TROY, Mich.–For the second consecutive quarter, J.D. Power is reporting it found the number of consumers who are “soft switching” their financial relationships—that is quietly opening secondary accounts and gradually making them their primary accounts—has increased.

The company said its Financial Services Churn Data and Analytics report found that fintech companies have emerged as major beneficiaries of the trend

The report, which tracks customer attrition among leading financial institutions, found fintech brands such as Chime and SoFi are attracting and converting new account openings faster than more traditional financial institutions, particularly among mass-market customers. Traditional banks continue to dominate new account openings among higher-income and affluent customers.

Secondary Accounts Drive Openings

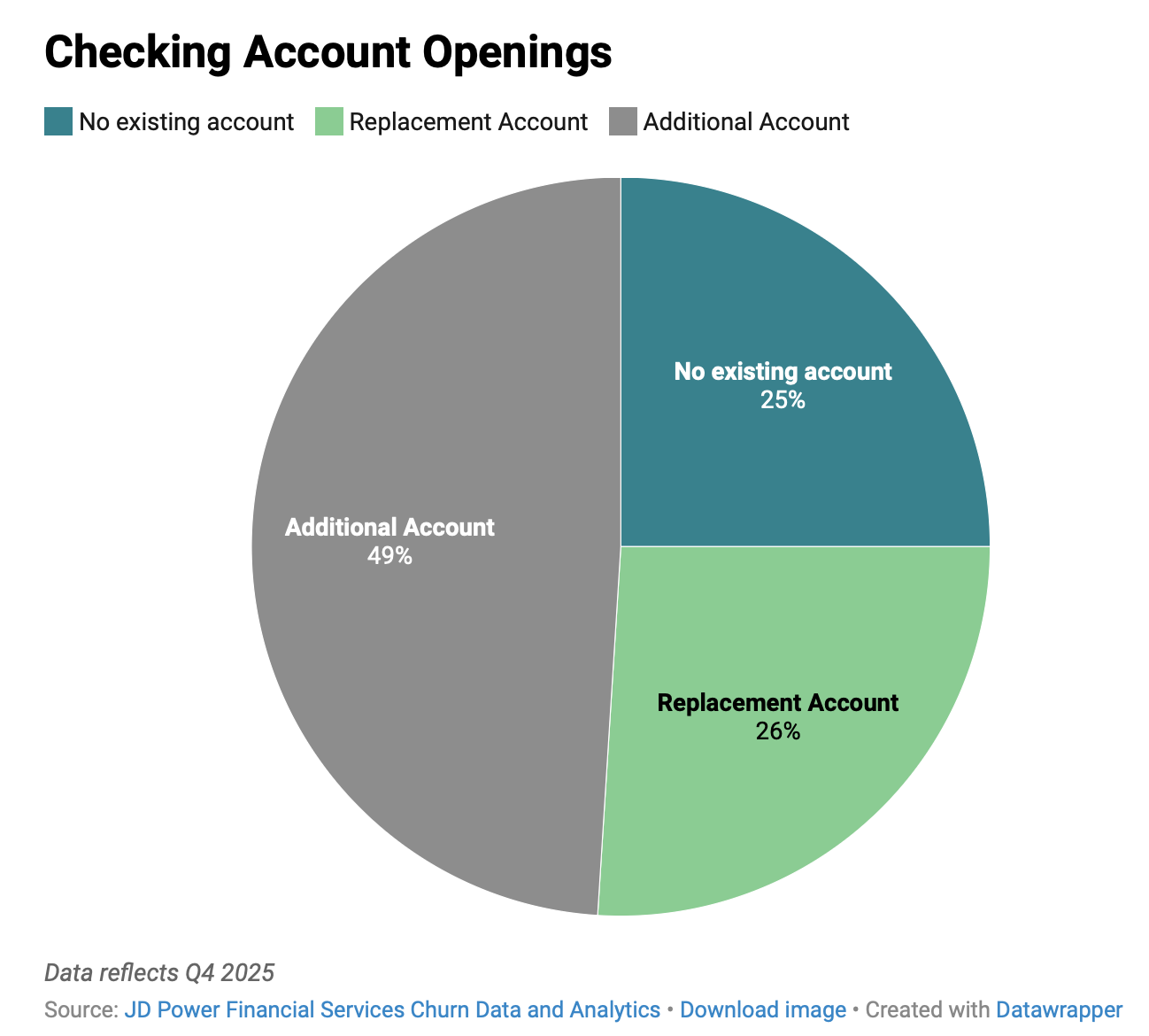

According to the report, nearly half of new checking accounts (49%) and 46% of new savings accounts opened during the fourth quarter of 2025 were secondary accounts created by customers who already had an existing banking relationship.

Another 26% of checking accounts and 18% of savings accounts were opened as replacement accounts, while 25% of checking and 36% of savings accounts represented new relationships for customers who previously did not have such accounts.

J.D. Power said the pattern, which mirrors results from the third quarter of 2025, suggests many consumers are diversifying their banking relationships rather than fully abandoning their existing institutions.

Chime Tops Checking Account Growth

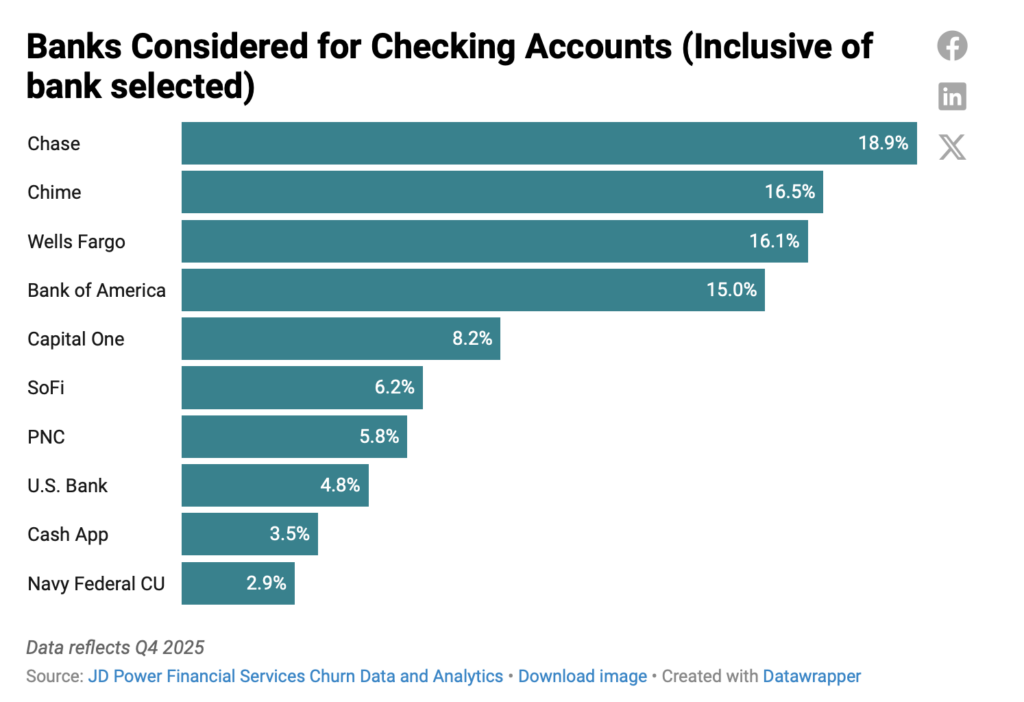

Chime captured the largest share of new checking account openings in the fourth quarter at 12.8%, followed by JPMorgan Chase at 8.4% and Wells Fargo at 7.1%.

In savings accounts, Chase led with 9% of new openings, followed by Chime with 8.4% and Bank of America with 6.3%.

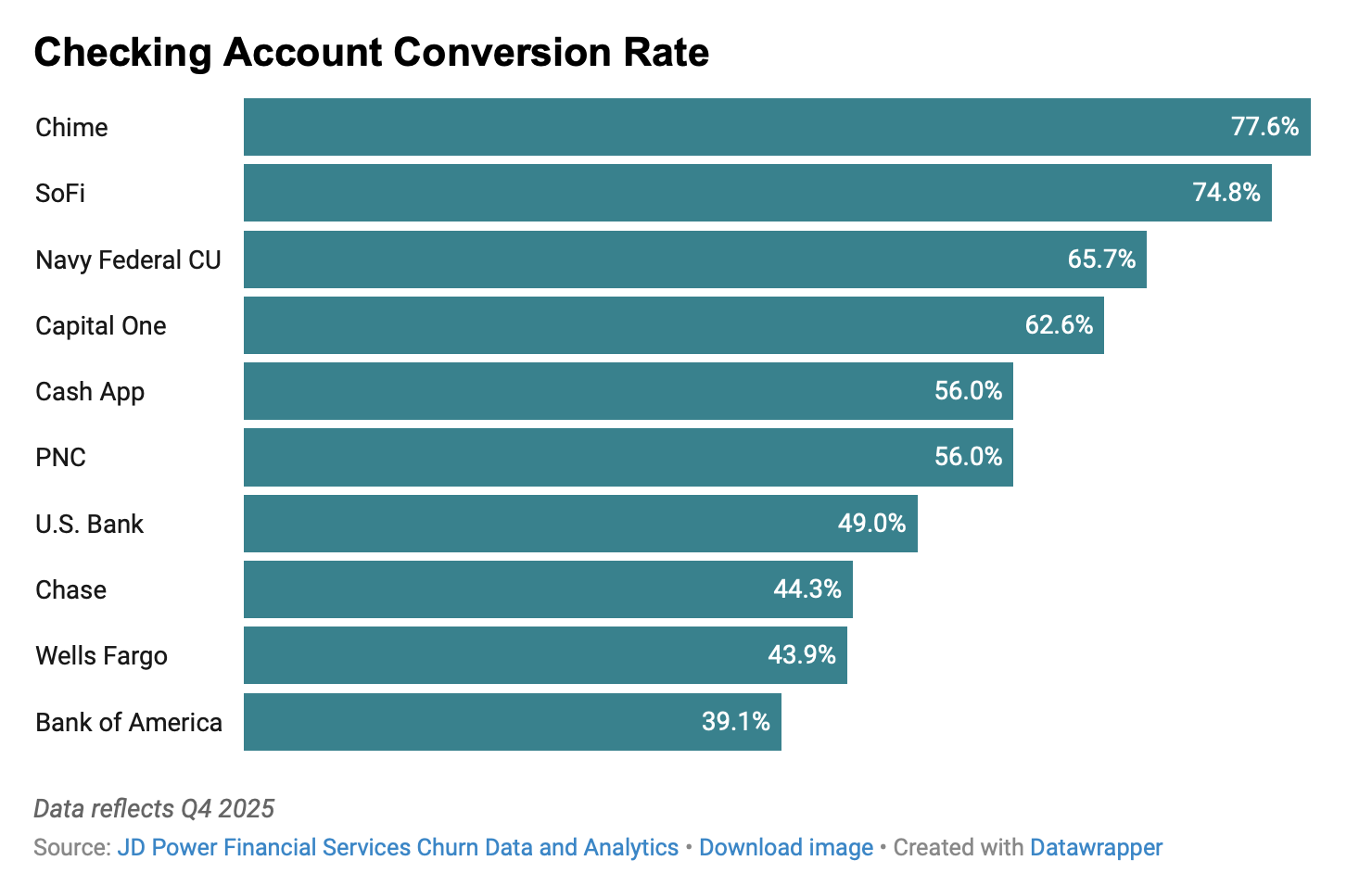

Chime also posted the highest conversion rates — the percentage of customers who ultimately opened accounts after considering multiple providers. The company converted 78% of customers considering new checking accounts and 85% considering new savings accounts, outperforming both fintech and traditional competitors, the report said.

Big Banks Lead With Wealthier Customers

While fintech firms gained traction with mass-market consumers, large national banks continued to perform strongly among wealthier customers.

Among checking accounts, Chime led customer acquisition in the mass-market segment with 11.5% of new customers. Chase led the mass-affluent segment with 10.9%, while Bank of America captured 14.1% of new affluent customers.

In savings accounts, Chime again led the mass-market segment with 11.5% market share. Chase led among both mass-affluent customers at 9.7% and affluent customers at 11.5%.

Investment Accounts

In the investment category, Fidelity captured the largest share of new accounts in the fourth quarter with 16.8%. Charles Schwab followed with 9.1% and Robinhood with 8%, according to the J.D. Power findings.

However, fintech company SoFi recorded the highest conversion rate, capturing 83.1% of accounts opened after customers evaluated competing providers. Fidelity converted 80.2% of such customers and Acorns converted 78.2%.

When broken down by total investable assets, Fidelity led across all wealth tiers — 16.3% of mass-market customers, 17.7% of mass-affluent customers and 16.4% of affluent customers. Robinhood ranked second in the mass-market segment with 10.5%, while Schwab ranked second among both mass-affluent customers at 10.8% and affluent customers at 13.1%.

Growing Competition

J.D. Power said the findings highlight a shifting marketplace in which consumers are increasingly exploring new providers while maintaining existing relationships.

The company said growing interest in fintech brands — particularly among mass-market customers — suggests digital engagement and technology-driven experiences could play a major role in the future competitive landscape of financial services.

The report is based on 263,151 customer responses collected between October and December 2025 as part of the J.D. Power Financial Services Churn Data and Analytics research program. The analysis was authored by Jennifer White, senior director of financial services intelligence at J.D. Power.