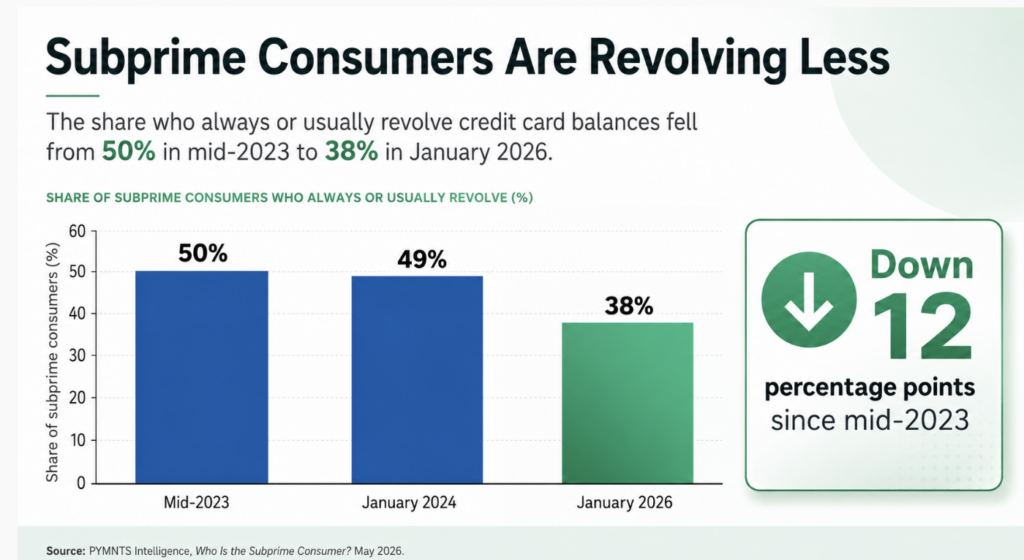

BOSTON — Fewer U.S. consumers with subprime credit scores are carrying credit card balances from month to month, a shift that suggests some borrowers are changing how they manage debt despite ongoing financial pressures, according to a new report from PYMNTS Intelligence.

The report, “Who Is the Subprime Consumer? A Behavioral Profile,” found that 38% of subprime consumers said they always or usually revolve credit card balances as of January 2026, down from 50% in mid-2023 and 49% in January 2024.

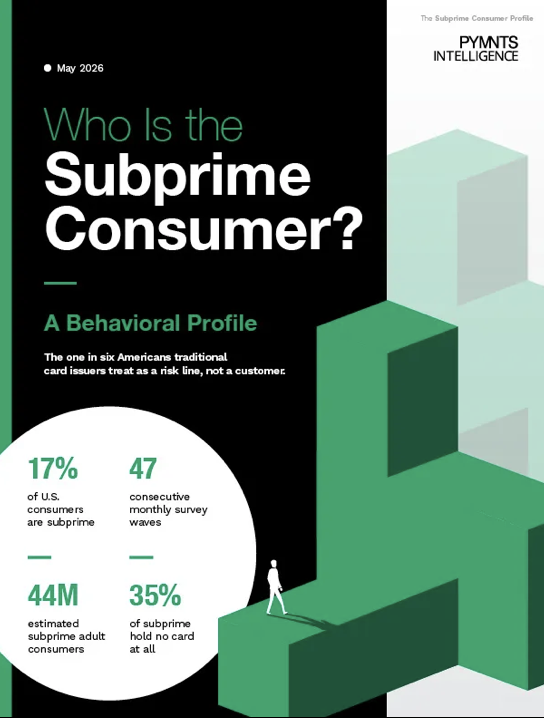

Subprime consumers account for about 17% of U.S. adults, or roughly 44 million people, according to the report. While the group continues to face cash flow challenges, researchers said many consumers are adjusting how they borrow and pay bills rather than relying as heavily on revolving credit.

Just 15% Pay in Full

The report found that only 15% of subprime consumers paid their credit card balance in full during the previous month. However, 45% said they paid more than the minimum payment but less than the full balance, suggesting many are reducing debt even if they cannot eliminate it entirely.

Researchers also pointed to changes in the types of credit products consumers are using. Thirty-five percent of subprime consumers reported having no credit or store card, while 4% said buy now, pay later was their only pay-later financing option. Nearly one in five subprime consumers, or 19%, used a buy now, pay later service in February 2026, compared with 13% of consumers overall.

The report suggests some borrowers may be shifting away from traditional revolving credit in favor of installment-based payment options.

Widespread Strain

Financial strain remains widespread among subprime consumers. According to PYMNTS Intelligence, 55% said they live paycheck to paycheck and struggle to pay bills. Among younger consumers in the group, 23% reported delaying a doctor’s visit because of the cost.

Tax refunds also remain an important financial resource. Sixty-seven percent of subprime consumers who received a tax refund described it as critical or very important to their financial well-being, the report found.