ORLANDO, Fla.—A credit union that credits its survival and existence to CUSOs—and which is among the nation’s leaders in the space—shared its history, what it’s doing now and the effect CUSOs have had on its financial performance and bottom line.

During the NACUSO Reimagine 2026 conference, Maps Credit Union CEO Mark Zook delivered an expansive look at how the $1.8 billion Oregon-based credit union built, restructured and in some cases exited CUSO investments over four decades—arguing those entities ultimately “saved the credit union” and continue to shape its strategy today.

“Our credit union wouldn’t exist today without CUSOs,” Zook said.

From Insurance Roots to Early Innovation

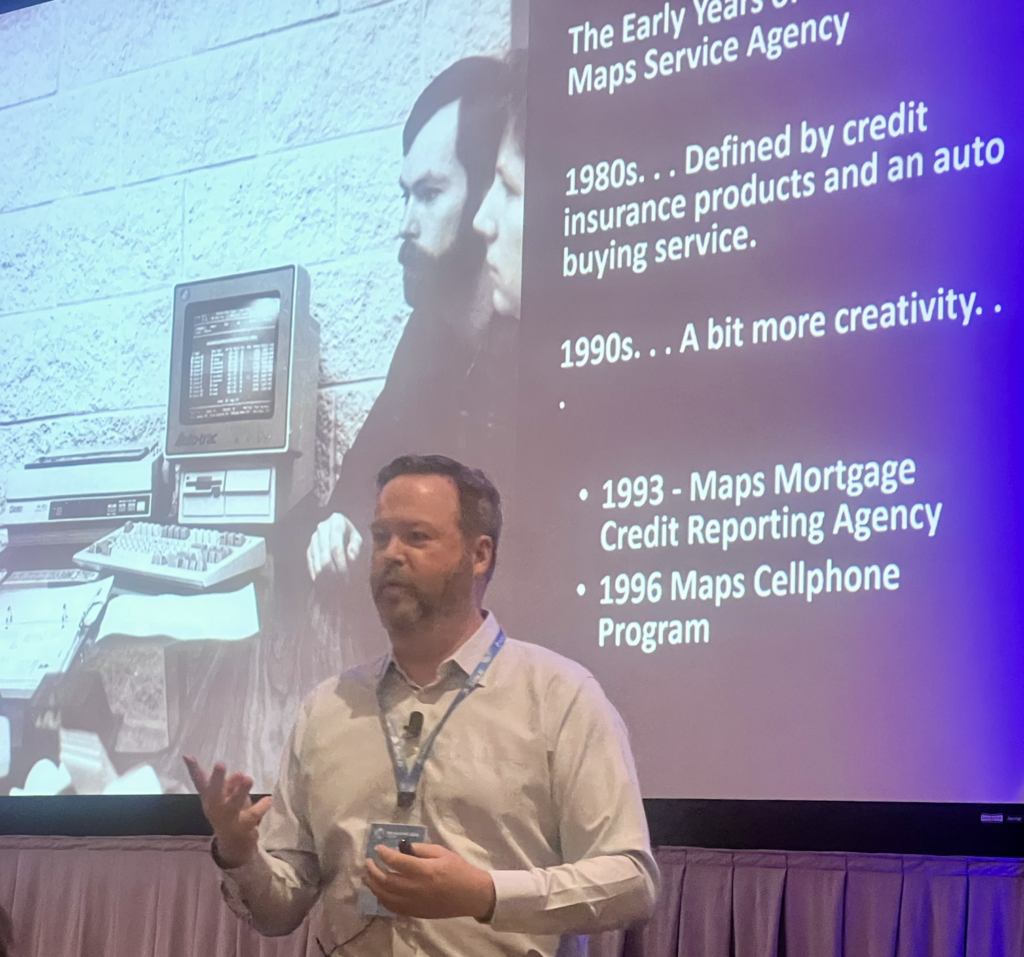

Founded in 1935, Maps began engaging with CUSOs in the 1980s, during a period when many Northwest credit unions were forming such entities, often focused on insurance products. In Maps CU’s case, in 1984 it formed Maps Service Agency. Zook said those efforts were influenced by industry figure Gary Sandifer, who helped popularize the model in the region.

Early offerings included a range of insurance products—some innovative, others less successful—but they laid the groundwork for broader experimentation.

By the 1990s, Maps expanded into new areas, including a mortgage credit reporting agency at a time when three-bureau reports were standard for home lending. A chance meeting in 1996 with executives from AirTouch, a precursor to Verizon, led to one of the credit union’s most unusual ventures: selling mobile phones to members.

“That program was so good for us that in the first two years we had sold about 7,000 phones for a credit union of about 20,000 folks,” Zook said. “Sometimes we were like a cell phone provider with a credit union on the back end.”

At its peak, the program expanded to roughly 22 credit unions.

A Regulatory Crisis and a Turning Point

The credit union’s trajectory shifted dramatically in 1998 when the National Credit Union Administration required Maps to divest $22 million in investments tied to collateralized mortgage obligations. The forced sale, conducted during a down market, resulted in a $3 million capital loss.

“It was a financial disaster,” Zook said, noting the credit union’s capital ratio fell to 4.9% and triggered additional regulatory requirements.

Maps CU was ordered to shrink from just under $200 million in assets to below $150 million and cut approximately $1 million in expenses just to break even. With limited ability to grow on the balance sheet and pressure mounting, leadership even explored merger options.

“There was no work that really could be done on the credit union side to grow,” Zook said.

Instead, leadership turned to CUSOs as the path forward.

“There was one big answer to this…we had been marginally successful in CUSOs, and that was going to save the credit union,” he said.

Rebuilding Through CUSOs

Zook, then a young executive with a background in market research and strategy, was tapped to lead the effort.

“I knew nothing about CUSOs,” he said. “I said no to the job, and [the CEO] said yes—and he won.”

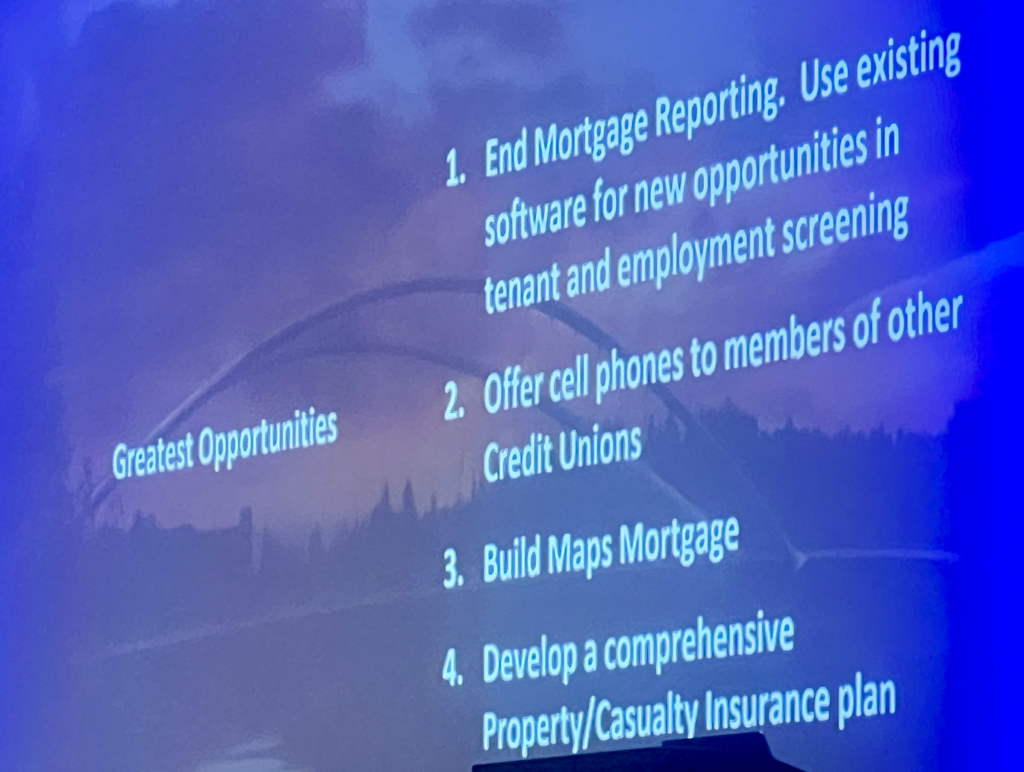

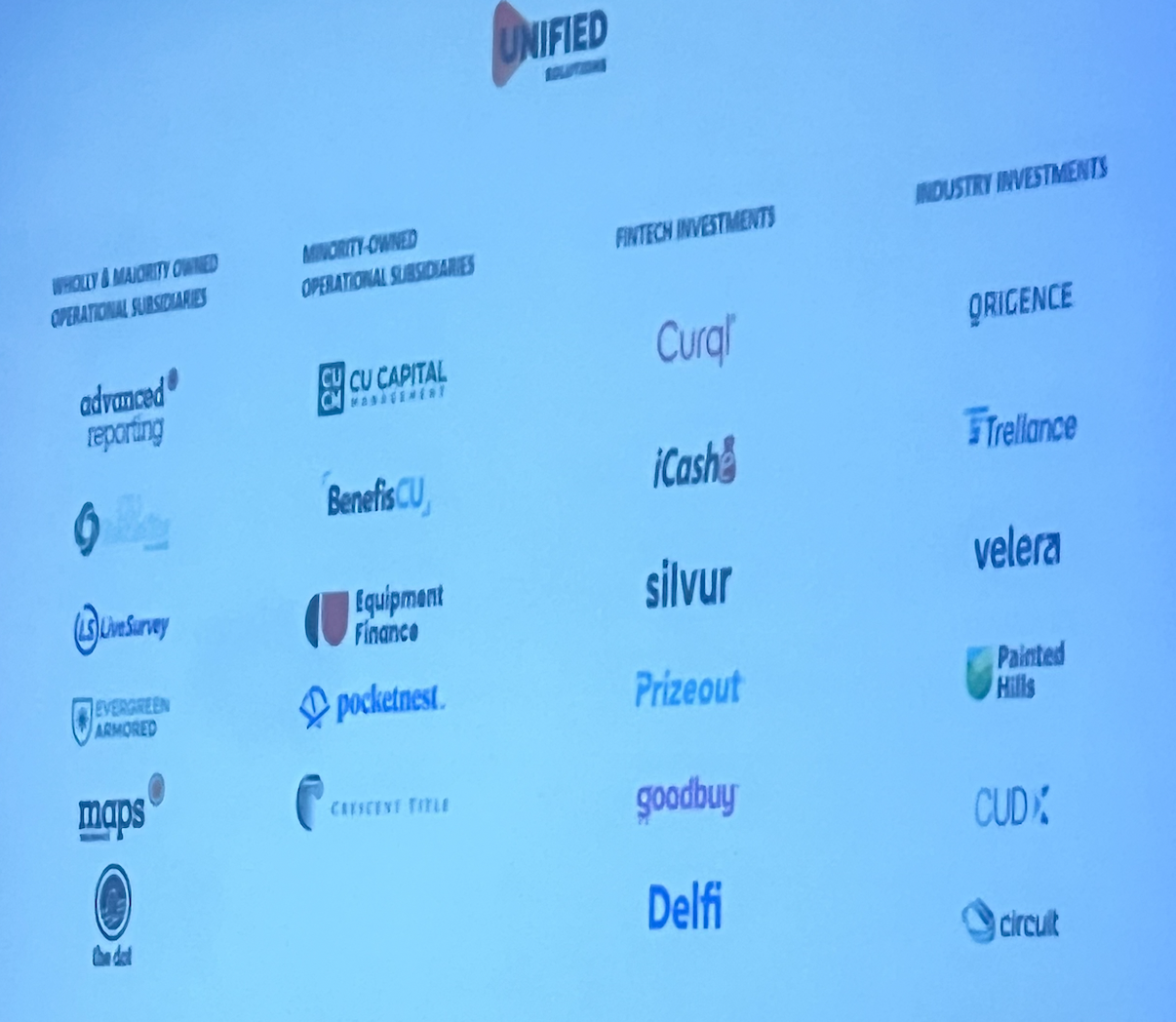

His first step was triage: eliminating or restructuring underperforming ventures. The mortgage credit reporting agency, which had lost $200,000 in just five months, was scrapped in favor of repurposing its technology into broader reporting services, which later evolved into Advanced Reporting, now serving roughly 1,000 companies.

Other moves included:

- Expanding the cellphone business to additional credit unions

- Launching a mortgage lending company, Maps Mortgage, in 1999 that eventually produced about 70% of the credit union’s net income

- Building a comprehensive insurance platform to replace earlier, unprofitable offerings in property, casualty.

“We needed to eliminate or redirect all of what I considered to be the bad,” Zook said.

Expansion, Collaboration and New Ventures

In the 2000s, Maps accelerated its CUSO strategy. It acquired its first property and casualty insurance agency in 2004 and later added several more. In 2007, it partnered with nine other credit unions to launch a multi-owner business lending CUSO.

Some ventures faded over time, but others expanded significantly. During the Great Recession, Maps launched a federally registered investment advisory firm focused on institutional investing for credit unions.

The credit union also became the first West Coast investor in Ongoing Operations, helping that company grow from a Washington, D.C.-based operation into a national CUSO before it became part of Trellance.

Zook acknowledged that not all ideas originated under ideal circumstances.

“I would say never start a CUSO in anger,” he said. “But I’m violating my rule here.”

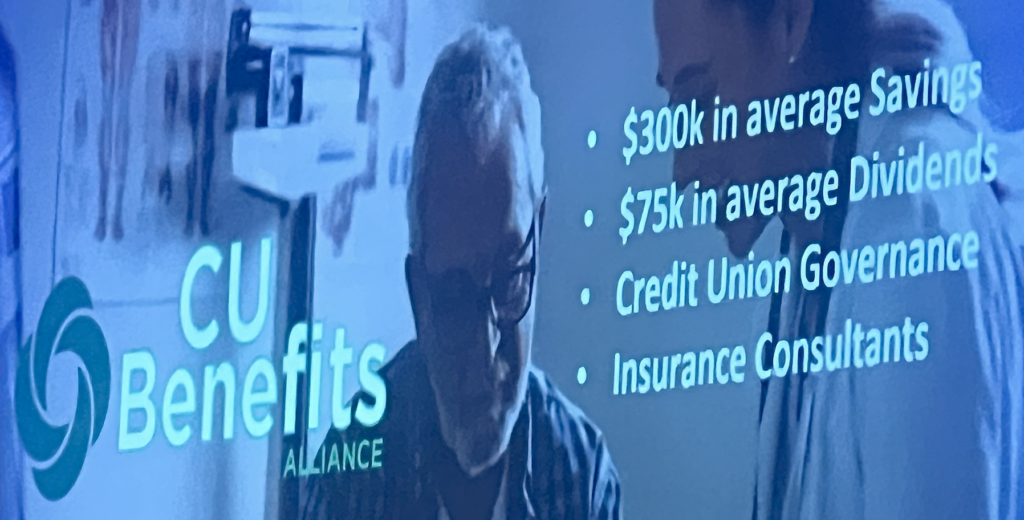

One such venture—formed out of frustration with vendors including Allied and CUNA Mutual—ultimately attracted 40 credit union investors and performed well. Zook later bought the company back to reposition it as CU Benefits Alliance, focusing on healthcare solutions.

“Every single time the credit unions came forward, they had one question: how do we solve for medical benefits, because they’re killing us,” he said.

Today, CU Benefits Alliance saves participating credit unions an average of about $300,000 annually, with collaborative owners receiving approximately $75,000 in dividends.

Innovation Driven by Necessity

Zook described another pivotal innovation during the financial crisis, when rapid deposit growth threatened to push Maps into Prompt Corrective Action due to capital constraints.

Sitting with his father, he recalled hearing a simple suggestion.

“Too bad you don’t have something to sell,” Zook said. “I thought, my God, I do have a building.”

Maps sold the building to its members and leased it back, offering a 6.5% return at a time of low deposit rates. The strategy helped recapitalize the credit union within three years. The concept later influenced broader industry approaches, including the development of CU Capital Management.

Zook said that company is now “probably the best company in the space” for unlocking capital tied up in real estate.

Newer Ventures and Ongoing Strategy

In 2020, amid the COVID-19 pandemic, Maps launched Evergreen Armored Transport, targeting what Zook described as one of the industry’s most persistent vendor problems.

“You ask anybody what is the biggest pain point from a vendor relationship, and they will often say it’s your armored transport,” he said.

The company operates through regional partnerships, with multiple credit unions helping capitalize operations and build routes before expanding services to other financial institutions. Maps plans to expand into additional regions, including the Southwest and Great Lakes.

Other recent investments include CU Capital Management and even a coffee shop launched in 2025 to enhance member and employee experience—though not intended as a profit center, it is owned through a CUSO structure.

Philosophy: Collaboration and Discipline

Zook said Maps views CUSO investments through two frameworks: income statement strategies, which generate ongoing returns, and balance sheet strategies, which explore new ideas and long-term value creation.

“The reality is the best ideas…come from the biggest pain points that our operations have,” he said.

He emphasized that collaboration is essential.

“Generally, just don’t go alone,” Zook said. “The power that we have is in scale. Power is in collaboration.”

At the same time, Zook stressed the importance of knowing when to step back from a venture.

“Sometimes you realize you’re not the right parent for that company,” he said, noting that selling or repositioning a CUSO can allow others in the industry to take it further.

Returns and Mission

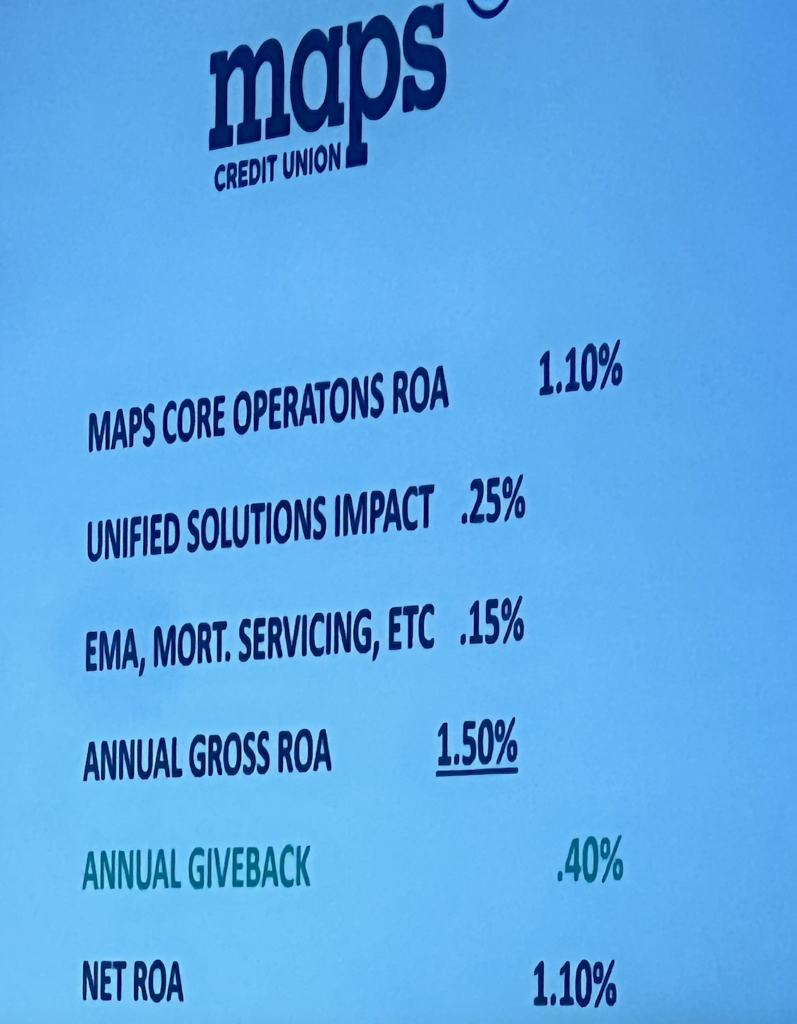

Today, the financial impact of Maps’ CUSO strategy extends beyond profitability. The credit union distributes roughly one-third of its return on assets annually across three groups: members, employees and the communities it serves.

“Our mission as an organization is give back,” Zook said. “We try to give back about a third of our ROA every year.”

That includes member givebacks, profit-sharing compensation for employees and executives, and community investments.

For Zook, the lesson from decades of CUSO development is that collaboration-driven innovation can both stabilize and transform a credit union.

“That leads to shaping our industry in a way that we financially control our destiny,” he said.