MADISON, Wis.–Loan growth among credit unions has accelerated in 2025 compared to 2024, new vendor contracts are driving up the expense ratio, and mergers are expected to “surge” over the next few years, especially among smaller credit unions, according to the new Trends Report from TruStage.

The Trends Report, which is now published quarterly rather than monthly, is based on data through June of this year and is compiled by Steve Rick, chief economist with TruStage.

Here’s a look at how credit unions performed by category, according to the new Trends Report analysis:

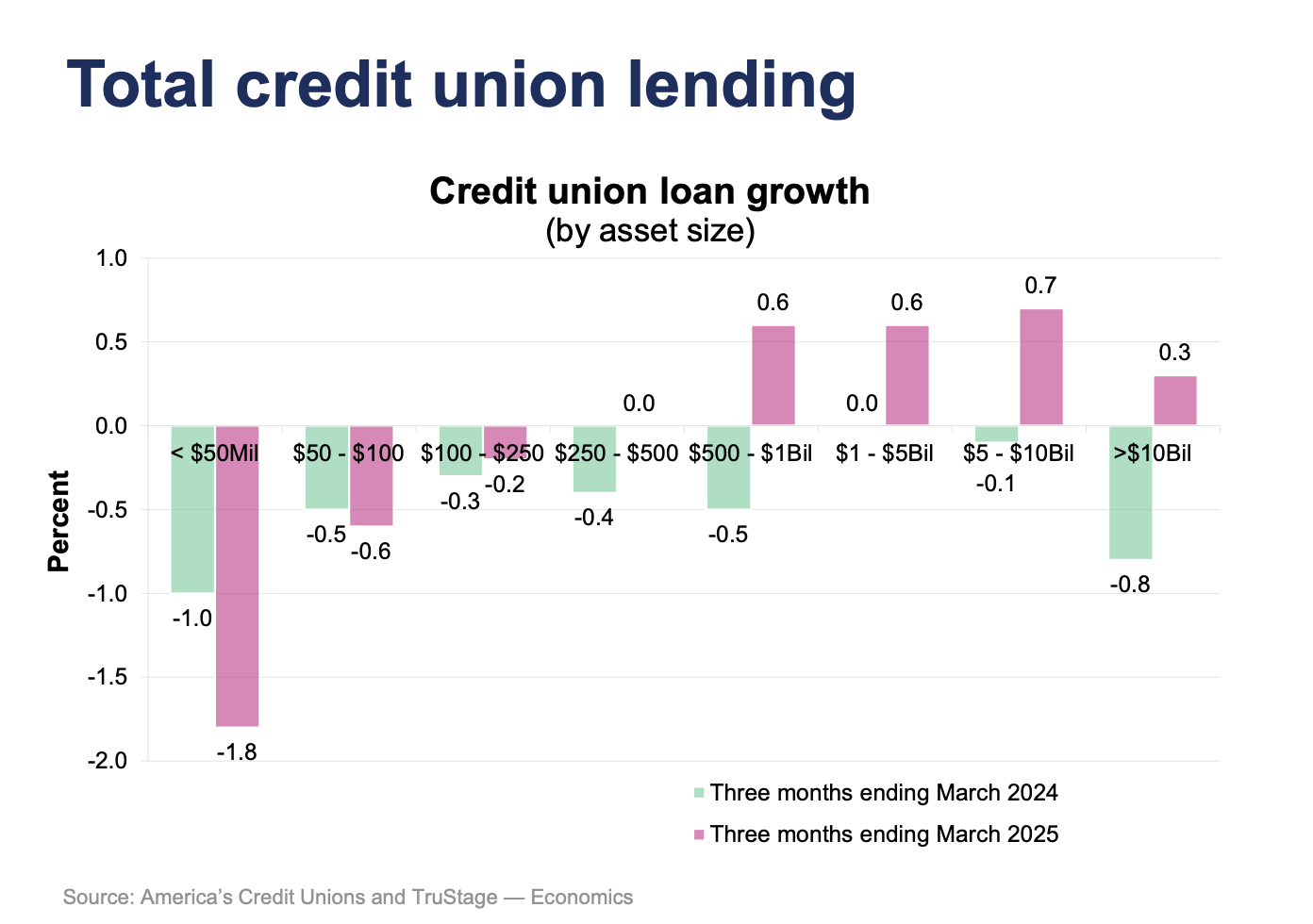

Total Credit Union Lending

The report notes that credit union loan growth has accelerated in 2025 compared to 2024.

“Credit union total loan balances rose 0.6% in the first quarter of 2025, above the 0.1% rise in the first quarter of 2024,” the Trends Report states. “Credit unions with assets exceeding $10 billion reported loan balances rising 0.30% in the first quarter compared to the 0.8% drop in 2024. Credit unions with asset less than $50 million reported loan balances falling 1.8%, versus a 1.0% drop in the first quarter of last year.”

According to the analysis, during the first quarter of 2025, loan balances rose 0.60%, above the 30-year average growth rate of 0.4%.

“There is significant seasonality in credit union loan growth, with only 6% of total annual growth occurring in the first quarter. The fastest growing loan category was home equity loan balances, which grew $2.1 billion (1.90%) in the first quarter,” the report states. “This constituted half of all loan balance growth and increased 19% during the last year.”

Credit union loan balances rose 4.8% in March, on a seasonally-adjusted annual rate basis, and 3.2% during the last 12 months.

“Expect credit union loan balances to rise only 5% in 2025 and 6% in 2026, which will be below the long-run average rate of 7.20%,” the report projects “Loan growth will be subdued due to high lending interest rates reducing the demand for credit and tight credit union liquidity reducing the supply.”

‘Long & Variable Lag’

In his analysis, Rick noted that the slowdown in both credit union and bank lending during the last two years is one of the “long and variable lags of tight monetary policy” that Federal Reserve Chairman Jerome Powell likes to mention at his press conferences to reduce the inflation rate.

“If inflation is caused by too many dollars chasing too few goods, then less lending will reduce the amount of dollars being created and spent, and therefore reduce inflation,” the report adds.

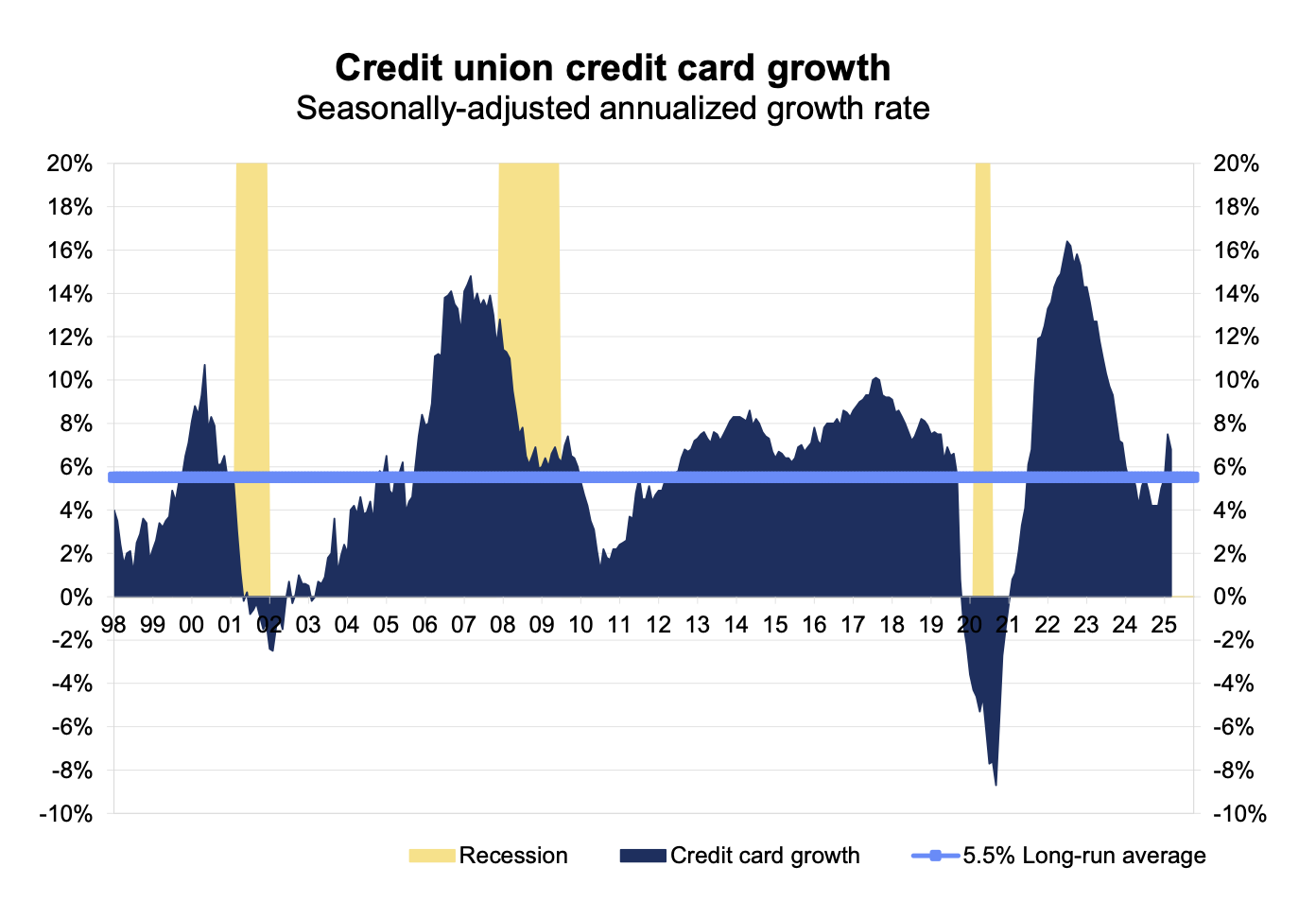

Consumer Installment Credit

The new Trends Report data show credit union credit card loan balances rose at a 6.8% seasonally-adjusted annual rate in March, better than the 5.7% reported in March 2024 and above the long-run average of 5.5%.

“The increase in credit union credit card loan balances could be partly explained by the fact that commercial bank credit card interest rates reached a record high in the last few quarters,” the report states.

According to the report:

- Total consumer credit rose 0.4% ($17.6 billion) in April by all lenders in the U.S., and 4.8% at an annualized rate.

- Revolving credit rose 0.8% in April ($9.5 billion) and increased at a 7.2% annualized rate.

- Nonrevolving credit (auto and student debt) rose 0.2% ($8.1 billion) and 3.4% at an annualized rate.

New Auto Loans Hit Accelerator

“New-auto loan balances grew quickly in March and April, reflecting a surge in new-car purchases by consumers trying to front-run the new tariffs on autos and parts,” the Trends Report notes. “Total consumer loan balances fell 0.8% over the last 12 months for all U.S. lenders, below the 6% annual average reported over the last decade. The year-over-year growth rate in the stock of consumer credit has been negative since December 2024, due to high interest rates, tighter lending standards, tight liquidity at banks and credit unions, and uncertainty over tariff policy.”

On the credit demand side, the Trends Report notes that lower interest rates in the second half of 2025 will make it less expensive to finance purchases, resulting in strengthening demand for loans.

“With inflation in retreat, the Federal Reserve is expected to start lowering interest rates in the third quarter of 2025, providing some relief for borrowers,” the Trends Report added.

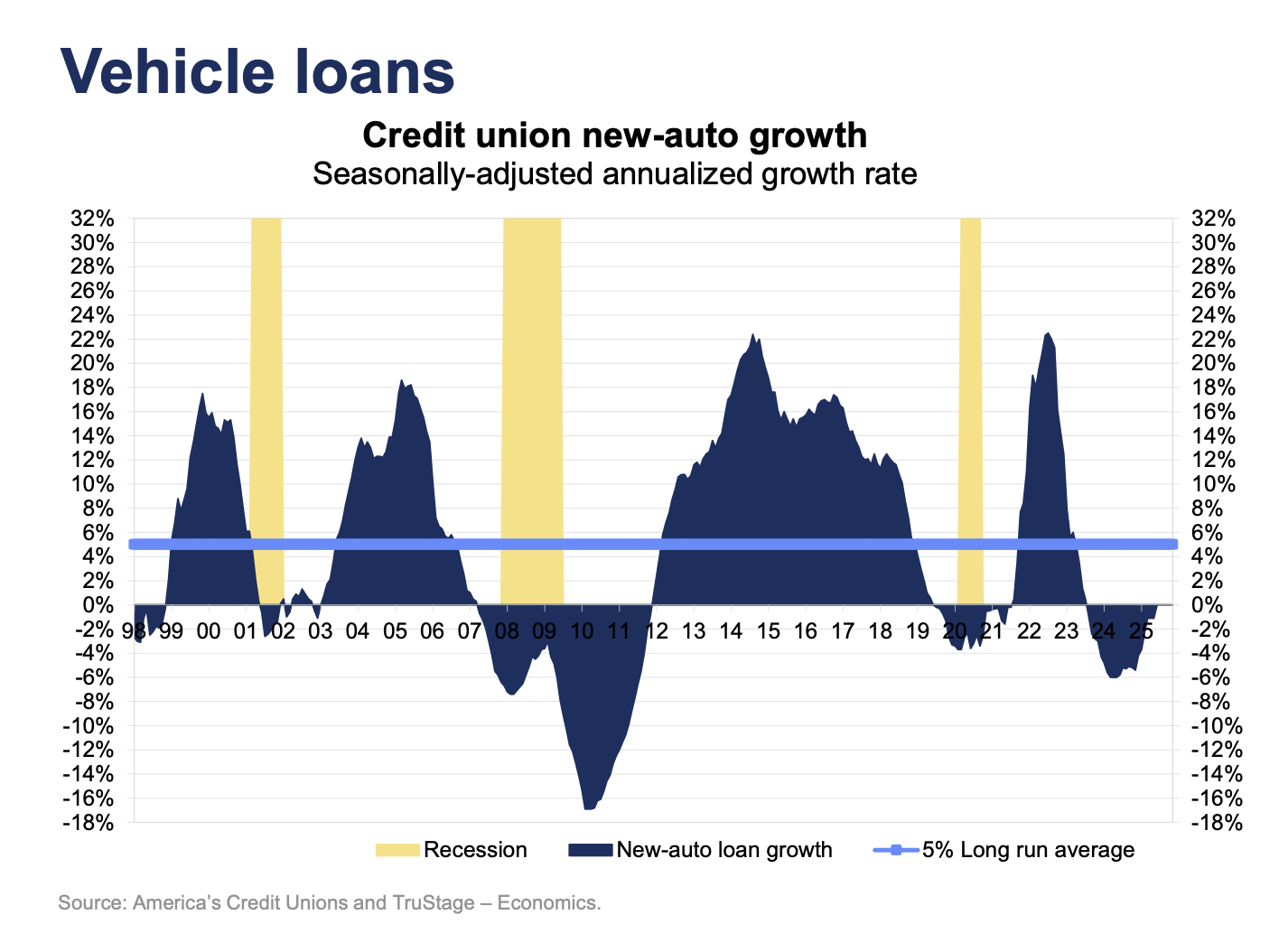

Vehicle Loans

Credit union new-auto loan balances fell 1.1% in March on a seasonally-adjusted annual rate, better than the -6% figure reported in March 2024, but still significantly below the normal 5% pace, according to the Trends Report.

New-auto loan balances fell 1.9% year to date, better than the -2.7% figure reported during the first three months of 2024.

“Looking forward, the month of May is historically the beginning of the new-auto lending season, so we expect credit union new-auto lending to accelerate through October,” the report states.

New vehicle sales fell in June to a 15.3 million seasonally-adjusted annualized sales rate — down 1.7%nfrom May–but rose 2.3% above the pace set in June 2024. This was the first instance of back-to-back monthly declines since mid-2023, the report states.

The Effect of Tariffs

“New vehicle sales numbers were 17.8 million and 17.3 million for March and April, respectively, the highest level in four years as consumers accelerated their purchases to front-run prospective U.S. tariffs on imported vehicles,” the Trends Report said. “The 25% tariff on foreign vehicles and components has resulted in a pullback in foreign vehicle sales relative to domestic brands over the past two months.

“We expect new vehicle sales for all of 2025 to be 15.9 million, only slightly better than the 15.8 million recorded in 2024 and below the 17 million considered to be a healthy new-auto market,” the report continues. “Consumer demand for new vehicles is facing numerous headwinds: trade policy uncertainty, job insecurity, lower consumer confidence, elevated auto loan rates and high new vehicle prices. On the supply side, expect new car prices to rise during the second half of the year as tariffs are passed through to consumers. This will also put price pressure on the used car market as consumers substitute used cars for new.”

Real Estate Information

The new quarterly Trends Report reveals credit union first mortgage loan balances rose 4.5% at a seasonally-adjusted annual rate in March, above the 2.1% pace set in March of 2024.

“Fixed-rate first mortgages now make up 81% of all credit union first mortgage loan balances, down from 82% last March which was the highest in credit union history,” the report states. “This high proportion of fixed rate debt raises concerns for interest rate risk if market interest rates rise.”

The report further notes the contract interest rates on a 30-year fixed-rate conventional home mortgage fell to 6.67% in July, down from 6.85% in June and lower than the 6.92% reported in July 2024. Mortgage interest rates fell over the last year due to a smaller credit spread, the Federal Reserve dropping short-term, the report adds.

“During the last 12 months, home prices rose only 2.7%, below the 4.1% long-run annual average, due to a persistent lack of supply of homes for sale,” according to the Trends Report. “Restricting housing supply is the current spread between the average rate on all outstanding mortgages (the effective mortgage rate) and the current mortgage rate. This spread is now 250 basis-points, which represents the amount an average household would pay in additional interest to trade an existing mortgage for a new one.”

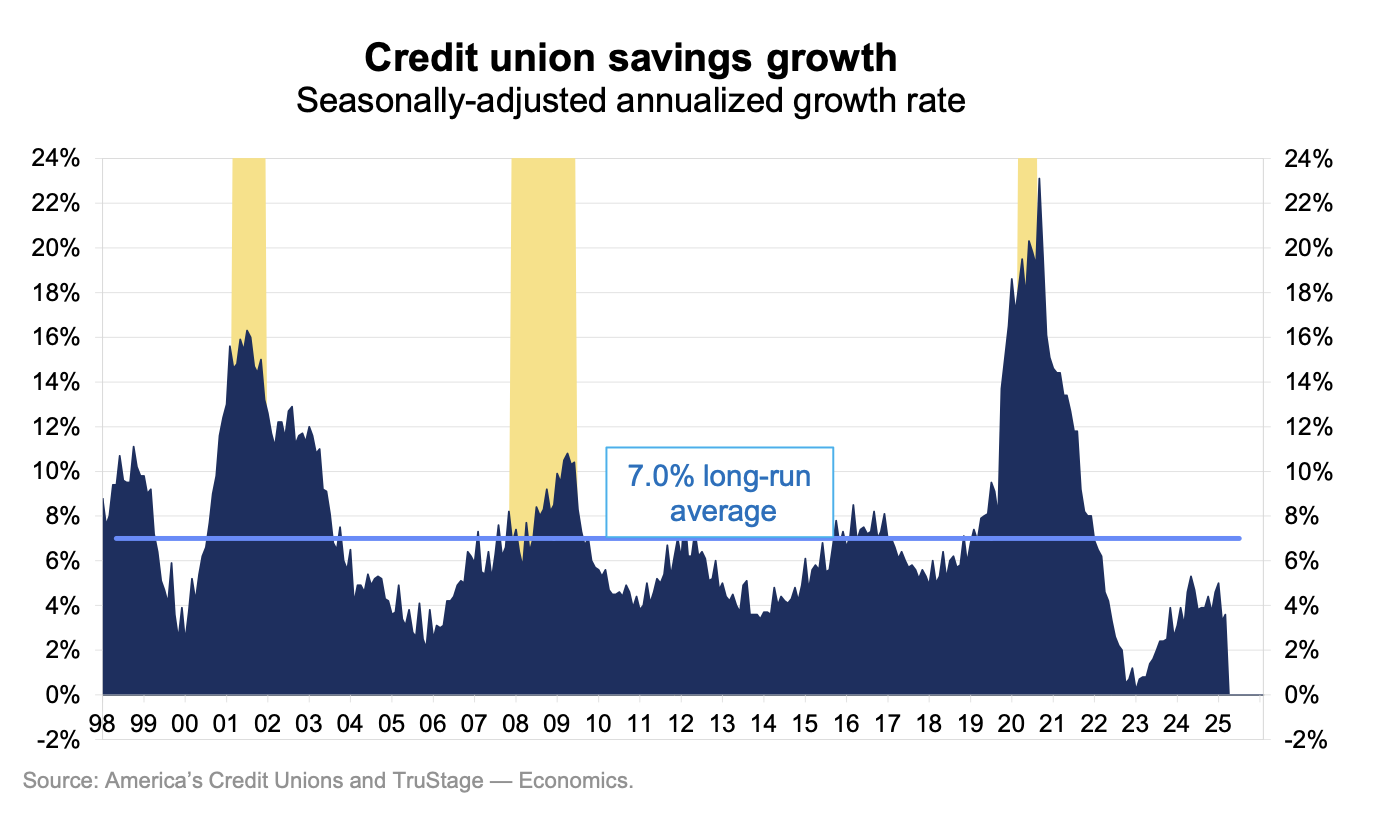

Savings Balances

Meanwhile, savings balances rose at a 3.6% seasonally-adjusted annual rate in March, significantly below the 7% long-run average (but above the 3.1% pace set in March 2024, according to the report.

“Credit union savings balances rose 2% in the first quarter, less than the 2.8% set in 2024 and below the 4% long-run average,” the report states. “Up to 59% of full-year deposit growth takes place in the first three months of the year due to tax refunds and bonus checks being deposited in checking and savings accounts. April is typically one of the weakest months for savings growth as members use deposits to pay tax liabilities.”

Better Liquidity Environment

The report notes that credit unions are now facing a better liquidity environment when it comes to savings deposits compared to last year. Moreover, as the report explained, the U.S. money supply as measured by M2 grew 4% over the last year to reach $21.8 trillion, still below the 5.5% average annual growth rate but better than the -0.1% year-over-year growth rate reported in March of 2024.

M2 is defined as the sum of currency in circulation, checkable deposits, savings accounts, money market deposit accounts, time deposits and money market mutual funds, Rick explained in the report.

“Expect savings balances growth to slowly rise this year to 6.5% full-year growth as consumers return to a more normal pace of spending and saving following the atypical spending/savings patterns experienced during the COVID-19 pandemic and its aftermath,” the Trends Report forecasts.

Equity and Other Key Measures

The new data show credit union return-on-asset ratios averaged 0.65% in the first quarter of 2025, two basis-points higher than the 63 basis-points reported in the first quarter of 2024, due to a rising interest margin 23-basis-points offsetting rising operating expense ratios, falling fee and other income ratios, and a rising provision for loan loss ratio.

“Credit union operating expenses rose 6.1% during the last year, faster than asset growth of only 2.7%,” the report states. “This pushed the operating expense ratio to 3.06% in the first quarter of 2025, up from 2.96% in the first quarter of 2024. During the last five years, the price level rose 24%. As credit union vendor contracts renew, much of this cost increase is showing up in new vendor pricing.”

Net Interest Margins Rise

Meanwhile, the data show net interest margins rose 23 basis-points as asset costs fell from 1.84% in the first quarter of 2024, to 1.83% this year. At the same time, asset yields rose from 4.84% to 5.06%. The net interest margin ratio measures the profitability of financial intermediation, i.e., taking in deposits and originating loans.

“For the full-year, we now expect credit union net income as a percent of average assets to rise to 0.70% in 2025 from 0.61% in 2024, as existing loans are repaid and reloaned out at today’s higher rates and then rise to 0.75% in 2026,” the report predicts. “Earnings will remain below their 78-basis-point 25-year average due to credit unions experiencing higher operating expense ratios from rising wages and high provision for loan losses.”

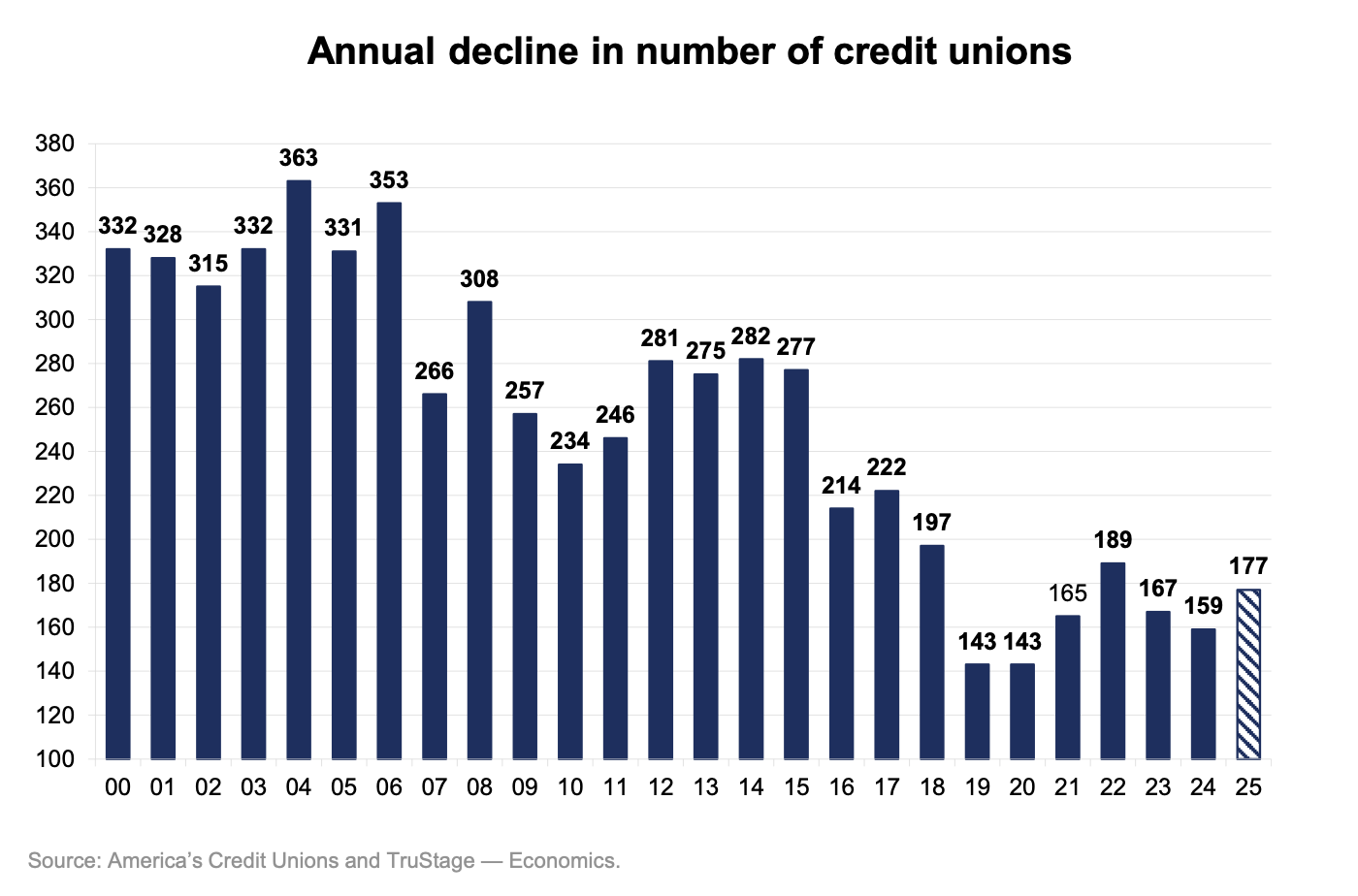

Credit Unions & Members

As of March 2025, America’s Credit Unions estimates 4,504 credit unions were in operation, 177 fewer than in March 2024.

“During the first three months of 2025, approximately 40 credit unions ceased to exist because of mergers, purchase and assumptions, or liquidation,” according to the report. “This rate is above the 29-credit union decline reported during a similar period in 2024. In 2024, the number of credit unions declined by 159, with 71 occurring during the first half of the year and 88 taking place in the second half. The second half of a year will typically experience 53% of all credit union mergers.”

The report is predicting the pace of credit union consolidation will accelerate in 2025 and 2026, due to some credit union managers focusing on possible merger opportunities due to rising competitive pressures.

“Moreover, continued high short-term interest rates produce a flat Treasury yield curve, which historically puts downward pressure on credit union net interest margins, earnings and equity,” the Trends Report states. “So, we expect the number of credit unions to decline by 180 in 2025, the fastest pace since 2022. This acceleration in the pace of consolidation is what happened in the wake of the global financial crisis in 2009 –2011, when the number of mergers dipped in 2010 and 2011, but surged in the four years following the crisis.

‘Surge in Mergers’

“With high short-term interest rates stressing some credit unions to the point of considering a merger, expect a surge in mergers during 2025 – 2028, as smaller credit unions with limited earnings, asset growth, capital growth and digital capabilities look for merger partners to increase the products and services offered to their members,” the Trends Report added.