MADISON, Wis.—During the second quarter a reduction in auto loan originations contributed to slower membership growth at credit unions—with CUs below $1 billion in assets seeing no to negative increase in memberships—while loan balances remained well below the average and provisions for loan losses were up, according to the newest Trends Report from TruStage, which is also forecasting home price appreciation to be zero to negative over the next year.

Here is a look at what the Trends Report—authored by TruStage’s chief economist, Steve Rick, has found regarding credit union performance by category:

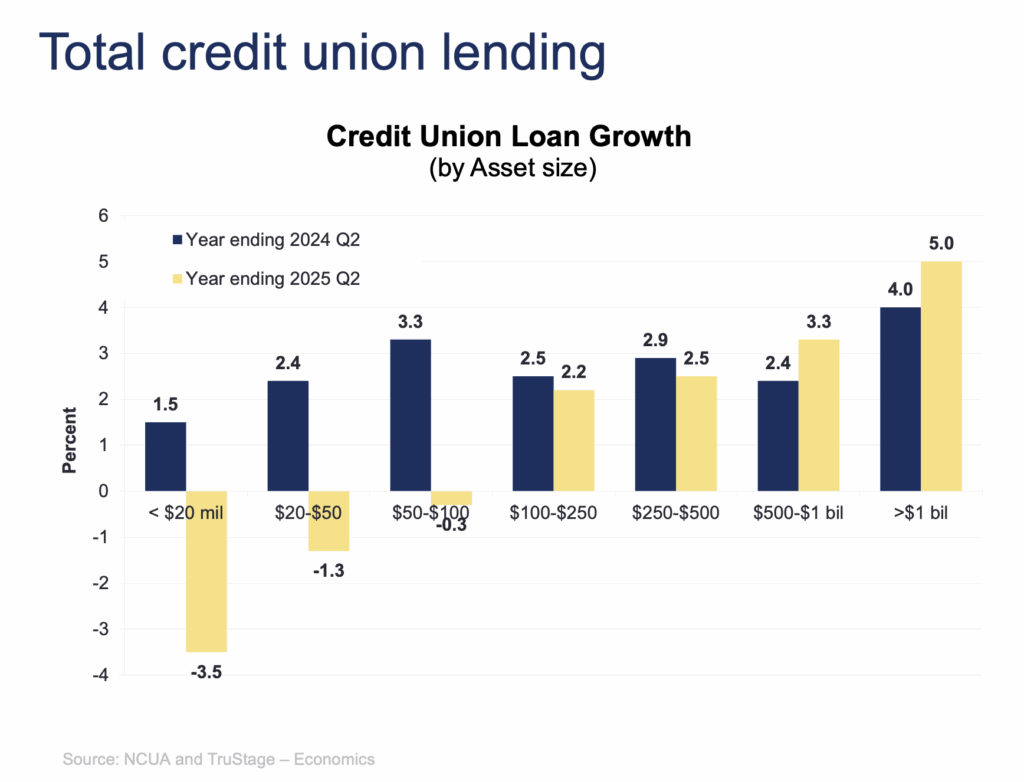

Total Credit Union Lending

Credit union loan balances rose 1.8% in the second quarter, above the 1.1% pace reported in the second quarter of 2024, due to lower interest rates increasing the demand for loans and rising credit union liquidity increasing the supply of loans, the report states.

Credit union loan balances rose 3.9% in the year ending in June 2025, up slightly from the 3.4% reported for the year ending June 2024.

As has been the trendline, the report adds, “Credit unions with asset size greater than $500 million reported faster loan growth this year than last year, while smaller credit unions reporting slower loan growth.”

The report further notes that bank lending also rose 3.9% during the 12 months ending in June 2025, faster than the 2.6% reported in the year ending in June 2024, but below their long run average of 6%. Slower than normal lending growth rates are one of the “long and variable lags of monetary policy” that Federal Reserve Chairman Jerome Powell likes to discuss at his press conferences, the report explains.

Credit union loan balances are forecasted to rise only 4.5% in 2025, below the long run average of 7% per annum. We are forecasting slightly better credit union loan growth for 2026 (around 5%) as lower interest rates encourages members to borrow and spend and credit unions experiencing slower amortization of past debt.

Consumer Installment Credit

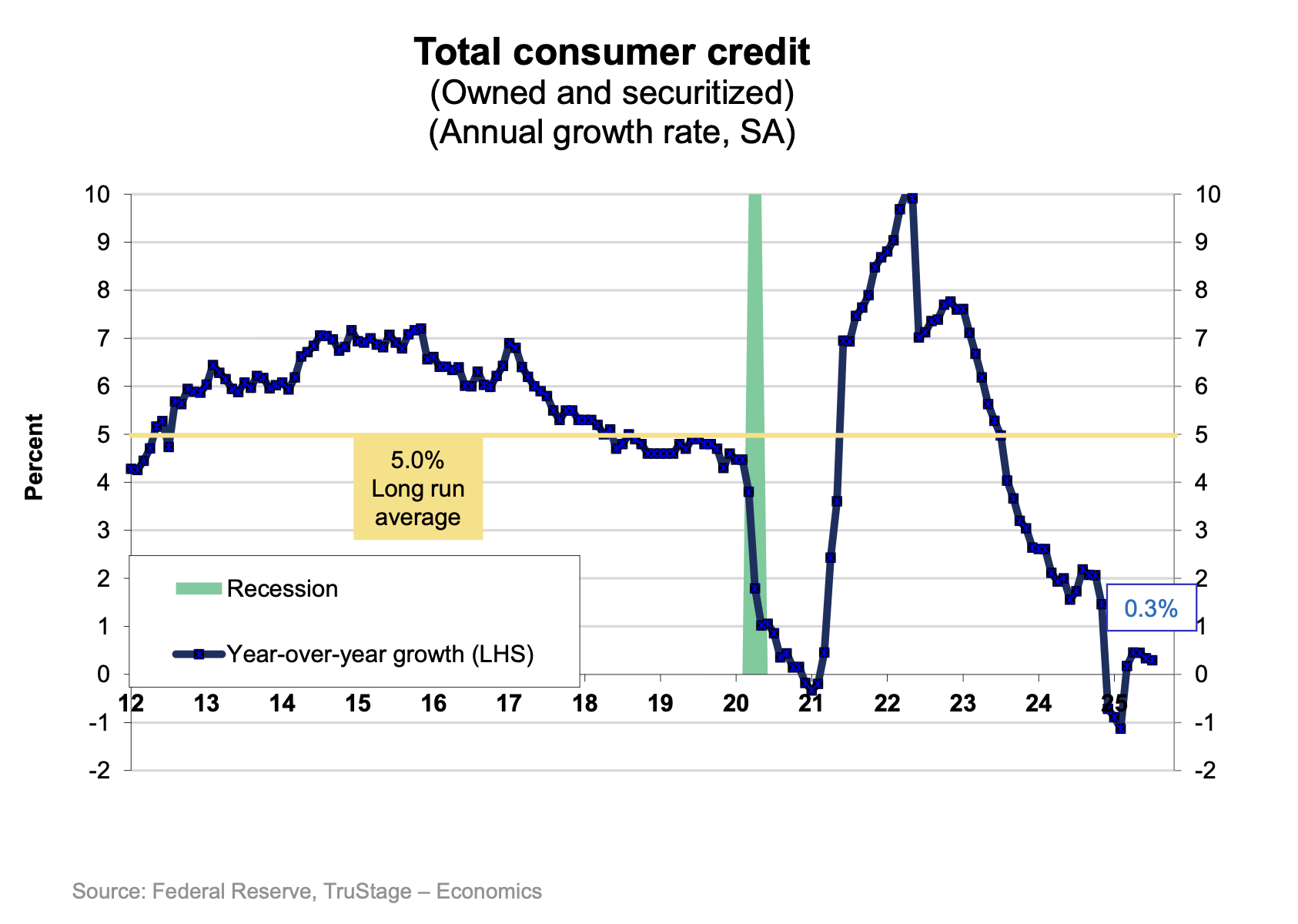

Credit union consumer credit loan balances (auto, credit card and other unsecured loans) fell 1.0% in the year ending June 2025, a deceleration from the 0.1% increase set during the 12 months ending in June 2024. A 1.9% drop in credit union auto loan balances account for the decline as the massive auto loan originates of 2022 get paid off today.

According to the Federal Reserve, consumer credit outstanding for all lenders rose only $0.4 billion in August, below the $15 billion long run monthly average growth; non-revolving credit (large loans such as automobile and student loans) rose $6.4 billion while revolving credit (credit cards and home equity lines of credit) fell $6 billion.

The decline in revolving credit was due to lower gas prices, borrowers trying to pay down high-interest rate debt and lenders tightening lending standards. Consumer credit outstanding is rising only 0.3% year-over-year, below the 5% long run average. This slowdown in credit creation is one of the “long and variable lags of monetary policy” the Federal Reserve Chairman Jerome Powell likes to mention at his press conferences. Less loan creation leads to less spending and therefore less price pressure. This will create disinflation as the inflation rate falls from around 3% today to the Fed’s target of 2% over the next two years.

Going forward, expect consumer credit growth to accelerate into 2026 as consumer demand picks up, lower interest rates make debt more attractive and credit union liquidity pressures subside, the report adds.

Vehicle Loans

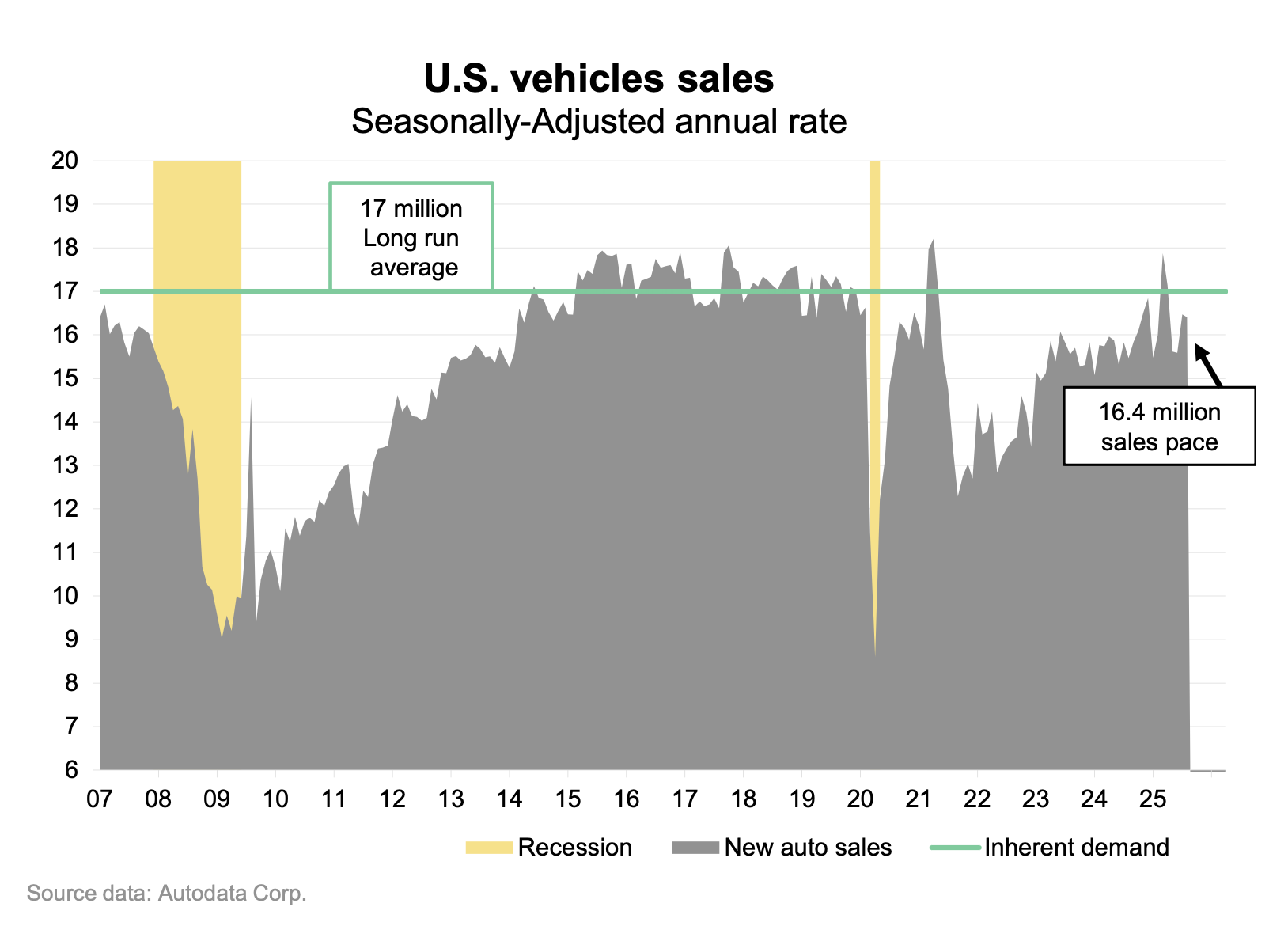

The Trends Report notes that vehicle sales fell in August to a 16.4 million unit seasonally-adjusted, annualized sales pace, which is down -0.4% from July, but up 6% from August 2024, when 15.5 million units were sold. New vehicle sales are still below the 17 million pre-pandemic pace considered to be the market equilibrium.

“Consumers seem to be holding out for better deals despite higher auto inventories and improving incentives,” the report observes. “Higher than normal auto loan rates will ensure that new-vehicle sales remain below the 17 million pace through 2026. New vehicle sales are then expected to surpass 17 million in the first quarter of 2017, when the Federal Funds interest rate is expected to fall back to its 3.0% neutral rate.”

The report found an increase in auto tariffs and therefore auto prices has reduced affordability for auto buyers. The Cox Automotive/Moody’s Analytic Vehicle Affordability Index, which measures affordability in the number of weeks it takes a median family income to purchase and finance a new vehicle, indicates autos are 14% less affordable today as compared to prior to the 2020 pandemic.

“Affordability will improve as auto interest rates decline as the Federal Reserve’s lowers its target rate, albeit with a lag,” the Trends Report forecasts.

A Look at Loan Balances

It further notes that credit union new-auto loan balances fell 2.3% in the first half of 2025, less than the 4% decline reported in the first of 2024. Used auto loan balances rose 0.1% in the first 6 months of 2025 above the 0.8% decline reported in the first half of 2024.

“With auto loan interest rates falling to the 5.0-7% range, auto demand is expected to improve. Auto loan supply, however, is being constrained as credit unions’ auto loan delinquency and charge-offs rates are up during the last year,” the report states. “This has led some credit unions to tighten credit standards and increase the percentage of loan applicants denied.”

Real Estate Information

Credit union fixed-rate first mortgage loan balances rose 1.3% during the year ending in June 2025, above the 0.5% decrease reported in the year to June 2024, according to the Trends Report. Credit union fixed-rate first mortgage loan balances fell 4.7% at a seasonally-adjusted annual rate in June, the third consecutive month of decline. Adjustable-rate first mortgage balances rose 13.3% during the last year, below the 19.3% gain reported in the year ending in June 2024.

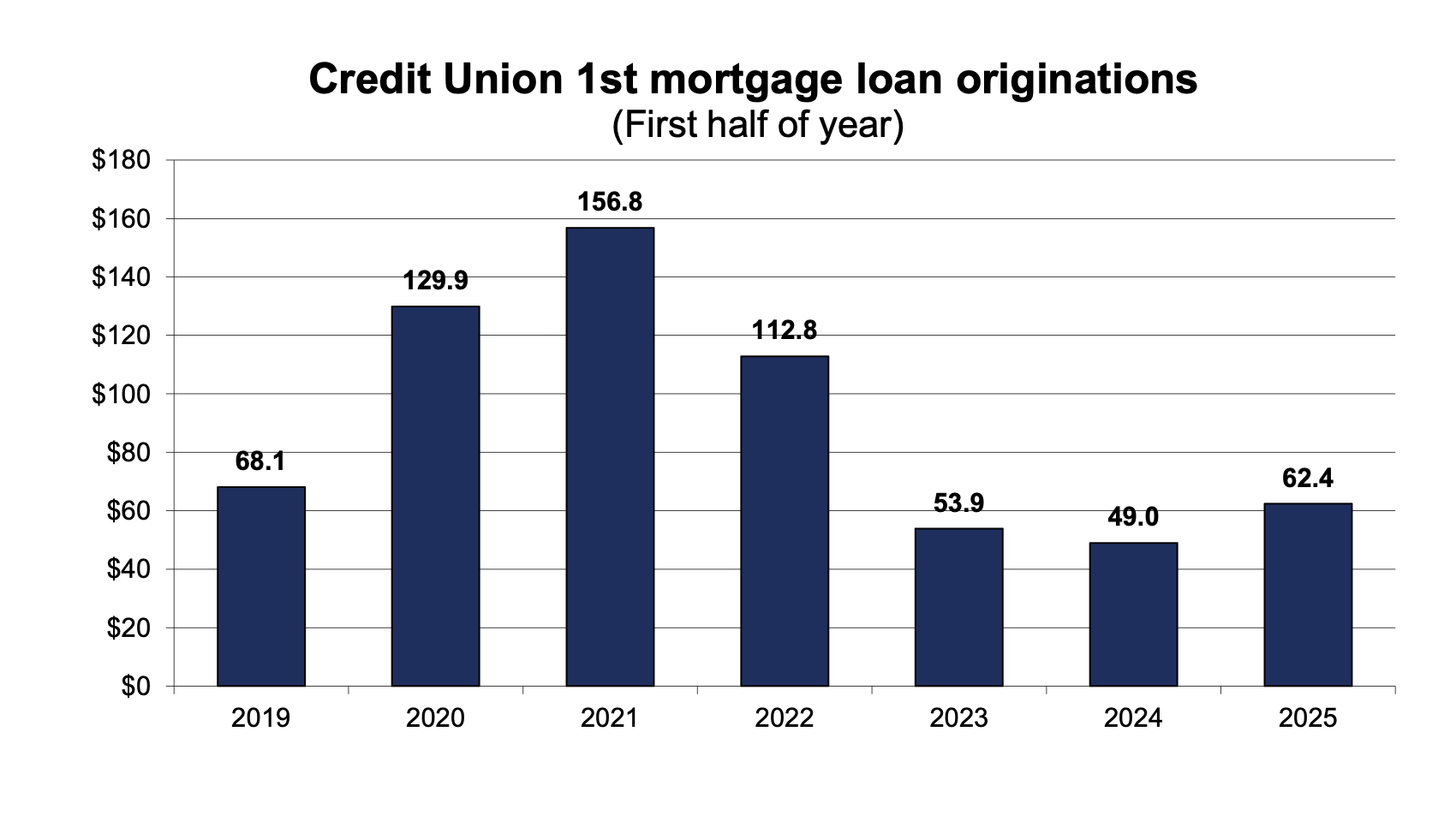

The report notes credit unions originated $62.4 billion first mortgage loans in the first half of 2025, a 27% increase above the $49 billion in originations in the first half of 2024, “but a remarkable 60% decrease below the record $156.8 billion in originations in the first half of 2021. Credit unions then proceeded to sell off only 24.9% of those originations into the secondary market in 2025, below the 33.7% sold off in the first half of 2024.

‘The Stage is Set’

“The stage is set for a better second half of 2025, due to the recent fall in mortgage interest rates to around 6.3% and a rising supply of home for sale,” the report continues. “We expect both purchase and refinance mortgage activity to accelerate during the next six months.”

Looking forward, the report forecasts, “Expect the pace of home price appreciation to slow as inventory grows and heightened economic labor market uncertainty reducing demand. Lower interest rates could increase housing demand, but housing supply may increase more. So, expect home price appreciation to be zero to negative over the next year.”

Savings & Assets

Credit union savings balances rose 3.3% in the first six months of 2025, above the 2.7% increase in balances reported in the first half of 2024, as lower money market interest rates reduce the competitiveness of money market mutual funds, according to the Trends Report, which notes that during the last 12 months, credit union savings balances rose 4.9%, above the 2.6% set in the year ending June 2024 but below the pre-COVID 19 pandemic average of 6.7%.

“During the first half of 2025 credit unions were paying an average 1.92% interest on their savings deposits, up slightly from the 1.89% in the first haff 2024. The interest paid by credit unions on deposit balances should have then raised deposit balances by around 1.9%,” the report states. “Moreover, with credit union memberships growing 1.9% during the last 12 months, deposit balances should have increased as new members opened checking and savings accounts and deposited new money into the credit union. Therefore, savings per member is currently rising at a slow 3.0% pace (4.9% – 1.9%). which is below the 4.2% long run average. The weak credit union savings growth rates are partly explained by the low national Personal Savings Rate (savings as a percent of disposable income) which averaged 5.1% over the last year, according the Bureau of Economic Analysis, below the long run average of 6%.”

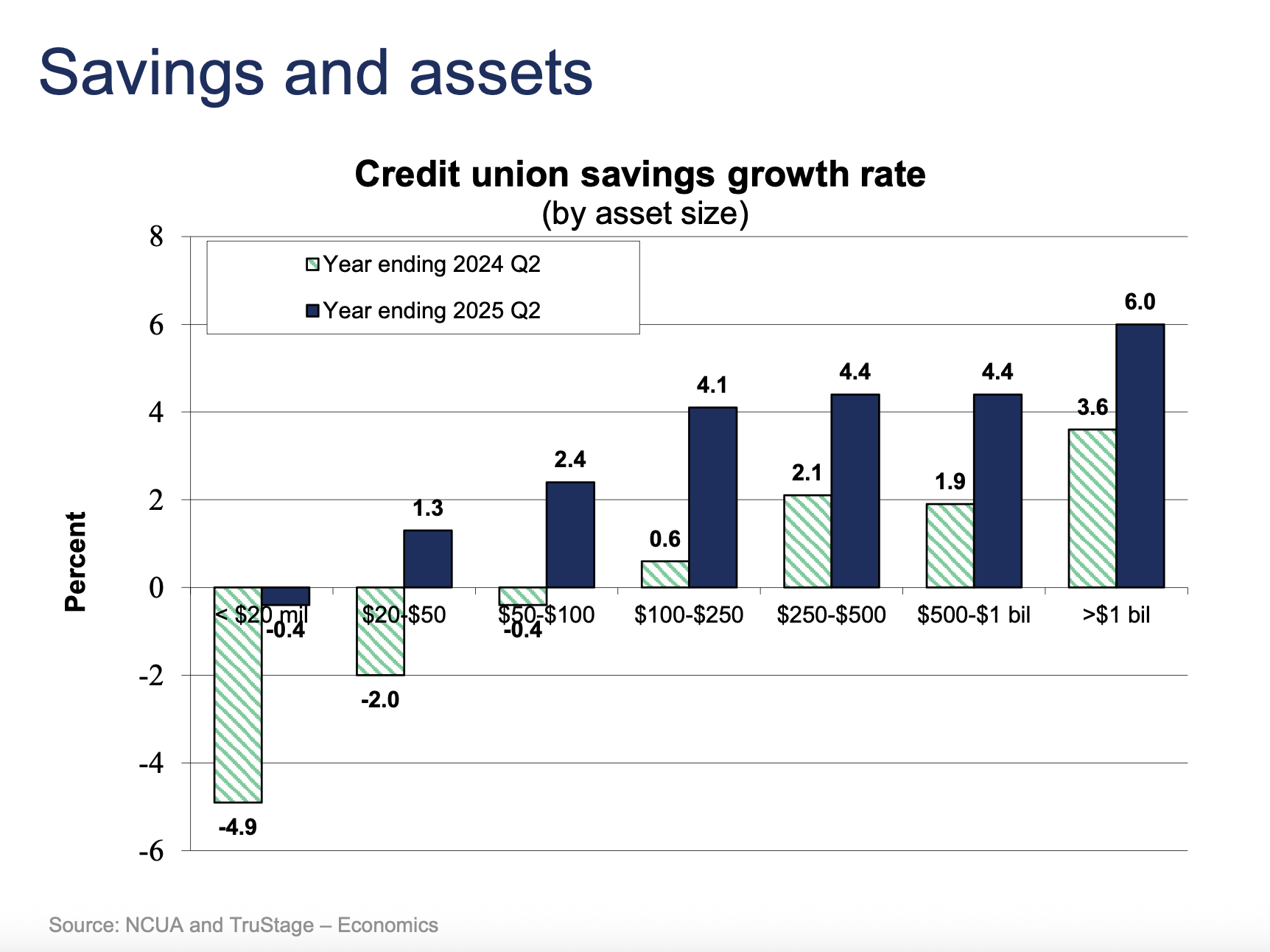

The report notes that according to NCUA call report data, credit unions of all sizes reported better savings growth rates during the last year as compared to the similar period in 2024. We expect credit union savings balances to rise 5% in 2025 and then accelerate to 6% in 2026 as the Federal Reserve continues to lower short term interest rates.

Equity and Other Key Measures

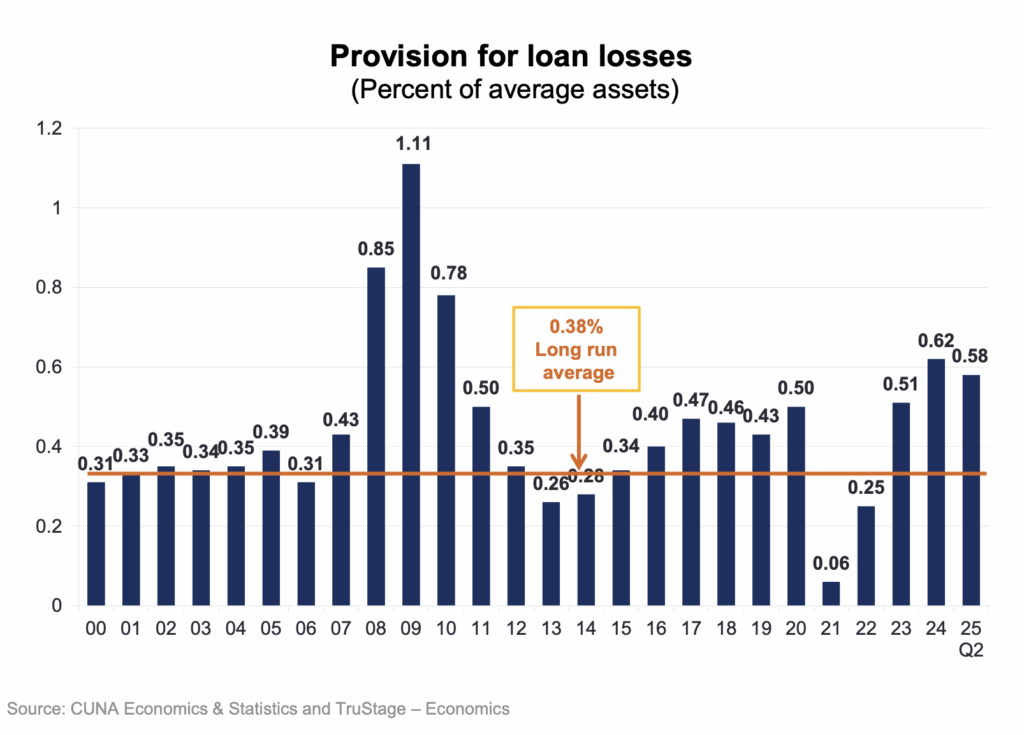

The Trends Report analysis shows credit union provisions for loan losses, as a percent of assets, rose to 0.58% in the first half of 2025, from the 0.57% reported in the first half of 2024, but down from the 0.62% set for all of 2024.

Historically, credit unions set aside 38 cents for every $100 in assets to account for loan losses (see the orange line in the figure). This surge in provisions during the last few years was one factor reducing credit union earnings and return-on-assets ratios in 2023 and 2024.

“Provisions are elevated this year in part due to high net loan charge offs, which are significantly above the 0.50% long run trend rate. Net loan charge offs to average loans came in at 0.75% in the second quarter of 2025, which was like the 0.78% reported in the first quarter of 2024,” the report states.

The Trends Report analysis notes that many credit union members are experiencing financial difficulties due to five factors.

- First, high inflation over the last four years reduced many members real (inflation adjusted) incomes and therefore reduced the purchasing power of their incomes.

- Second, higher interest rates are squeezing consumers who may have variable rate debt by raising their debt service costs.

- Third, high rents, food prices and auto insurance has reduced funds available for debt servicing.

- Fourth, the resumption of student loan payments has squeezed young borrowers’ budgets. And finally, many credit union members have exhausted any “excess savings” they may have accumulated during the COVID-19 pandemic. These factors will continue high loan charge offs rates at credit unions and therefore high provisions for loan losses during the next year.

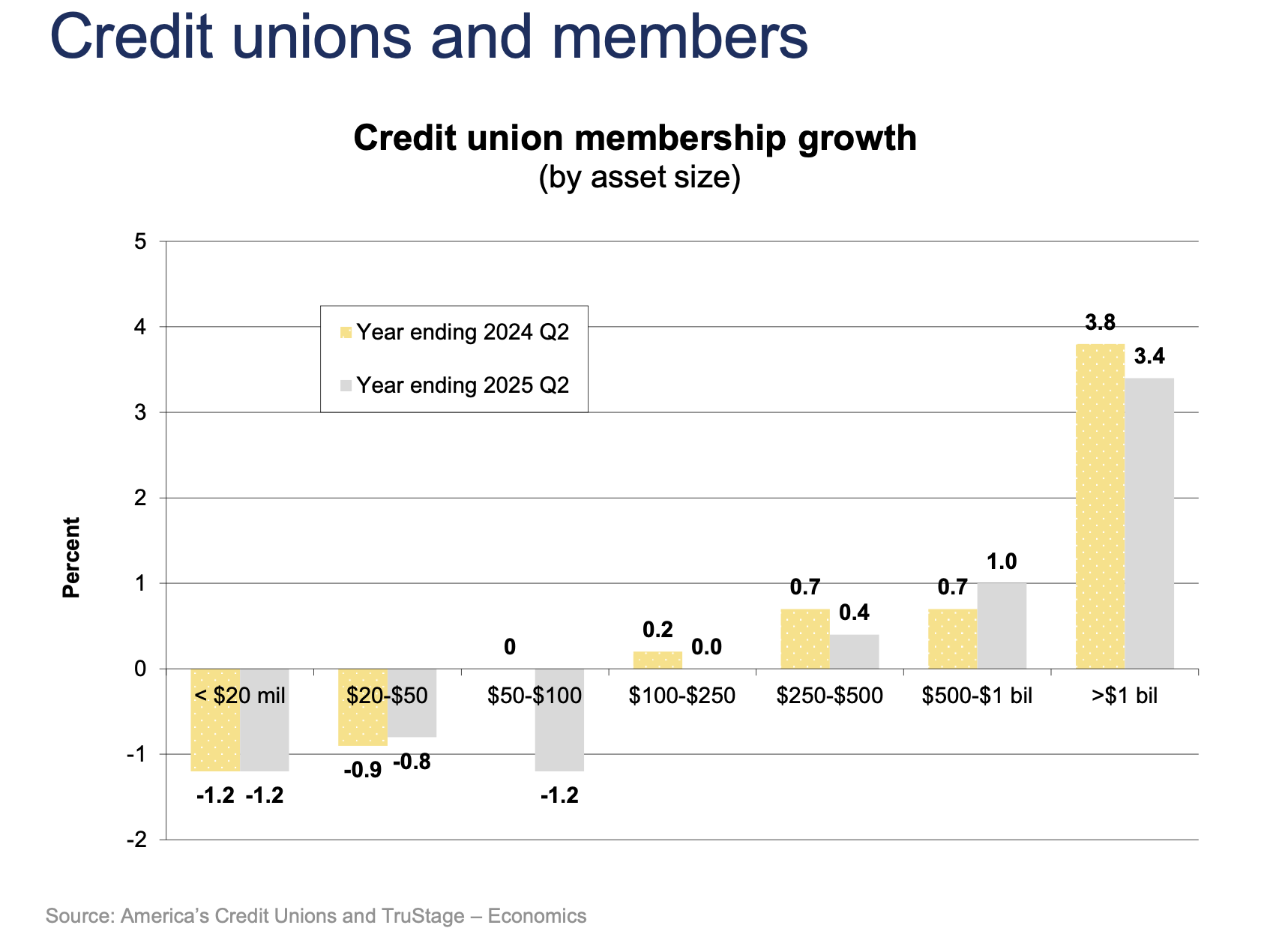

Credit Unions & Members

Credit union memberships grew 0.5% in the second quarter of 2025, below the 0.6% reported in second quarter of 2024, to a significant reduction in auto loan originations and slower job growth. On an annual growth rate basis, memberships are up only 1.9% in the year ending in June 2025, below the 2.4% pace set in the year ending in June 2024, according to the report.

“We expect this slow membership growth pace to continue as many of indirect auto loans made during the boom year of 2022 get paid off and credit unions remove these inactive accounts from their membership rolls,” the report states. “The membership growth slowdown was also partially driven by weak job growth. During the last 12 months the economy created only 1.5 million jobs, down from the 2 million gained during the year ending in June 2024, according to the Bureau of Labor Statistics. Many Americans join credit unions that may be affiliated with their employer when they obtain employment.”

As has also been a trendline, the report found most credit unions with less than $250 million in assets reported no to negative membership growth during the last 12 months.

“Meanwhile, credit unions with assets greater than $1 billion reported relatively strong membership growth of 3.4% due to organic growth and mergers activity,” the Trends Report states. “Credit unions should expect membership growth of around 2.0% in 2025, and a slightly better 2.2% membership growth is forecasted for 2026 as loan growth picks up.”