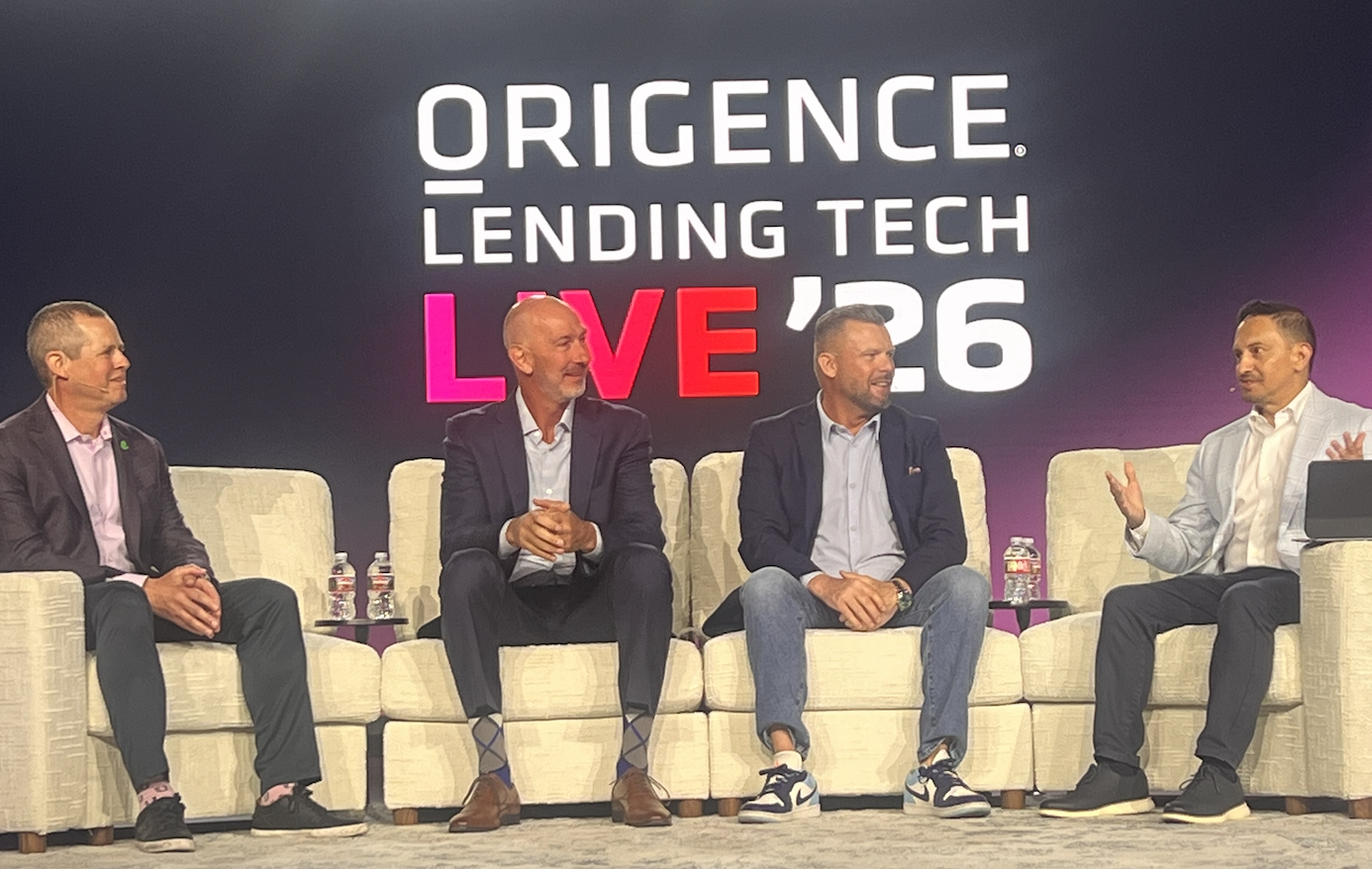

PALM DESERT, Calif.–Representatives of some of the largest auto dealerships in the country told CU auto lenders here they need to get on board with e-contracts (or else), shared reasons why some CUs rate highly with them as partners and others do not, and offered some forecasts for what they see coming down the road.

The auto dealer panel, which is one of the most popular discussions annually at the Lending Tech LIVE event hosted by Origence, included as panelists:

- Mark McAndrews, AVP-Enterprise Car Sales, which has 169 locations in 40 states

- Mike Fealey, F&I director, Litha Auto Sales, which has more than 500 dealerships worldwide

- James Hutmacher, senior director of F&I Operations, Garff Automotive, which has 73 dealerships ins nine states

The three panelists represented three of the 10 largest dealerships in the United States. The session was moderated by Josh Amaton, SVP-dealer solutions with Origence.

Below is a look at what was discussed:

Amaton: Preowned vehicles are critical to the car market. When it comes to consumer affordability, from where you are sitting, what are you seeing from your customers with the rising costs of insurance, interest rates and fuel prices? How is that impacting sales?

McAndrews: All of these outside factors have had an impact. From the rental perspective, we went from operating normally during COVID to suddenly sitting on roughly 700,000 vehicles. We didn’t even know where to park them. We had some real challenges.

Then we went into the chip crisis, which also turned into inflation. Our average vehicle was around $21,000 from a retail perspective, and that went up to about $28,000 within a 15-month period. The good news is that things are starting to settle in.

The bigger difference is mileage. A typical used vehicle used to have about 28,000 miles on it. Now it’s in the 40,000-mile range. But that’s much better than at the peak, when we were seeing vehicles in the 60,000-mile range. We believe we’re going to see a more traditional used-vehicle market, with a little bit of a dip and a larger spread between used and new vehicles. There are still a lot of outside factors that are beyond our control.

Fealey: To combat prices, we are selling a lot more used cars. I feel that’s where our growth is going to come from. We have a lot of stores in the Northwest where longer loan terms are helping offset those higher prices.

Last quarter, 75% of our loans were 72 months or longer. We’re keeping a lot more used cars that we previously would have wholesaled.

McAndrews: Sticker shock is real. We installed defibrillators in all of our showrooms.

If you look at new and used car prices pre-COVID versus now, it really is a shock. I remember when I thought a $500 car payment was high. We have people every day leaving with $1,000 payments. So, getting great terms on those loans is really important.

The other thing is that while we’re selling some cars we used to wholesale, and it’s hard to get used cars today, we want to make sure the cars are prepared properly. That adds to the cost. We would rather have that than put a car on the road that isn’t ready.

Amaton: We have seen prices rise, stabilize and then rise again on used vehicles. Have prices been reset in a permanent way?

Hutmacher: I’m afraid to predict that right now. If the Fed reduces rates, that could change things. If rates stay where they are, it could make things more difficult. It’s hard to find used vehicles. There simply are not enough of them. We partner with Enterprise, but it’s still very difficult.

Fealey: Sourcing used cars right now is hard. We’ve had dealers camp out in Walmart parking lots asking people if they are looking to sell their cars. I think the market is still volatile and is going to move up and down for the foreseeable future.

Amaton: The CFPB has essentially been neutralized. What other federal regulatory concerns do you have?

McAndrews: The FTC is coming at dealers really heavily right now. Some states are putting restrictions in place that make it harder to sell a car.

We want to do business the right way. I’m not worried about us operating outside the lines. But if regulators continue putting these onerous requirements on us, it raises the cost of vehicles. As far as compliance goes, we deal with it every day. Several dealer groups have had to pay fines of several million dollars due to compliance issues.

Fealey: We are a big target. We have to have our i’s dotted and our t’s crossed.

We are not worried about the CFPB because we have always tried to treat every customer the same way. Every customer is fully educated before they come into the dealership.

Now it’s more FTC-related, with advertising requirements, pricing disclosures and storing information for seven years. Regulators think they are doing what’s best for the customer, but in reality it raises prices.

McAndrews: We are fortunate in that we don’t have any interest-rate markup. But the state level is where things get really interesting, such as in California with the CARS Act. It’s now more about how things are disclosed than about process changes. States are really stepping in where the CFPB stepped out.

Amaton: Especially since COVID, digital retailing has really changed the way consumers shop and purchase vehicles. It changes where that finance conversation happens. What is your expectation of lenders in that online marketplace?

Hutmacher: The expectation for us is that it be seamless. If a customer wants to buy a vehicle in pajamas from home, we want them to be able to do it. One thing that is difficult is that if the customer is a credit union member, many credit unions still don’t do e-contracting, so we have to send them a wet contract.

It’s all about speed, efficiency and security.

Fealey: Our motto is “wherever, whenever, however.” We have to be able to adapt. If you’re not e-contracting, I think you’re going to be left behind. When we look at it from the corporate level with 500 dealerships, when funds are floating out there for a few days, it can cost millions of dollars.

McAndrews: The key is that you want to be part of the front-end decisioning. If you’re not, you miss out. From a credit union perspective, you want to be on that front end. As a dealer, we want the customer to feel trust, convenience and transparency. About 50% of our traffic is online. The key is that when a customer comes into the dealership, they can pick up where they left off online.

We’ve found that people still like coming into the dealership, even though we can deliver vehicles to their homes. They just want to get through the process quickly.

Amaton: What is speed?

McAndrews: We want decisions completed in less than three minutes. About 85% are done in under 45 seconds. We don’t want to show declines. If someone is in a tougher credit situation, we want to provide an adjusted offer. The customer is not going to wait for you. Speed is incredibly important in lending.

Fealey: A minute or less is the decision time we look for.

We have a Driveway.com site where customers can shop online and apply for credit right there. We expect those decisions to come back in under a minute.

Hutmacher: Speed is everything. We live in an era of “I want everything now.” Even if there are clarifications needed, the process still has to move at the speed required to take care of the customer properly. The F&I person just wants to click and get a green approval. I’m all for making the customer experience as great and as fast as possible.

Amaton: What are you looking for in lender partnerships?

Fealey: We want a partner, not just another vendor or another lender. We want a true extension of us. We want flexibility and a single point of contact.

McAndrews: On our platform, we don’t have lender reps coming into our stores. We want strong support through pre-checks. We have our own credit policies with these lenders. On the back end, we want funding to be a very smooth process. We also want a single point of contact.

Hutmacher: Preferred lending is a huge and critical part of our business. For credit unions specifically, you should listen to this: preferred lending is where the industry is moving. We want that single point of contact. As a company, we want you to treat us like we’re a member.

When we look at preferred lenders, we ask whether they have the same moral character and operate the way we do. Are they going to be a benefit to us? We don’t want to have 60 or 70 lenders to send deals to.

The third factor is financial. After you meet the first two criteria, what does it mean financially to do business with you? Our hierarchy includes preferred lenders such as Bank of America and others that have programs specifically for the Garff organization. Below that are regional preferred lenders, including credit unions and banks with strong local relationships. The next level is captive lenders. Those are the people we have to do business with, including leases.

Credit unions come next. For us to include credit unions among our preferred lenders, they have to treat us like a member and it has to be profitable for us. We’ve seen situations where customers come to us from a credit union, and then a week later we get charged back because the credit union rewrote the contract. They think they are helping their member, but at the end of the day they’re not.

We like consolidation because we want that single point of contact. We want programs that are specialized for our customers. We like to get creative. Our partners do a great job. Preferred lenders have carte blanche in our stores.

Fealey: As far as the partnership goes, fraud is increasing at a crazy rate right now. We do every fraud check we can and still get burned. We can’t have a lender simply saying, “You need to buy this back.” We need to discuss it. Can we partner on this? We don’t need someone shoving it down our throats. It has to be a true partnership.

McAndrews: We’ve worked with credit unions for a long time and it has been a great relationship. But he’s right — fraud is on the rise. With fraud, it has to be a give-and-take relationship, like any true partnership.

Amaton: What about lender consolidation? What drives the decision to consolidate lenders?

McAndrews: In 2010, we took 175 regional agreements and reduced them to 12. It really helped us. It’s important that we have consistency. We went from 12 lenders down to eight and now back up to 10 as we continue to grow. It’s been important to have that commitment and recognize that you can’t be everything to everyone. You have to decide who you are and who you want to be.

We are working with Origence on FI Connect so we can present the customer with a single option and then, behind the scenes, place them with a credit union. It’s also an opportunity to gain membership. We are going to be testing this in California within the next 60 days or so.

Fealey: We are kind of unique in that we are not as top-down as some of our peer groups. I don’t think we’re going to drastically reduce our lender base. A dealer has to have a legitimate reason to add a lender. We then decide whether it’s a yes or no. If it’s a yes, they have to remove a lender we have already added.

Credit unions are necessary in many of the markets we serve, and I can’t be responsible for a dealer underperforming in a market because I removed a credit union. But never say never. Make sure you remain relevant and that your technology is up to date. If you’re not e-contracting, you will not be onboarded as a new lender.

Hutmacher: I want to make sure everyone understands that I’m not against credit unions. I’ve been a member of Navy Federal Credit Union since I was a teenager. I’m a big fan. My father was in law enforcement, and growing up, the credit union took very good care of us. I see credit unions operating in a way that our organization likes to operate. You are embedded in the community, and that’s how we like to operate as well.

Two years ago, we had more than 1,000 lenders that we did business with. We have now pared that down to fewer than 100. We always have two to three lenders in the same niche because we want it to be a horse race. We want them to compete. Our lenders pay us a management fee. We essentially become a representative for our 20 or so preferred lenders. We support them. We partner with them. We work together on issues such as fraud.

In return, our preferred lenders get more opportunities, and our customers get served even better. We will always have credit unions as part of that mix.

Amaton: What is virtual F&I?

Fealey: There are a couple of different models, and we are just getting into it. Obviously, you have to be able to e-contract to use that model. One model has the F&I manager in the store while the customer remains at home and never leaves the house. We have a store in Minnesota where 45% of deals are remote deliveries. We want that experience to be similar to the in-store experience, but without all the time involved. Another model has the F&I manager at home while the customer is in the store. We are going to experiment with different models, but I do think it is the way of the future.

Amaton: Amazon is now entering automobile sales. What do you think?

Hutmacher: Amazon has not yet impacted our business. I think it will have a bigger impact in the future, but I believe that is still a few years away.

Fealey: We have a few Hyundai stores that are part of the Amazon process. It hasn’t had a major impact so far. It’s still a bit clunky. There are a lot of things that need to be worked out. But I think it will be good for the business in the long run.

Amaton: If you could change one thing about credit unions, what would it be?

McAndrews: We partner with a lot of people in this room. I’m interested in feedback on what we can do better. I think we’ve already covered some of that. The competitors have shown that speed is really, really important. The second part is consistency. Understand how you fit into the business model.

Fealey: I would say that credit unions should treat dealers the way they treat their members. Sometimes it seems that credit unions value the member more than they value us. It’s a partnership. It’s a two-way street.

Hutmacher: It’s all about relationships. You have members in the community who want to finance with you. That’s not a problem. With our best credit union partners, we are actually driving new members to them. Without a true partnership, that doesn’t happen.

We do a lot of philanthropic events, and our credit union partners are involved in those. Likewise, we participate in their events. Credit unions are embedded in the community, and so are we. We don’t look at our 70 dealerships simply as dealerships. We view them as a way to provide thousands of people with opportunities to improve their lives.

We love doing promotions and driving additional traffic to our partners. Help us with our business, and we will help you with yours.