By Michael C. Macchiarola

We believe credit unions are entering a period where defensive balance-sheet positioning is becoming increasingly important. While the sector remains fundamentally well capitalized and historically conservative, several macro and industry-specific signals suggest that now may be an opportune moment for institutions to consider raising subordinated debt as a precautionary capital buffer.

Three themes stand out: emerging credit stress in consumer portfolios, uncertainty surrounding labor market disruption from artificial intelligence, and early cracks appearing in private credit markets.

Deteriorating Asset Quality Metrics

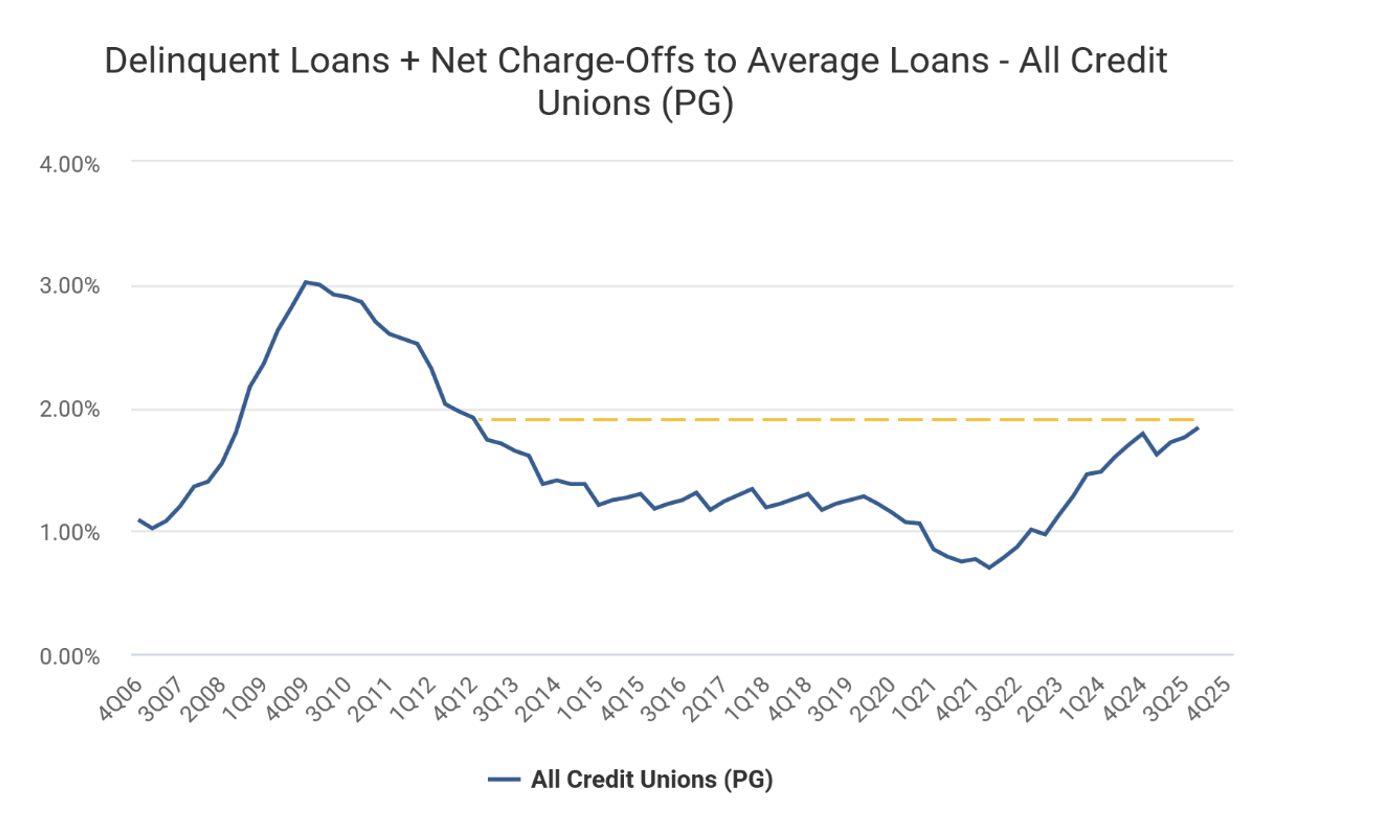

First, asset quality metrics across the credit union industry are beginning to deteriorate from unusually benign post-pandemic levels. Delinquencies and charge-offs have been rising steadily over the past two years as higher interest rates, pandemic-era savings depletion, and increased consumer leverage weigh on household balance sheets. Chart 1 below illustrates this shift clearly: the combined delinquency and net charge-off rate for credit unions has climbed to the highest level since 2012.

This trend is not yet alarming in absolute terms, but the slope of the trendline matters. Historically, credit performance turns gradually and then deteriorates more rapidly once economic conditions weaken. For credit unions with growing exposure to unsecured consumer lending, indirect auto, or higher-risk member segments, the normalization in credit costs may still have further to run.

Raising subordinated debt during a period when capital markets remain relatively receptive allows institutions to add loss-absorbing capital before stress intensifies. We see significant advantages in being in front of a supply-demand equilibrium that can turn from an issuer’s market to a buyer’s market overnight.

An Uncertain Labor Market

Second, the outlook for the labor market has become more uncertain. This matters because labor conditions are one of the most important drivers of consumer credit performance. Although headline unemployment remains relatively low, several Federal Reserve research indicators suggest that underlying labor market momentum may be weakening.

Research from the Federal Reserve Bank of Minneapolis indicates that traditional measures of labor market tightness may overstate current strength. When adjusting job vacancy data from the Job Openings and Labor Turnover Survey (JOLTS) to account for measurement distortions, economists at the Minneapolis Fed recently observed that labor market tightness may already be closer to, or even below, pre-pandemic levels. In other words, the gap between labor demand and labor supply may be narrowing faster than commonly assumed.

One Early Signal

The Chicago Fed’s Labor Market Indicators show that hiring rates for unemployed workers have begun to decline, an early signal that job-finding prospects are softening. Historically, declines in hiring rates tend to occur before increases in the unemployment rate, making them a useful early warning sign for shifts in labor market conditions.

Beyond cyclical dynamics, structural changes driven by artificial intelligence are adding a new layer of uncertainty to the employment outlook. Advances in AI and automation are expected to reshape employment patterns across a wide range of industries. Academic research suggests a large share of the workforce could see meaningful portions of their job tasks affected by generative AI technologies. While productivity gains from these technologies may ultimately benefit the broader economy, the transition could create uneven employment adjustments across sectors and regions.

Stark Warnings

Some technology leaders have begun issuing stark warnings about the pace of disruption. For example, venture capitalist Vinod Khosla, an early investor in OpenAI, recently argued that artificial intelligence could ultimately replace as much as 80% of existing jobs as automated systems take on a growing share of economic production. Similarly, Anthropic CEO Dario Amodei has cautioned that AI could eliminate significant portions of entry-level white-collar roles in fields such as law, consulting, and finance within the next several years.

While such projections remain the subject of great debate, nevertheless, they underscore the possibility that the labor market could face meaningful transition risk.

For member-focused institutions like credit unions, localized employment shocks can translate directly into credit deterioration within their loan portfolios. Unlike large, diversified banks, many credit unions serve concentrated geographic or employer communities. If AI adoption accelerates layoffs or wage compression in specific industries, delinquency rates could rise quickly across those member segments. Strengthening capital buffers in advance provides flexibility to absorb potential credit losses while continuing to serve members during periods of economic transition.

Stresses in Private Credit Markets

Third, stress signals emerging in private credit markets provide an additional cautionary indicator. Large asset managers including Blue Owl and BlackRock have recently highlighted rising borrower stress and increased restructuring activity within certain private lending portfolios. Private credit has grown rapidly over the past decade, often financing highly leveraged companies that may struggle if growth slows or refinancing conditions tighten.

While credit unions generally have limited direct exposure to these funds, problems in private credit can serve as a canary in the coalmine for broader credit conditions. Historically, stress tends to appear first in leveraged corporate markets before spreading into consumer and small-business credit channels. If private lenders begin to experience higher defaults, it could signal that tighter financial conditions are starting to bite more broadly across the economy.

Recent revisions to key economic data may suggest that the softening in credit conditions is not merely a forward-looking risk but is already underway. Restatements of measures tied to consumer balance sheets and economic activity have painted a weaker picture of recent months than originally reported.

Notable Direction

The direction of the adjustments is notable: growth appears somewhat slower and financial stress somewhat higher than previously believed. For lenders and credit analysts, that shift reinforces the possibility that the early stages of credit deterioration are already emerging beneath what had appeared to be relatively stable and encouraging headline data.

Against this backdrop, subordinated debt represents an increasingly attractive strategic tool for credit unions. Unlike traditional deposits or retained earnings, subordinated debt provides long-term capital that can strengthen net worth ratios without diluting member ownership. It also creates a cushion that can absorb losses while preserving lending capacity during downturns.

How to Remain Resilient

Importantly, raising capital is far easier when conditions are still relatively stable. Once credit stress becomes visible in earnings or regulatory metrics, funding costs rise and market access can narrow. Institutions that proactively issue subordinated debt today can lock in capital at more favorable terms while positioning themselves defensively for potential volatility ahead.

Credit unions have historically weathered economic cycles better than many financial institutions due to conservative underwriting and strong member relationships. By combining those structural strengths with proactive capital planning, they can ensure they remain resilient even if credit conditions, labor markets, or broader financial markets become more challenging in the years ahead.

Today, the strategic deployment of subordinated debt can be an important ingredient in that recipe.

Michael Macchiarola is the CEO of Olden Lane Inc.