ALEXANDRIA, Va.—An update on NCUA’s ongoing Deregulation Project was provided during the Thursday board meeting.

Offering the update was Amanda Parkhill, acting director of the agency’s Office of Examination and Insurance.

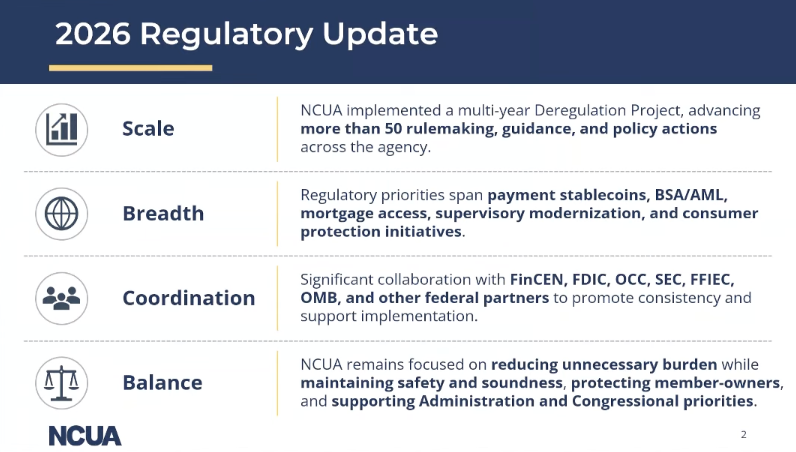

“There’s a lot going on and we anticipate over 50 rulemaking guidance and policy actions as a result of the deregulation project and other efforts taken to reduce burden and streamline processes,” said Parkhill. “These cover a wide variety of topics from new, innovative technology to long standing anti money laundering and consumer compliance requirements. Many of the actions we are working on involve coordination with other regulators to ensure that requirements are consistent among banks and credit unions.”

Parkhill said 31 proposals have been made as part of the Deregulation Projects, two of which are still out for comment.

“We are in very stages of finalizing several of the proposed rules,” Parkhill said. adding that objective is to wrap up phase one of the Deregulation Project by the end of this year or early 2027, at which point it will start on phase two.

“Phase one focused on rules that were obsolete, overly burdensome, duplicative or intended as guidance,” Parkhill said. “Phase two will include rules that may fall into one of those categories but were deemed as more complex, changes requiring more research or those that will have greater operational impact and require more planning.”

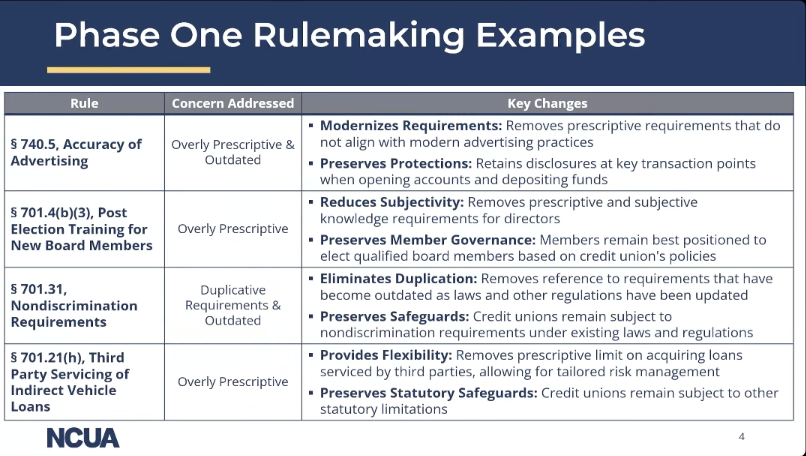

Four Examples Shared

As an example, Parkhill shared these four examples from phase one.

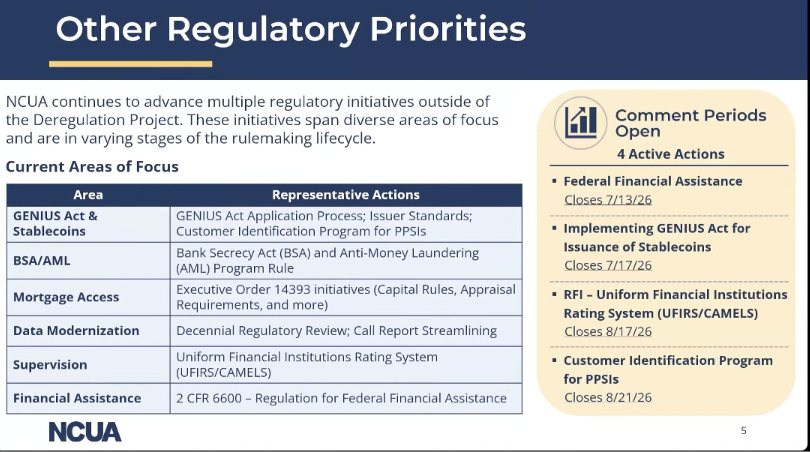

Parkhill also outlined a series of other regulatory priorities that are not part of the Deregulation Project, as outlined below.

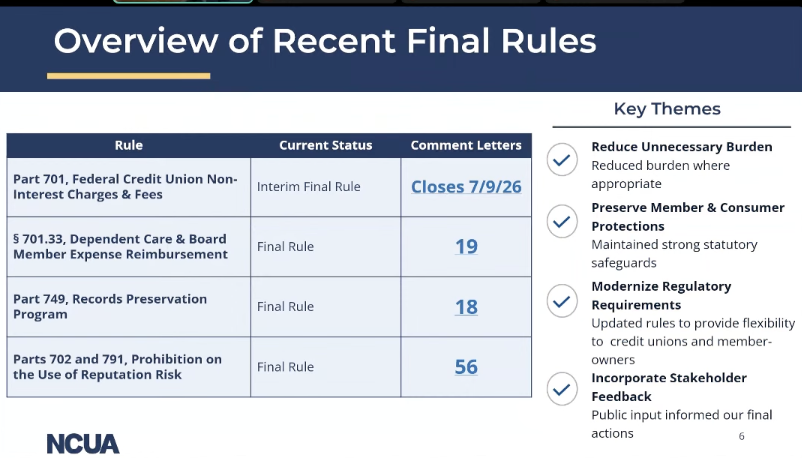

Parkhill also reviewed other final rules enacted by the agency, as seen in the graphic below.

Chair Invites Input

Hauptman, said NCUA continues to invite input as it “housecleans” and focuses on “safety and soundness.”

He cited two final rules, in particular, that he said deserve to be highlighted, including rules related to advertising and third-party servicing. He noted that old regulations related to print media reflect how much times have changed, as advertising in a newspaper now is a way to “hide the announcement rather than advertise it.”

In addition, he said many of the rules related to advertising were “overly prescriptive,” as were rules around third party servicing of indirect vehicle loans.

“NCUA doesn’t need to tell credit unions how to operate and manage their business unless there’s material risk involved,” he said. “We at NCUA do not run credit unions. When we give credit unions the flexibility to operate as they see fit without sacrificing safety and soundness, they’re better able to meet member needs.”