lower on average, which translates to approximately $400–$500 less in interest costs per year on a typical $5,000 credit card balance vs. using the card of a big bank.

The letter further notes:

- FCUs have an 18% interest rate ceiling 18 percent interest

- Credit union card APRs average about 12.7% at credit unions vs. 15.5% at banks

Higher Risk Borrowers to be ‘Cut Off’

“A 10% cap on credit card APRs would dramatically curtail lenders’ ability to manage risk through pricing, forcing them to tighten lending standards and cut off higher-risk borrowers,” the letter states. “Research indicates that as many as two-thirds of current credit card revolvers those who carry balances would likely see their credit lines reduced or eliminated under a 10% cap….The borrowers most vulnerable to losing access are those with imperfect or subprime credit

histories, ironically, the very people who most need the backup liquidity of a credit card in emergencies. These higher-risk consumers require higher interest rates to compensate for

default risk; if rates cannot exceed 10%, issuers will simply be unable to extend credit to them.

“In fact, close to 75 percent of credit card users with riskier credit profiles would be adversely affected by a 10% cap, losing access to their cards,” the letter continues, noting approximately 47 million Americans are currently considered subprime borrowers.

Simpson: ‘Devastating for Members’

“Credit unions were founded as the original consumer protectors, and that mission still shows up in the real-world value they deliver every day. Their members consistently benefit from the lowest rates in the marketplace, roughly half the average APR charged by other issuers, which translates into meaningful, measurable savings for working families,” said America’s Credit Unions President and CEO Scott Simpson in a statement. “That’s affordability people can feel in their financial well-being. A 10% interest rate cap would be devastating for credit union members. While we appreciate the President’s desire to increase affordability, the plain truth is that capping rates at 10% does not make credit more affordable, it makes it unattainable for millions of working Americans because financial institutions will not be able to offer credit cards to most consumers at a 10% rate.

“We will continue to work to ensure this policy does not harm the very people the President intends to protect,” Simpson added.

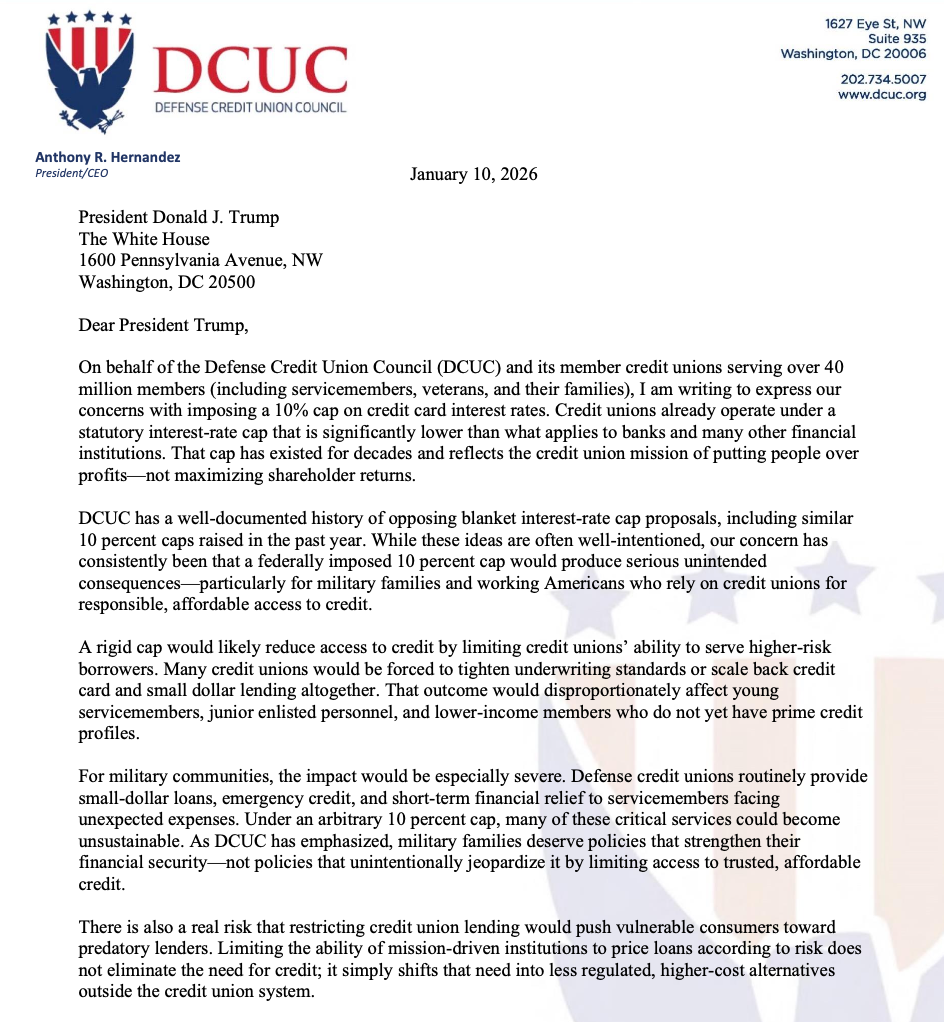

Defense CU Council Responds

The Defense Credit Union Council noted it has been heavily engaged on this issue since the President announced the proposal via social media late Friday night. Over the weekend, DCUC sent a letter of concern to President Trump, and a similar letter to the Chair and Ranking Members of the Senate Committee on Banking, Housing and Urban Affairs, and the House Financial Services Committee. Every congressional office on Capitol Hill also received copies.

‘Not Paid to Sit’

With Trump indicating the cap could take effect as early as Jan. 20, 2026, DCUC is urging immediate engagement and has produced talking points credit unions can use to “clearly and specifically explain how a blanket interest rate cap would negatively affect responsible lending, financial readiness, and access to credit for military families and working Americans.”

“As I have said before, ‘Credit unions don’t pay dues to their trade associations and leagues to sit and monitor a situation! They pay us to take & organize action,” D Anthony Hernandez, DCUC President/CEO. “We don’t have much time to respond as narratives are already being set. This is why DCUC has been working hard over the weekend.”

‘Reduces Access’

Separately, Jason Stverak, chief advocacy officer with DCUC, issued a statement saying, “Credit unions already operate under a statutory interest-rate cap that is significantly lower than what applies to banks and many other financial institutions. That cap has existed for decades and reflects the credit union mission of putting people over profits—not maximizing shareholder returns,” said DCUC Chief Advocacy Officer Jason Stverak in a statement. “DCUC has a well-documented history of opposing blanket interest-rate cap proposals, including similar 10% caps raised in the past year. While these ideas are often well-intentioned, our concern has consistently been that a federally imposed 10% cap would produce serious unintended consequences—particularly for military families and working Americans who rely on credit unions for responsible, affordable access to credit.

“A rigid cap would likely reduce access to credit by limiting credit unions’ ability to serve higher-risk borrowers,” Stverak continued. “Many credit unions would be forced to tighten underwriting standards or scale back credit card and small-dollar lending altogether. That outcome would disproportionately affect young servicemembers, junior enlisted personnel, and lower-income members who do not yet have prime credit profiles.

‘Especially Severe’

For military communities, the impact would be especially severe. Defense credit unions routinely provide small-dollar loans, emergency credit, and short-term financial relief to servicemembers facing unexpected expenses,” Stverak added. “Under an arbitrary 10% cap, many of these critical services could become unsustainable. As DCUC has emphasized, military families deserve policies that strengthen their financial security—not policies that unintentionally jeopardize it by limiting access to trusted, affordable credit.

“There is also a real risk that restricting credit union lending would push vulnerable consumers toward predatory lenders. Limiting the ability of mission-driven institutions to price loans according to risk does not eliminate the need for credit; it simply shifts that need into less regulated, higher-cost alternatives outside the credit union system.”

Broader Threat

Stverak said interest-rate cap proposals threaten the broader service model that defense credit unions provide.

“Beyond lending, our credit unions deliver financial counseling, fraud protection, deployment-related assistance, and tailored relief products for servicemembers and their families. A one-size-fits-all cap could undermine the sustainability of those services,” he said in a statement.”

Stverak said that rather than imposing a blanket national cap, DCUC has urged policymakers to pursue more targeted consumer protections—expanding financial education, promoting responsible lending, and directly cracking down on predatory actors.

“We look forward to working with Congress and the Administration to highlight the indispensable role credit unions play in supporting financial readiness for our armed forces and the hard-working American worker, while ensuring policy solutions do not penalize the institutions that have consistently put people first,” he said.

‘Not Your Father’s Republican’

John McKechnie, who advocates on Capitol Hill on behalf of credit unions, said in a statement, “If you ever needed proof that Donald Trump is not Your Father’s Republican, here it is. The president has embraced a type of economic populism that you would have expected from Bernie Sanders and AOC. This move not only stirs the pot on credit card interest rates, but it could have ramifications for other card issues. Buckle up.”