DUBLIN, Ohio– A new report released by American Share Insurance (ASI) demonstrates the “strength, stability, and strategic value of private share insurance for credit unions,” according to the company.

The 2025 Economic Report, authored by Dr. Bill Hampel, the former chief economist with CUNA/America’s Credit Unions, examines the financial health and performance of credit unions with private deposit insurance and compares them to national averages.

“The findings reveal that privately insured institutions demonstrate stronger capitalization, comparable asset growth, and increased member engagement,” ASI said in releasing the findings.

According to the report, ASI-insured credit unions have demonstrated “resilient growth over the past three decades,” which the company noted included stressful economic and financial environments.

“Assets at ASI-insured institutions expanded at an average annual rate of 5.6%, closely tracking the 6.3% rate of federally insured credit unions,” ASI said.

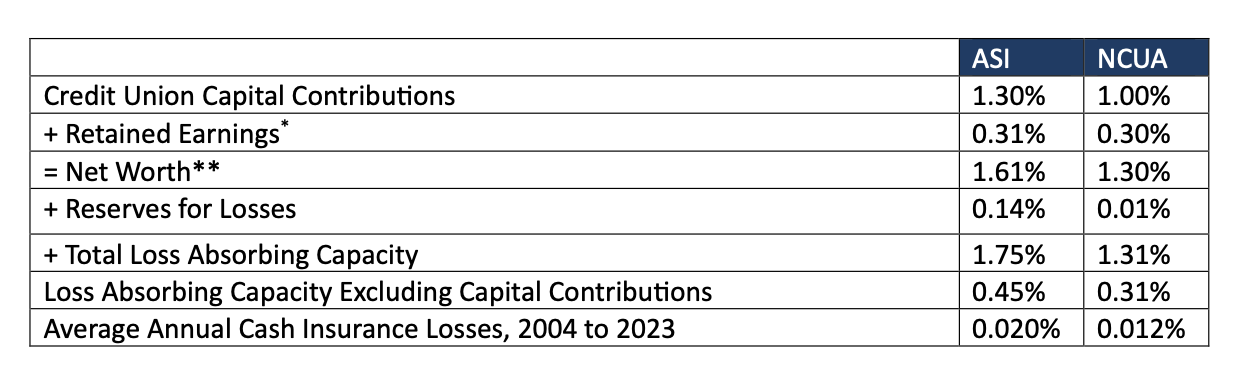

The company said the report further shows ASI’s track record of financial stability, noting that in “nearly five decades of operation, no credit union member has ever suffered a loss of insured shares. This strong performance was particularly evident during the Great Financial Crisis of 2007-2009, when ASI successfully managed heightened challenges despite significant exposure in states hardest hit by the economic downturn.”

Proven Model

“Private share insurance is not the right fit for every credit union, and we recognize that. For state-chartered credit unions that choose it, ASI delivers a proven model built on strong capital, trusted state oversight, and the flexibility to serve members in ways that reflect local priorities and values,” Hampel said in a statement. “These findings should encourage policymakers and credit union leaders to explore viable alternatives that preserve the unique strengths of the credit union model.”

Additional Findings

In addition, ASI said the report reveals the availability of ASI insurance “enhances the attractiveness” of a state credit union charter.

“From 2000 to 2023, the proportion of credit unions with a state charter rose in states that allow private insurance, while the share fell in states that prohibited it,” ASI stated. “The difference in these trends is dramatic. State-chartered credit unions in ASI states increased from 42.9% to 47.4% of total institutions, while falling from 38% to 35.6% in all other states. This substantial divergence in the incidence of state charters reflects not only strong financial performance – including consistently high capital ratios and low delinquencies – but also operational advantages such as streamlined regulatory oversight that eliminates dual federal examinations.”

Stronger Business Lending

ASI said the report further identifies the “strategic positioning” of ASI credit unions in business lending.

“These institutions devoted 12.2% of their assets to business lending in 2023 — more than double the 5.8% rate at federal credit unions and significantly higher than the 8.3% at state credit unions overall,” ASI said. “This focus enables them to serve diverse member needs and demonstrates strong support for local business communities.”

‘Greater Independence’

“Our model provides a sound, state-regulated alternative to federal insurance that gives credit unions more flexibility, greater independence, and the ability to serve their members better,” ASI CEO Theresa Mason said in a statement. “This report confirms what we’ve long believed: when credit unions are empowered to choose the insurance solution that aligns best with their mission and members, everyone benefits.”

The report can be found here.