BOSTON — Cash-paying consumers and households with lower incomes effectively subsidize credit card rewards programs used disproportionately by higher-income Americans, resulting in an estimated annual transfer of more than $9 billion, according to a new study from Harvard Business School.

The working paper, titled “Who Pays for Rewards? Redistribution in the U.S. Payments System,” examined the growth of premium credit card rewards programs and the economic effects of interchange fees. The study found that merchants generally pass those costs on to all customers through higher prices, regardless of how they pay. As a result, consumers who use cash, debit cards or non-rewards credit cards help fund rewards earned by higher-income cardholders, according to the researchers.

Estimated Cost of $9.2 Billion

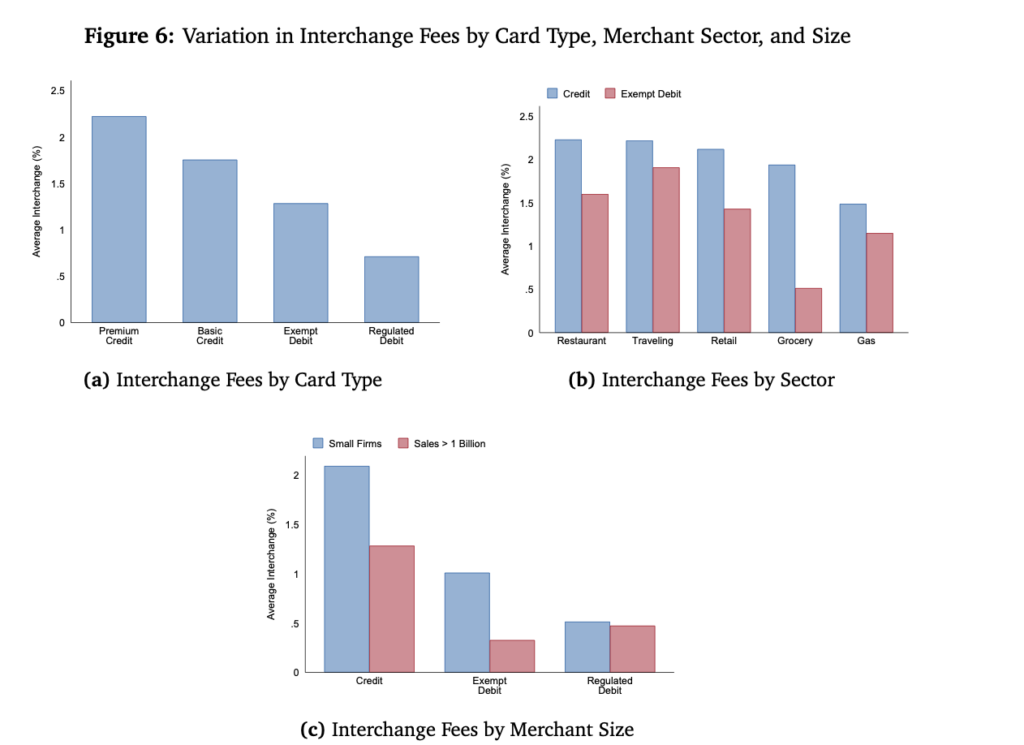

The Harvard researchers estimated the resulting redistribution from lower-income households to higher-income households totaled approximately $9.2 billion annually. The study found that while premium rewards cards accounted for about 15% of credit card spending in 2012, they represented roughly 60% of spending by 2023, reflecting the rapid growth of rewards programs.

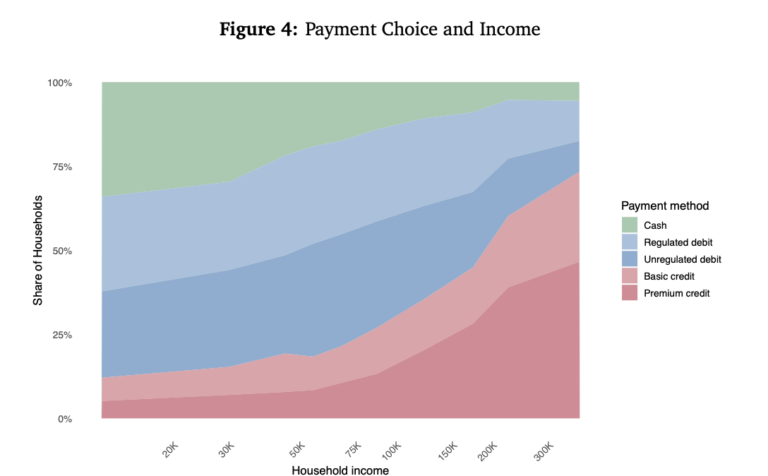

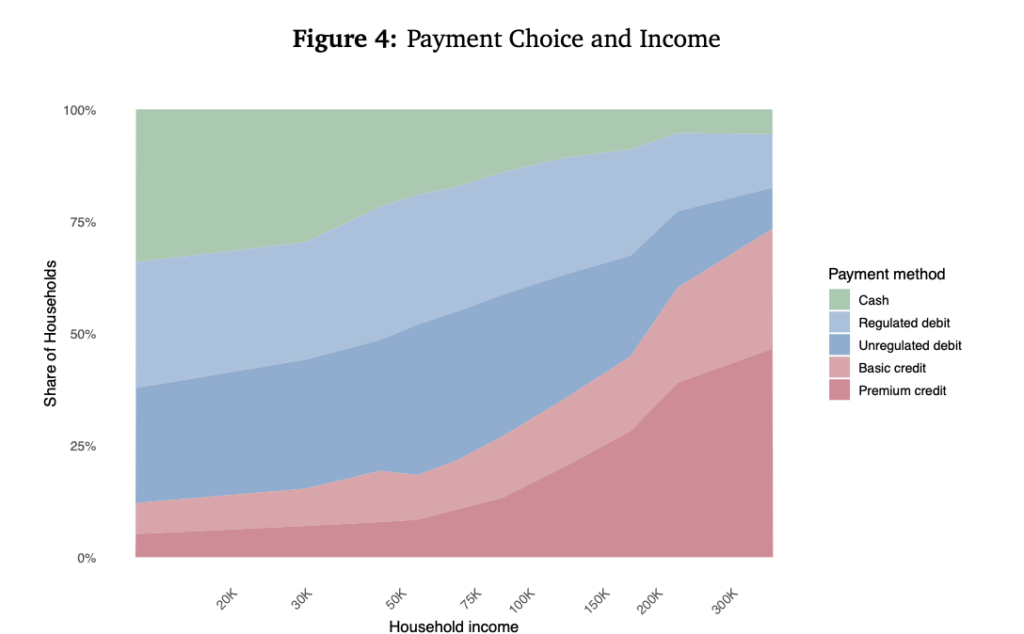

According to the study, higher-income consumers are more likely to qualify for premium rewards cards because of stronger credit profiles and higher spending levels. Those consumers receive cash back, airline miles, hotel points and other benefits funded in part by interchange revenue generated from merchant fees. Merchants, in turn, often incorporate those costs into prices paid by all shoppers.

Disproportionate Burden

The researchers found the burden falls disproportionately on consumers who do not receive comparable rewards benefits. Cash users, debit card holders and consumers with limited access to premium credit products often pay the same retail prices as rewards-card users while receiving none of the associated perks, according to the report.

The findings add to a long-running debate over whether credit card rewards programs create a “reverse Robin Hood” effect that shifts wealth from lower-income households to more affluent consumers, analysts said. Earlier research by economists at the Federal Reserve Bank of Boston similarly concluded that merchant fees can create a transfer from cash users to credit card users when those costs are embedded in retail prices.

Critics Respond

The Harvard study is already drawing criticism from some payments industry analysts and merchant fee opponents, who argue the researchers overstate the degree to which interchange costs are passed through to consumers and underestimate the benefits rewards programs provide across income groups. Critics contend that rewards cards have become increasingly common among middle- and lower-income households and that many consumers use cash-back rewards to offset everyday expenses.