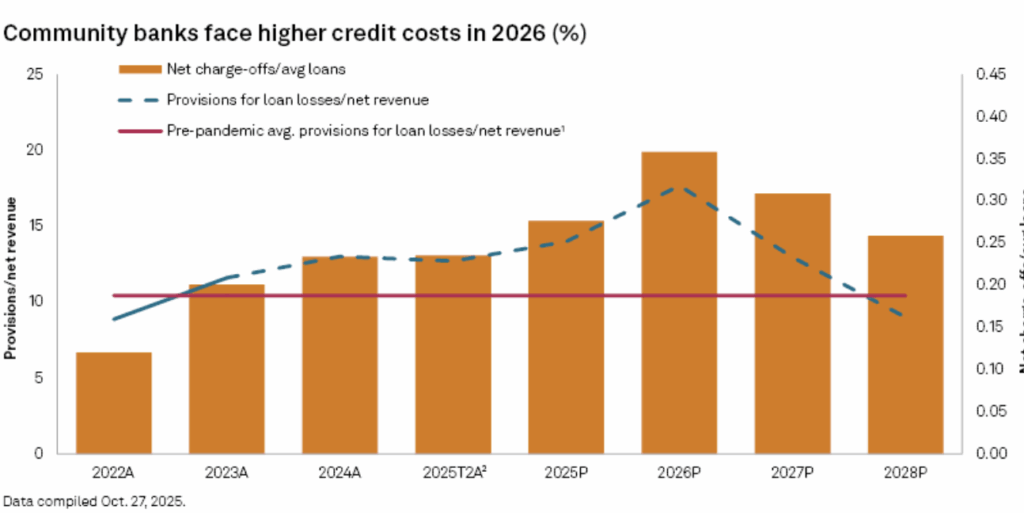

NEW YORK–Strong net interest margins have supported earnings at U.S. community banks’ in 2025 and earnings growth should continue in the coming quarters, even as credit costs continue to migrate higher, according to a new forecast from SPG Global.

“Community bank margins have expanded as the benefit from fixed-rate assets repricing has overshadowed modest increases in funding costs,” SPG Global said. “Community banks in aggregate reported strong earnings growth in 2025, but the pace of earnings growth is anticipated to moderate in 2026 due to the higher credit costs. Credit quality is expected to slip as the lagging impact of tariffs could slow economic growth, impact consumer spending and increase delinquencies, necessitating higher reserve builds.”

Shoe Has Yet to Drop

SPG Global added in its analysis that many investors have been waiting for the credit shoe to drop but asset quality remains benign.

“While a handful of regional banks reported issues related to loans to nondepository financial institutions, most community banks have little to no exposure to that asset class,” SPG Global said. “Most regional and community banks, in a variety of geographies, reported little to no deterioration in their credit quality in the quarter.”

As an example, SPG Global said banks such as Grand Rapids, Mich.-based Mercantile Bank Corp., Kalispell, Montana-based Glacier Bancorp Inc., Cincinnati-based First Financial Bancorp., Olympia, Wash.-based Heritage Financial Corp., Novato, Calif.-based Bank of Marin Bancorp., Chicago-based Byline Bancorp Inc. and Houston-based Stellar Bancorp Inc. noted on their respective third-quarter earnings calls that asset quality generally was “excellent” or “stable to improving,” though a few institutions reported challenges with a single relationship.

Credit Quality to Normalize

“We expect credit quality to normalize from current levels due to weakness in the US consumer and some stress in commercial real estate portfolios, leading to a higher level of losses,” SPG Global said. “Consumer delinquencies have risen from historical lows and student loan delinquencies have jumped back near pre-pandemic levels now that the moratorium on payments is several quarters in the rear-view mirror. Community banks generally do not have direct exposure to those credits, but the deterioration offers another indicator that the US consumer is stretched, marked by slower savings rates and recent weakness in the labor market.”