DES MOINES, Iowa — A new analysis of 2025 Home Mortgage Disclosure Act data shows the mortgage market is regaining momentum after a prolonged downturn, though growth remains uneven and concentrated among a small group of lenders.

According to iEmergent, total U.S. mortgage volume rose in 2025, driven largely by refinancing activity and higher loan balances rather than a broad-based recovery in home purchase demand. The findings were released as part of iEmergent’s Mortgage MarketSmart analysis.

Top Takeaways

iEmergent said the top takeaways from its analysis include:

- Refinance activity drove a disproportionate share of volume growth.

U.S. lenders originated approximately 6.75 million loans totaling $2.12 trillion in 2025, up from $1.82 trillion in 2024, according to iEmergent. Refinances climbed to $610.4 billion, accounting for 29% of total lending volume, compared with 22% the prior year. The firm said the increase suggests recent gains are being fueled more by rate-driven activity than by underlying purchase demand. - IMBs extended their lead in both share and growth capture.

Independent mortgage banks increased their share of originations to 57.8% in 2025, up from 55.8% in 2024, and accounted for 61.9% of total lending volume. They captured $193 billion of the market’s $303 billion year-over-year growth, far outpacing depository institutions, and represented 18 of the top 25 lenders by both loan count and dollar volume. - Rising loan sizes continue to pressure affordability.

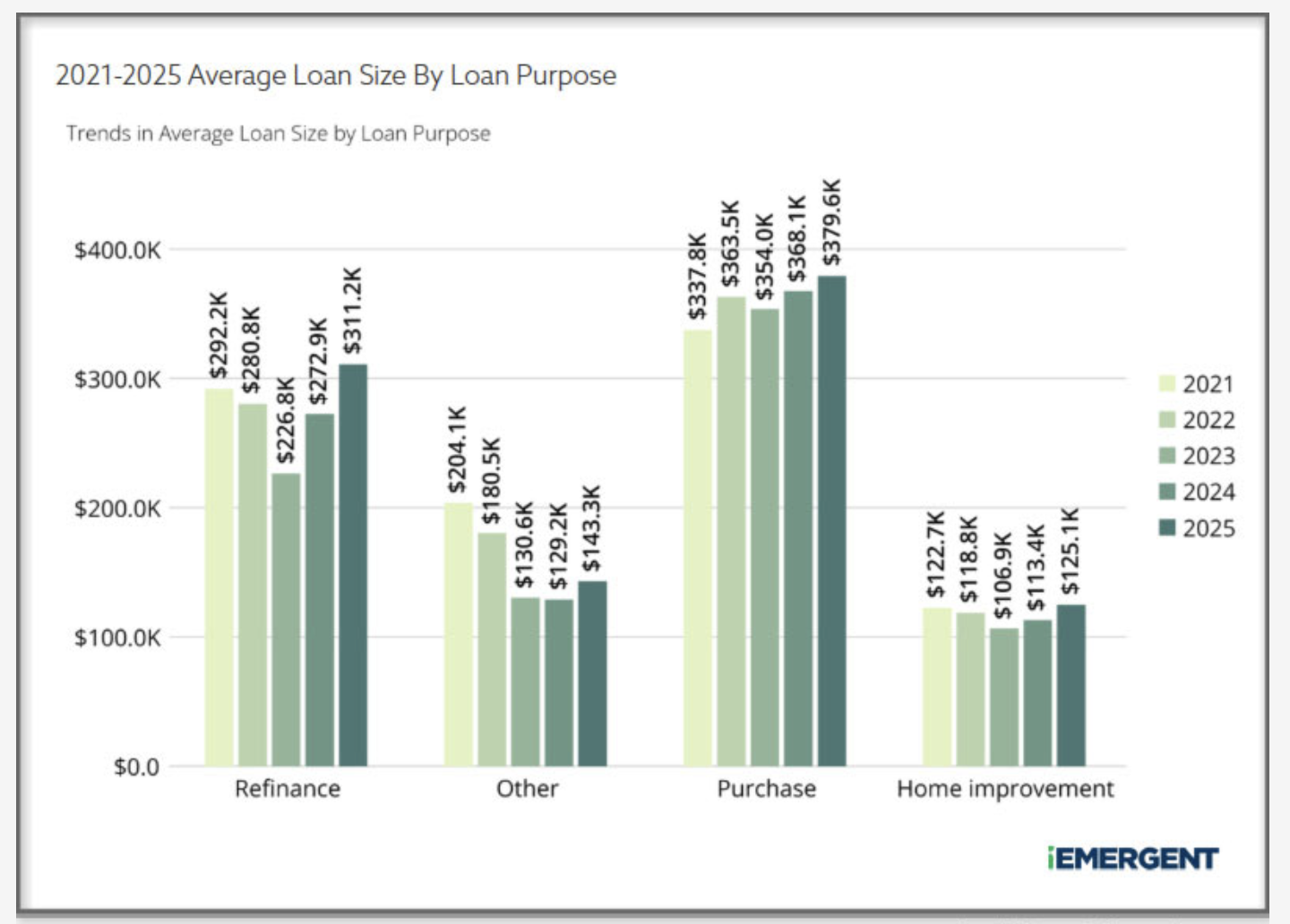

Average loan sizes increased across both purchase and refinance segments. Purchase loans rose to $379,600 from $368,100, while refinance loans increased to $311,200 from $272,900. iEmergent said persistent inventory constraints and elevated home prices are pushing borrowers toward higher balances and limiting access for more price-sensitive buyers. - Denial rates edged down, but elevated fallout points to ongoing borrower friction.

While denial rates declined modestly, overall application fallout remained high. About 40% of applications from non-Hispanic White borrowers did not result in funded loans, while fallout exceeded 50% for Black, Native American/Alaskan and Pacific Islander applicants. The firm said increased withdrawals and incomplete applications point to affordability constraints and valuation challenges disrupting the origination process. - Market concentration remains high, with production concentrated among a small group of lenders.

The top five lenders accounted for just over 20% of both loan count and total volume in 2025. More broadly, only 47 lenders — roughly 1% of all institutions — originated half of total mortgage volume, underscoring the importance of scale and operational efficiency. - Loan purpose mix varies significantly by geography, reinforcing the need for localized strategy.

Purchase-driven markets in the Sun Belt, such as Houston (71% purchase) and Austin (68% purchase), contrast with coastal markets like Los Angeles (40% refinance) and San Diego (38% refinance). iEmergent said the differences highlight the need for market-specific strategies.