SACRAMENTO, Calif.— A member of SAFE Credit Union who has publicly opposed the proposed merger between that credit union and Seattle-based BECU said a recent meeting with SAFE President and CEO Faye Nabhani revealed ongoing disagreements over transparency, governance and the potential impact of the deal on members and the Sacramento community.

In response, SAFE Credit Union told the CU Daly it “deeply believes” in listening to its members.

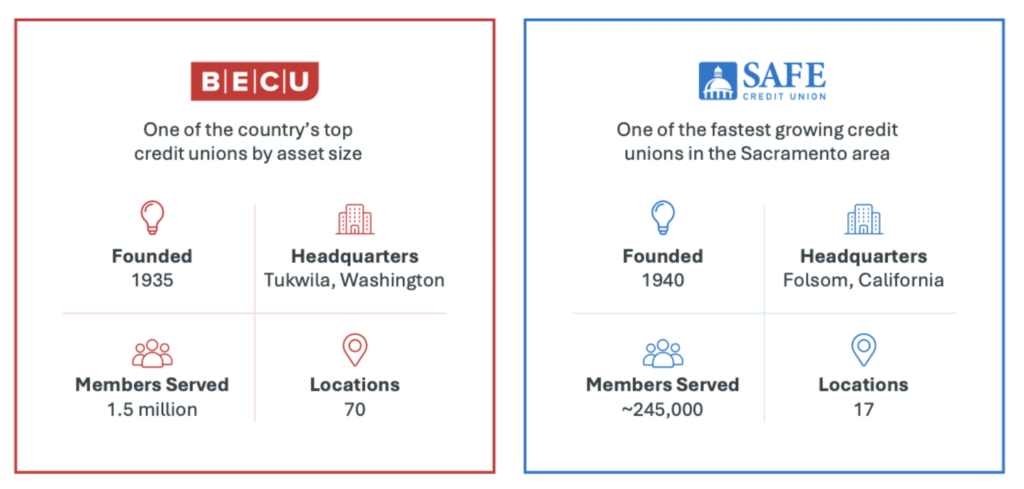

The $4.3-billion SAFE Credit Union asking its members to vote in favor of a merger in the $29-billion BECU. SAFE has nearly 700 employees and about 244,000 members, while BECU employs roughly 3,200 people and serves more than 1.5 million members.

As the CU Daily reported has reported, most recently here, SAFE CU member Scott Rose has published a letter to the editor in the Sacramento Bee and met with local state and congressional representatives to voice his objections to the combination, which include his contention the transaction would result in the termination of SAFE’s charter and the transfer of approximately $4.31 billion in assets — including about $345 million in member equity — to BECU without direct compensation to SAFE’s members.

In a detailed account of the April 7 meeting shared with the CU Daily, Rose said the two held a 2.5-hour discussion that at times became contentious as he pressed his objections to the proposed acquisition by BECU.

Rose said he questioned the strategic rationale for the combination, arguing that SAFE, which he described as a “thriving institution,” would be absorbed by a credit union roughly seven times its size. He said also raised concerns about BECU CEO Beverly Anderson, suggesting her background in commercial banking with Wells Fargo could conflict with credit union principles.

Pushing Back

According to Rose’s account, Nabhani pushed back, saying her experience working with Anderson indicates support for the credit union philosophy of “people helping people,” and expressing confidence that BECU would act in the best interests of the Sacramento region.

A central point of dispute during the meeting was the issue of transparency. Rose alleged Nabhani acknowledged that merger discussions were conducted confidentially and were not disclosed to members prior to the public announcement, including omission from a prior annual meeting agenda.

Nabhani defended that approach, Rose said, arguing that early disclosure could have triggered employee departures and member withdrawals, potentially creating instability.

Rose characterized the decision as a breach of fiduciary duty, asserting that withholding information from members—particularly regarding what he described as a “definitive” agreement—undermined the board’s obligation to act in members’ best interests.

Governance Issues

According to Rose’s account, the discussion also turned to governance issues, with Rose alleging that SAFE’s board nomination process has limited member participation. He claimed that some board candidates were not members until shortly before their nomination, which he said circumvented the intent of the credit union’s bylaws.

According to Rose, Nabhani maintained that the process complies with legal requirements, but acknowledged concerns about whether it aligns with the “spirit of those rules.”

Safe Credit Union’s online listing of its board members indicates its chairman, Rick Blumenfield, has been a SAFE member since 2014, the same year he joined the board. Overall, it indicates nine of the 12 board members become members in the same year they joined the board.

Additional Issues Discussed

According to Rose’s account, additional issues discussed included:

Local Impact

Rose said he further raised concerns about the long-term local impact of the merger, including the future of philanthropic efforts and naming rights tied to SAFE’s presence in Sacramento. He argued that community investment typically follows a company’s headquarters location, suggesting those commitments could diminish under out-of-state ownership.

According to Rose, Nabhani responded that contractual obligations would require BECU to honor existing commitments, though Rose said she acknowledged that some long-term details, including naming rights, remain unresolved.

Employment

Employment was another major focus. Rose said Nabhani indicated the agreement includes an 18-month no-layoff provision for SAFE’s more than 700 employees, but he argued that timeframe is insufficient and called for longer-term protections and severance guarantees.

Commitment to Market

Rose said he also questioned BECU’s long-term commitment to the Sacramento market, suggesting BECU could eventually reduce its local footprint if performance expectations are not met. Nabhani disputed that view but acknowledged there are no explicit guarantees preventing such an outcome, according to Rose’s account.

Regulatory Review

The two also discussed the pending regulatory review, including oversight by California’s Department of Financial Protection and Innovation. Rose said he is seeking to block the transaction before approvals are granted, arguing that a later member vote could be influenced by incomplete information.

Nabhani, he said, maintained that members would have an opportunity to hear opposing viewpoints during the voting process and rejected the notion that the outcome would be predetermined.

No Capital at Risk

Rose additionally raised concerns over what he characterized as a lack of visible capital at risk from BECU in the transaction, warning that the acquiring institution could exit the market with limited downside if the expansion proves unsuccessful.

In response, Nabhani pointed to planned investments by BECU in areas such as improved services, lower rates and reduced fees, though Rose said details have not been publicly disclosed.

Despite sharp disagreements, Rose said he acknowledged SAFE’s strong financial condition, citing its most recent audited financial statements and credited Nabhani’s leadership for the organization’s performance. He reiterated, however, that he believes the merger is unnecessary and poses risks that outweigh potential benefits to members and the broader community.

SAFE Credit Union Responds

In response to a request from the CU Daily for a response, SAFE CU said it is its standard practice to not share details from individual conversations with members. But in a statement,VP Communications and Government Relations Micah Grant said, “As leaders of a member-owned cooperative, SAFE’s board of directors and management deeply believe in listening to our members. We are committed to being available to meet with members who have questions, concerns, or need more information and our CEO feels a strong personal commitment to connecting directly with people and hearing their perspectives. That commitment continues as we move through this process.”

6 Responses

The 18 month no layoff should be little assurance. BECU needs those employees until they get on the same system. After they do, and when the SAFE CEO leaves at 18 months, there won’t be local leadership and no one to protect the local employees and community. Since BECU’s expense issue is so severe, there will be a lot of job reductions in CA.

Performative at best.

Glad these conversations are happening and that he’s asking the right questions—he’s pushing in the way more people should.

What’s becoming clear, though, is that the credit unions don’t really have strong answers—they just have strong PR. BECU, in particular, is very good at managing perception.

Underneath that, the leadership approach feels far more like a traditional bank than a credit union. The new CEO comes across as performative at best—saying the right things publicly, but not reflecting that same philosophy behind closed doors.

Internally, employees have described leadership as political and calculated—always saying the right thing publicly, but the moment anyone questions it, they’re pushed out, fired, or laid off.

BECU isn’t new to working the layoff systems with minimal NDA’s and severance packages. Last April, several employees were let go, and shortly after, nearly identical roles were reposted and filled—often through existing networks or familiar circles. All while moving forward with a costly (millions!) and terribly structured naming rights deal.

You can’t claim credit union values while operating like that.

100% a wolf in sheep’s clothing. Just because you “meet them and they said all the right thungs” doesn’t mean they are not well coach and performative AF. What that leadership teams says in public and what they do behind thr scenes are two very different things.

Do not for profit credit unions have revenue goals?

Someone should from SAFE should ask why BECU’s General Counsel, Chief Auditor, Chief Risk Officer, Chief Impact Officer, and Chief Business Officer all decided to leave, more or less at once. Nothing normal about that.

Don’t forget the ENTIRE executive team that left within months of the new CEO coming on. It’s a revolving door in the C-Suite for a reason.

Most of the employees at BECU were very excited with this hire even knowing the CEO came from Wells Fargo, she seemed to say all the right things, talk about the movement, the members first philosophy, actually we all felt a little inspired and then reality hit.

3.5 years later BECU is a shell of what it was and there is no stewardship towards the CU movement AT ALL behind closed doors, it’s 100% toxic and performative. They have pushed out so many of the employees and leaders that made that place special.

So I am so glad Faye liked her and that Bev said “all the right things” but it is shallow and performative just like others have mentioned. She is a very very good actor in public, she very much slips up behind closed doors. To having the table slammed in front of you while profanities were flying to lying about how she was “listening” to employees with “listening sessions” but behind closed doors was saying “Gotta go pretend that I care about what they say” (jaw dropping really….) to being shushed in meetings for no reason, to tearing people up because they got one thing wrong in a speech she was giving. The executive team is no longer local to Seattle, they live in Atlanta, New York, and LA – flying in on the companies dime with no connection to the region or any care about moving the community forward. Yes, they EMT and Board are being incentivized for a merger, so they chose a “SAFE” merger (pun intended) to get their bonuses and show they increased they asset size, cause their net growth is not great.