WASHINGTON — Credit union loan growth slowed sharply during the first quarter of 2026, with most of the industry’s expansion concentrated among the nation’s largest institutions—which has been an ongoing trendline, as the CU Daily has been reporting–according to a new analysis released by Forvis Mazars.

In its “Credit Union Performance Trends: Q1 FY 2026” report, Forvis Mazars said loan growth across all credit unions slowed to 1.7% on an annualized basis during the quarter, down from 4.4% in the fourth quarter of 2025.

The analysis, based on NCUA call report data, found larger credit unions with more than $10 billion in assets continued to post strong loan growth, while smaller institutions struggled to maintain momentum.

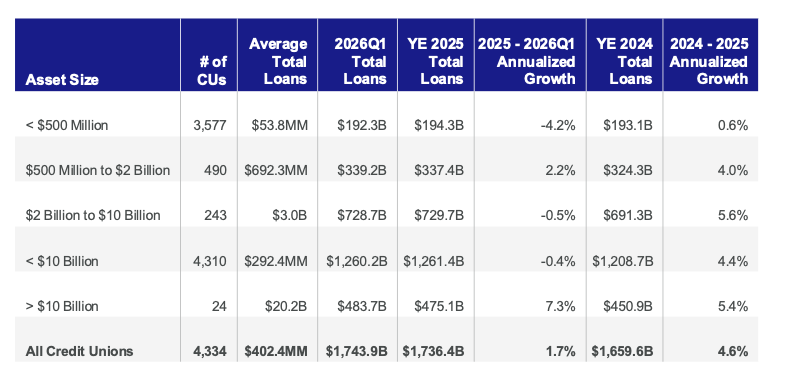

According to Forvis Mazars, total loans outstanding at 4,334 credit unions reached $1.744 trillion as of March 31, an increase of $7.4 billion from year-end 2025 and $84.3 billion from the end of 2024.

Among credit unions with less than $10 billion in assets, total loans declined by $1.2 billion, or 0.4% on an annualized basis, during the quarter, the report said. Credit unions with more than $10 billion in assets reported annualized loan growth of 7.3%.

Commercial, Real Estate Lending Continue to Grow

Forvis Mazars said growth continued to be driven by 1-4 family real estate lending and commercial real estate lending.

The report said commercial loans have been the fastest-growing loan segment for credit unions since 2023, particularly among institutions with less than $10 billion in assets.

According to the analysis:

- Commercial loans and lines of credit at credit unions under $10 billion increased by $33 billion from year-end 2023 through the first quarter of 2026.

- Commercial loans now represent 13.1% of total loans at those institutions.

- First-lien 1-4 family real estate loans totaled $432.7 billion during the quarter.

- Junior-lien residential real estate loans reached $137.2 billion.

- Commercial real estate-secured loans totaled $151.6 billion.

Forvis Mazars warned that growing concentrations in commercial real estate lending could increase risks tied to geographic regions, industries or borrower types and potentially stretch underwriting and risk management capabilities at institutions traditionally focused on consumer lending.

Brad Snider, managing director of loan review and credit risk services at Forvis Mazars, said in the report that as member business lending portfolios grow and diversify, oversight and risk management expectations also increase.

Margins Plateau as Loan Yields Ease

The report said net interest margins, loan yields and deposit costs are beginning to plateau after rising since 2022.

For credit unions with less than $10 billion in assets:

- Net interest margin measured 4.43% during the first quarter, down slightly from 4.46% in the fourth quarter of 2025.

- Loan yields declined to 5.97% from 6.09%.

- Cost of funds declined to 1.87% from 1.99%.

- The loan yield-to-cost-of-funds spread remained unchanged at 4.11%.

Forvis Mazars said maintaining and increasing margins could become more difficult as loan yields plateau, adding that attracting lower-cost core deposits could help mitigate pressure on earnings.

Asset Quality Improves

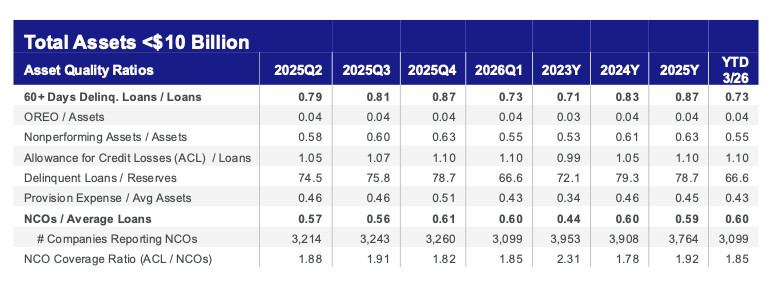

According to the report, asset quality improved during the first quarter of 2026, with delinquency rates, provision expenses and nonperforming asset ratios all declining quarter over quarter.

Forvis Mazars said that among credit unions under $10 billion in assets:

- Loans 60 days or more delinquent fell to 0.73% of total loans from 0.87% at year-end 2025.

- Provision expense to average assets declined to 0.43% from 0.51%.

- Nonperforming assets to total assets improved to 0.55% from 0.63%.

- Net charge-offs remained elevated at 0.60% of average loans, though slightly below fourth-quarter levels.

The report said credit unions should continue evaluating collections effectiveness, workout strategies and recovery processes to reduce loss severity and improve portfolio performance.

Matt Wainscott, senior manager of loan portfolio and capital stress testing at Forvis Mazars, said in the report that credit unions should perform loan portfolio and capital stress testing at least annually to ensure adequate capital levels under deteriorating economic conditions.

Profitability Improves Slightly

Forvis Mazars reported profitability improved modestly during the quarter, while capital ratios declined slightly from year-end 2025 levels.

Among credit unions under $10 billion in assets:

- Return on average assets increased to 0.66% from 0.63% in the fourth quarter of 2025.

- Operating expenses as a percentage of operating revenue rose to 79.3% from 79.0%.

- Net worth to total assets declined slightly to 12.45% from 12.51%.

The report said profitability remains essential for supporting future expansion and strategic initiatives, adding that credit unions should prioritize operational efficiency, technology investments and member experience enhancements.

Some Areas See Acceleration

In its conclusion, Forvis Mazars said the first quarter reflected a continuation — and in some areas an acceleration — of trends that emerged in late 2025.

The firm said management teams should focus on preserving margins through disciplined loan pricing, active deposit management and ongoing evaluation of funding mixes, while maintaining close attention to credit monitoring and capital management.

The Recommendations

Among the recommendations outlined in the report:

- Refine loan growth targets to align with funding capacity.

- Stress test deposit sensitivity under multiple rate scenarios.

- Maintain conservative allowance and capital planning assumptions.

Chad Garber, national credit union industry leader at Forvis Mazars, said in the report that the data continues to demonstrate the strength of the credit union model despite ongoing growth pressures.