PALM DESERT, Calif.–The CEOs of four credit unions have shared their perspective on numerous lending-related issues, including how they are working to improve their lending processes, weighing in on the long-time challenge of turning indirect members into more engaged members, and admitting that while many dealers want to do business with credit unions, “they don’t need us as much as they used to

The conversation took place during a panel discussion titled The Future of Financing” at Origence’s Lending Tech LIVE event. The panelists for the session, which was moderated by Steve Williams, CEO and partner with Cornerstone Advisors, included:

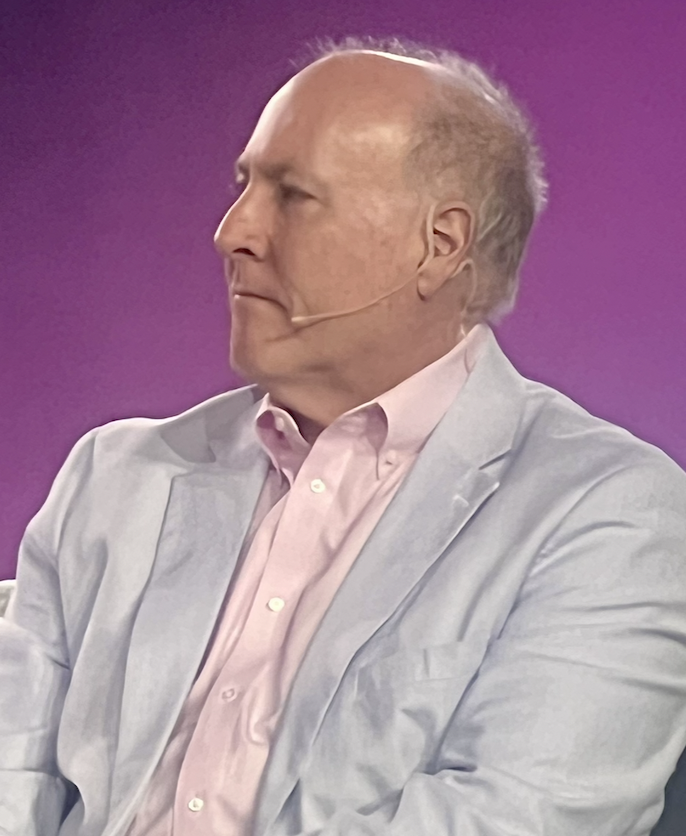

- Tony Boutelle, president and CEO of Origence

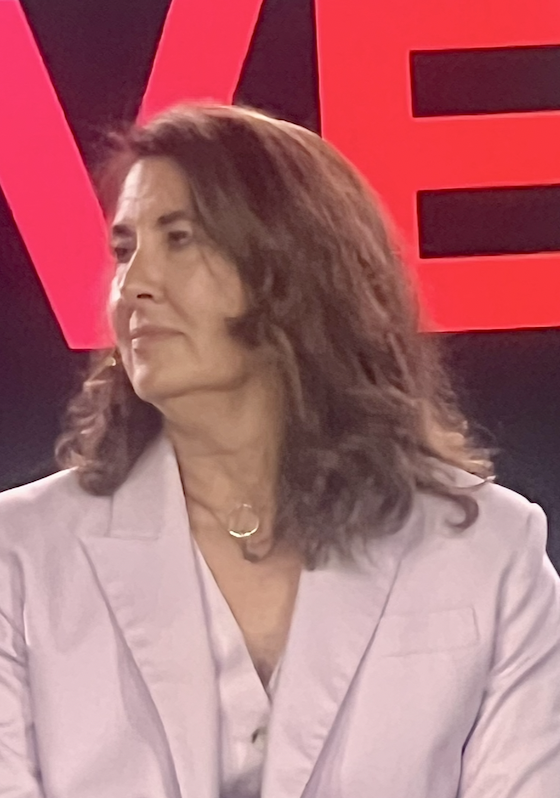

- Steph Sherrodd, president and CEO of Sunward Federal Credit Union

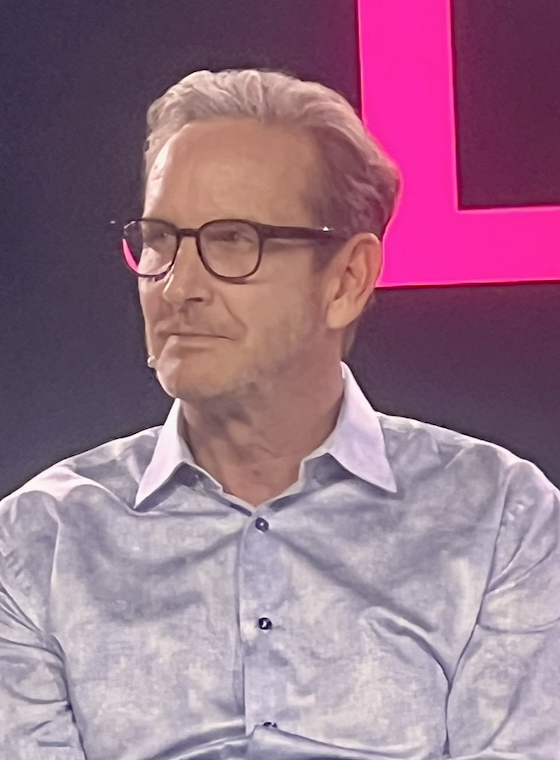

- Bill Cheney, president and CEO of SchoolsFirst FCU

- Bob McKay, president and CEO, Together Credit Union

Below is a look at some of what was discussed:

Williams: We are member-driven organizations. How do we turn the indirect channel into true, engaged members? What are you doing?

Sherrodd: It is so important. At Sunward, one in five members became a member through the indirect channel. It’s the biggest front door we have. For us, it starts with a call on day one, making sure we have a warm connection. And then a call 30 days later for a more thorough financial discussion. It’s that connection early on that creates growth.

Cheney: We do indirect lending a little bit differently at SchoolsFirst. You actually have to already be a member to get a loan at a dealer. Expanding relationships with our members is a huge deal for us. Working with Origence and its dealer network, we have preapprovals for when they get to the dealership. Origence enables that. We have 1.6 million members.

McKay: It’s our largest source of members, as well. We’ve not done a great job of turning them into active, productive members. We get about 10% using another product. One of the things we’re doing is partnering with our AI partner, Posh, on a new outbound effort to scale this better, to at least get warm leads.

Williams: What gets you excited about this Holy Grail?

Boutelle: It’s been a 30-plus-year dilemma. Members go to the dealer to get a car, not financing. That’s why 80% of financing is done at the dealership. We want to help dealers grow that. About 11% of indirect members become more active members. It is definitely something that’s important. I know there are a lot of credit unions in the 25% range. You will never get to 100%, but we should be able to get beyond 11%.

Williams: CU lenders are competing with the experiences of a Chime or an Apple. What part of your digital experience have you been working on, and what parts still kind of suck?

McKay: We are right in the middle of converting to Arc OS (from Origence). There is a lot of room for improvement for us.

Cheney: It’s continuous improvement on the digital experience for us. One, we are trying to close the gap with what members can do at a branch or contact center and what they can do in mobile. Forced channel switching is not good, and that’s not what we want. Chime doesn’t have branches. We have to fix some legacy issues. We are also rethinking, reengineering and rebuilding our consumer loan experience so you have the same experience online or mobile that you have talking to our wonderful employees.

Sherrodd: We are also focused on getting digital to be a similar experience to what is available in the branch. We have been particularly focused on consumer lending so you can go from end to end without us getting engaged in the process. That’s table stakes today.

Chime is not in the local market. They’re not raising money for the University of New Mexico Hospital. We are trying to make sure we leverage the fact that we are part of the community.

Williams: There is no perfect origination system. What excites you now about this generation?

Boutelle: AI is making it so much easier to build things quickly and to test things. The new CUDL Rate Hub was done in one night using Claude. What you need to know is how to ask a really good question to get a really good answer. I’m really excited about that.

I think most people would not like to spend four or five hours to buy a car. Tesla and Carvana have started with getting a lot of the financing done online before you get to the dealership. I think that experience is going to improve. We’re trying to make it so we are wherever you are when you need a loan.

Williams: You are all Origence board members. In the next 12-24 months, what would you really like to see come out of Origence?

Sherrodd: When we’re thinking about the future, we’re thinking about what our members are going to be thinking about and how they’re shopping for cars. Tony and his team are really thinking about where the consumer is going to go and how they can build the relationships. The collective power of our credit unions on a platform speaks with a very loud voice.

Cheney: We just went live on FIConnect and are having early success. It’s a way we can serve our members that didn’t exist before. Hats off to Origence for getting out ahead of that. It’s an opportunity to broaden our reach. As a board member, what we have heard here from the dealers is they are seeking to be more efficient, or shall we say, increase their revenue, by reducing the number of lenders they work with. That’s a big deal. FIConnect can be part of the answer. I think in the next 24 months that’s a big challenge: How do we work as best we can with automation? And how do we position CUDL and Origence with these dealers to be a part of their futures?

Williams: Speaking of dealer consolidation, as they roll up as an industry and flex their muscle, what’s the experience that those lenders that are the best? What should we be taking back to our boards and executive teams about this chessboard?

Boutelle: As you heard from the dealers (see separate reporting in the CU Daily), relationships are critical. They really are investing in the tech stack, too, for a better customer experience. I really felt like the dealers who were here want to do business with us, but they don’t need us as much as they used to. It’s interesting that they are talking about treating their customers like we treat our members.

What’s also interesting is the ones that are centralized have a lot of opportunity to create efficiencies. The ones that are not do not. Depending on what community you are in, I do like what the dealers said about being community organizations. They do like that relationship we have. There are still only about 25% of all dealerships that are part of the big dealer groups.

Williams: Could credit unions aggregate our collective 120 million members just from a bargaining standpoint?

Cheney: I think this already exists. I don’t think AutoNation knows it. We are their No. 2 or No. 3 lender, $75 million or so, at AutoNation. I think a member at SchoolsFirst wants their loan through their credit union. I don’t think they are going to be satisfied being told they are going to be financed through Wells Fargo or Bank of America, or that they are going to have to go somewhere else to get the car. How does that help AutoNation? We have fast-track dealers on our website; AutoNation will no longer be a part of our list.

Sherrod: It speaks to the power of the cooperative. This is credit unions working together; that’s Origence. As large dealers consolidate their lenders, we need to aggregate our buying power.

Williams: What do you hope everyone leaves with, and where do you want to see conviction on working together?

Boutelle: One thing that happens every year after Lending Tech LIVE is we see a bump in credit unions making more loans. Right now, lending is pretty flat. We hope to see more of our tools deployed to help make more loans.

Williams: What can be done to get e-contracting done?

Boutelle: I know credit unions in common communities feel like they compete against one another, but this is one opportunity where, if all credit unions in one community got together and did e-contracting, that would speed this along.

McKay: I thought it was a pretty direct call to action when the dealer said, “If you’re not doing e-contracting, we’re not working with you.” Origence is one of the biggest collaboration efforts in credit union history. That’s why we’re here.