LOST PINES, Texas–Most credit unions are pricing loans and modeling their ALM based on the assumption rates will continue to decline, which brings risks of its own—such as credit risk from longer-term, underpriced loans—but CUs should also be wary if rates increase, which brings risks on the deposit side, one person is cautioning.

In remarks to Catalyst Corporate’s Strategic Summit here, Steven Houle, vice president, Advisory Services at Catalyst Strategic Solutions, covered a wide range of economic and product-related issues during an update on issues credit unions should be giving attention.

Among the areas of the balance sheet Houle touched upon were:

Credit Cards

Houle noted CUs have about 10% of their loan portfolios in credit cards. This category was ever-so-negative for CUs, but overall over the last three years card debt is up 22% among consumers.

“Credit cards represent about 35% of consumers’ transactions,” Houle said. “ So, when you look at your volume how does that compare to the national average for utilization?”

Houle noted consumers are increasingly saying they find value in some very high-cost credit cards due to the rewards programs, such as the American Express Platinum card, which recently raised it’s annual fee to almost $900.

When Houle asked his audience if any credit unions have raised their card fees in the last three years, just one hand was raised.

“People are getting enamored with these reward programs. They see value that lets them justify the cost,” he said, adding that some households are paying thousands of dollars in annual credit card fees.

“What’s also important is who uses credit cards for their spending, and what’s interesting is it’s the greater-than-$150,000-in-annual-income (households) who use it most,” he said. “I think this is one of the evolving dynamics.”

Personal Savings

Roughly speaking, U.S. consumers save around 5% of income.

“So, if you’re planning to bring in 6% or 8% in deposits, how are you going to be above the trend? Maybe with rate? Maybe with a lot of promotion? If you have a lot of liquidity, do you need to bring those deposits in? If not, you may have to overpay for it.”

Federal Open Market Committee

House noted the FOMC is now moving its focus from inflation to employment, with the Fed projecting 1.6% GDP growth moving forward, after earlier predicting negative growth. Any sub-2% growth is not robust, he pointed out.

FOMC members have indicated they see Fed funds moving to 3.4% at year-end 2026, and to 3% in the 2027.

CU Industry Trends

Industry trends cited by Houle included:

- 2025 annualized growth rates are tracking close to the 10-year averages

- The industry net worth ratio continues to increase and was 11.2% at end of Q2

- Risk-based capital was at 15.8% as of the end of Q2.

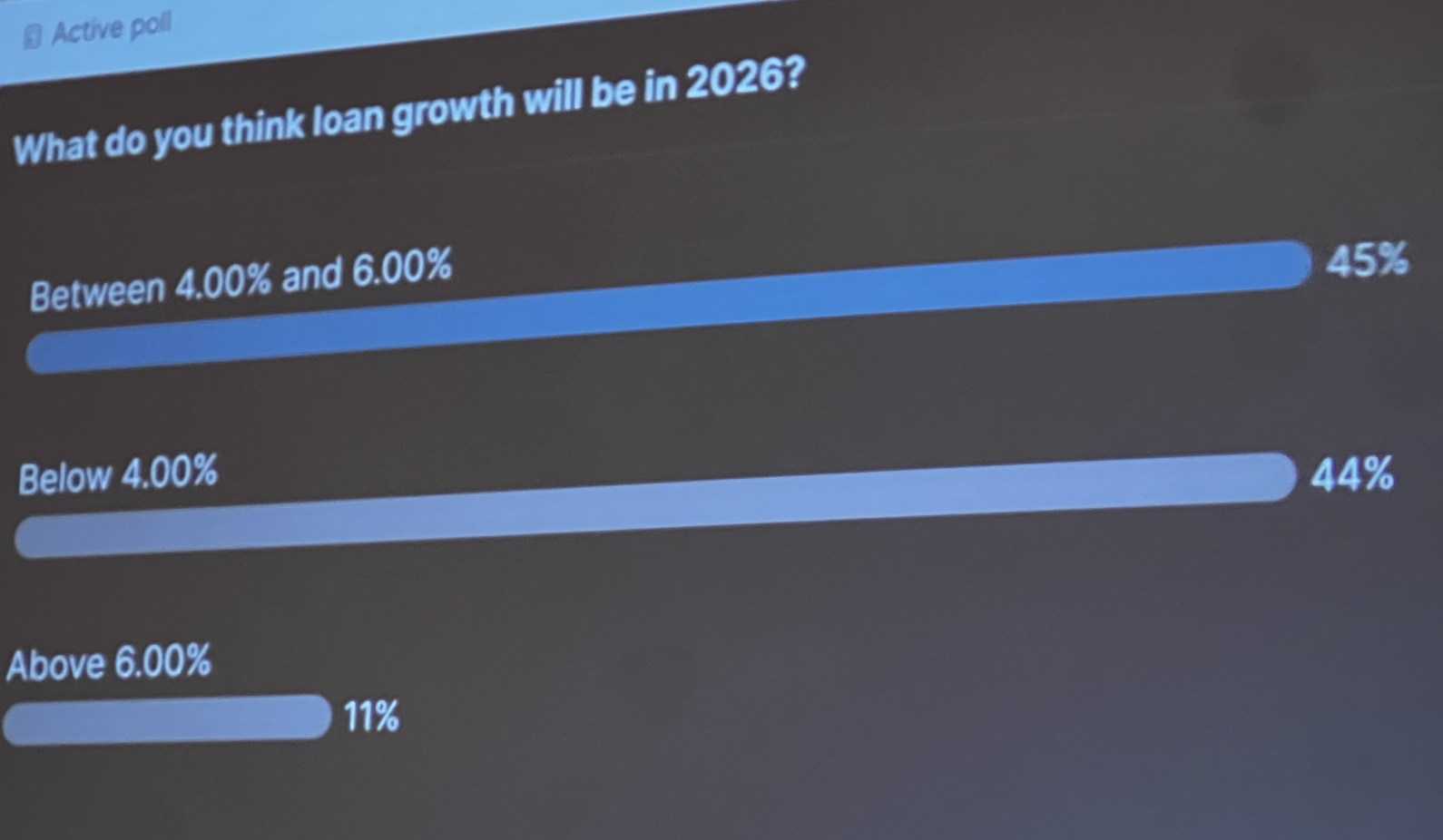

- Loan growth remains anemic. Houle does not see any return to the 10% loan growth days, or even 8%. He predicted a loan volume increase of 4-6% for next year.

Loan Allocations

Loan allocation trends shared by Houle included:

- Unsecured loans decreased 0.3%

- Vehicle loan decreased 0.9%, with new car lending decreasing, but used car lending increasing

- Junior liens have increased, up 14.5%.

- First mortgages increased 6.6%

Real Estate Allocations

- The 30-year loan to the 15-year loan is a 3:1 ratio among credit unions.

“Collectively, credit unions are seeing a slight shift, with first-lien fixed decreasing, with the first lien balloon and junior liens increasing,” said Houle. “The question is what is your limit? I would say we have capacity to increase this. One, collectively, as an industry we have strong net worth. Two, we can use other mechanisms on the balance sheet, and three, the use of derivatives is more available.”

Loan Quality

Houle further noted:

- Delinquencies and net charge-offs have improved in 2025 but remain elevated. Delinquencies are at .91% and net charge-offs at 0.70%.

- “The areas of heartburn have been credit cards and used auto loans, but the good news is they have come off their peak and are being flushed out of the system,” Houle said.

Loan Rates

“Prepare yourself if we do see lower-term yields. We’ve got to be nimble,” House said. “If rates fall and activity picks up, will you have the liquidity and staff resources to manage a fast-moving environment, if we get there?”

The chart above reflects an audience vote taken during the meeting.

Share Growth

The industry LTS has hovered around 80% for some time, noted Houle. But he added there have been changes in the funding dynamics of credit unions, and that has included a refocusing on certificates for funding. CDs now represent about 30% of the CU deposit portfolio.

But it’s also an area of risk in that 95% of funding reprices within a year. “Be very mindful of that distribution,” Houle cautioned.