NEW YORK–During 2024 a record 4.8% of workers in 401(k) plans took a hardship distribution for financial emergencies, up from a prepandemic average of about 2%, according to a new analysis from the Vanguard Group.

In addition, nearly one-third of people who leave jobs annually liquidate their 401(k)s, paying taxes and often penalties rather than keeping the money in a retirement account, Vanguard said.

The withdrawals have come for a number of reasons, including that Congress has repeatedly made it easier to raid these accounts, the Wall Street Journal pointed out..

“This adds up to a sea change in how Americans view their retirement savings: The $12.2 trillion in 401(k) accounts isn’t necessarily locked away, earmarked only for retirement income,” the Journal stated. “As people divert more of their savings to 401(k)s, the accounts are doing double duty as emergency funds.”

Social media has also contributed what is referred to as 401(k) “leakage,” according to the Journal, which cited Tik Tok accounts, for example, where people talk about cashing out their 401(k) savings to pay off debt and say they are happy with their conditions, even if they had to pay penalties.

Critics & Proponents

The report said policymakers argue that without early access, many Americans would be less willing to save for retirement to begin with, while proponents say early withdrawals can prevent problems from becoming crises that inflict greater damage on people’s finances.

The Journal reminded that a big downside is that early withdrawals threaten to reduce the wealth available for retirement by about 30% when the lost annual savings are compounded over 30 years, according to economists at Boston College’s Center for Retirement Research.

Further contributing to leakage is automatic enrollment, which has put more workers into 401(k) accounts who might not have chosen to save. Workers can opt out, but many fail to take that step, the Journal added.

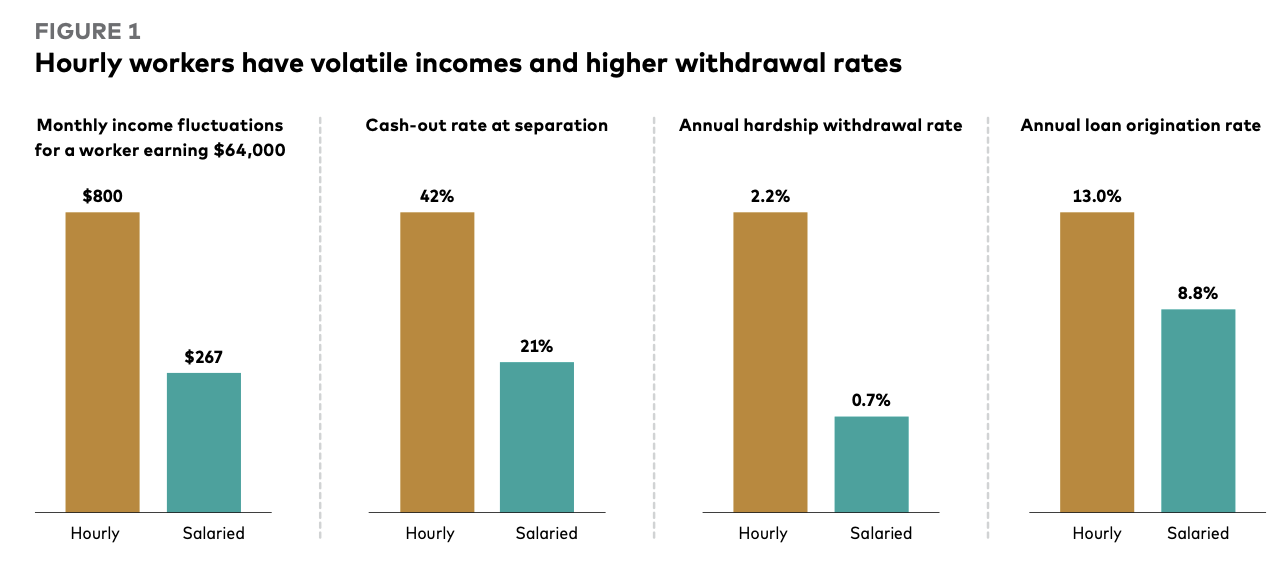

Hourly Workers’ Cash Out

That includes many hourly workers, who cash out and take hardship withdrawals at significantly higher rates than salaried employees, according to new research from Vanguard, which analyzed about three million participants in 401(k) plans it administered from 2008 to 2022.

The Vanguard analysis found that among hourly workers earning $50,000 to $75,000, 42% cashed out their 401(k) savings after leaving an employer, rather than keeping the money inside a tax-advantaged 401(k) or individual retirement account. Of those paid comparable salaries, only 28% cashed out.

A Record

Thanks in part to the spread of automatic enrollment, 82% of eligible workers now save in the 401(k) plans that Vanguard administers, up from 68% in 2007, the company reported.

The average savings rate is a record 12% of income, including employer contributions.