WASHINGTON–A newly released survey of community bankers identifies other banks, including their community bank brethren as their primary competitors, not credit unions.

The report also reveals many community bankers citing the same challenges as credit union leaders.

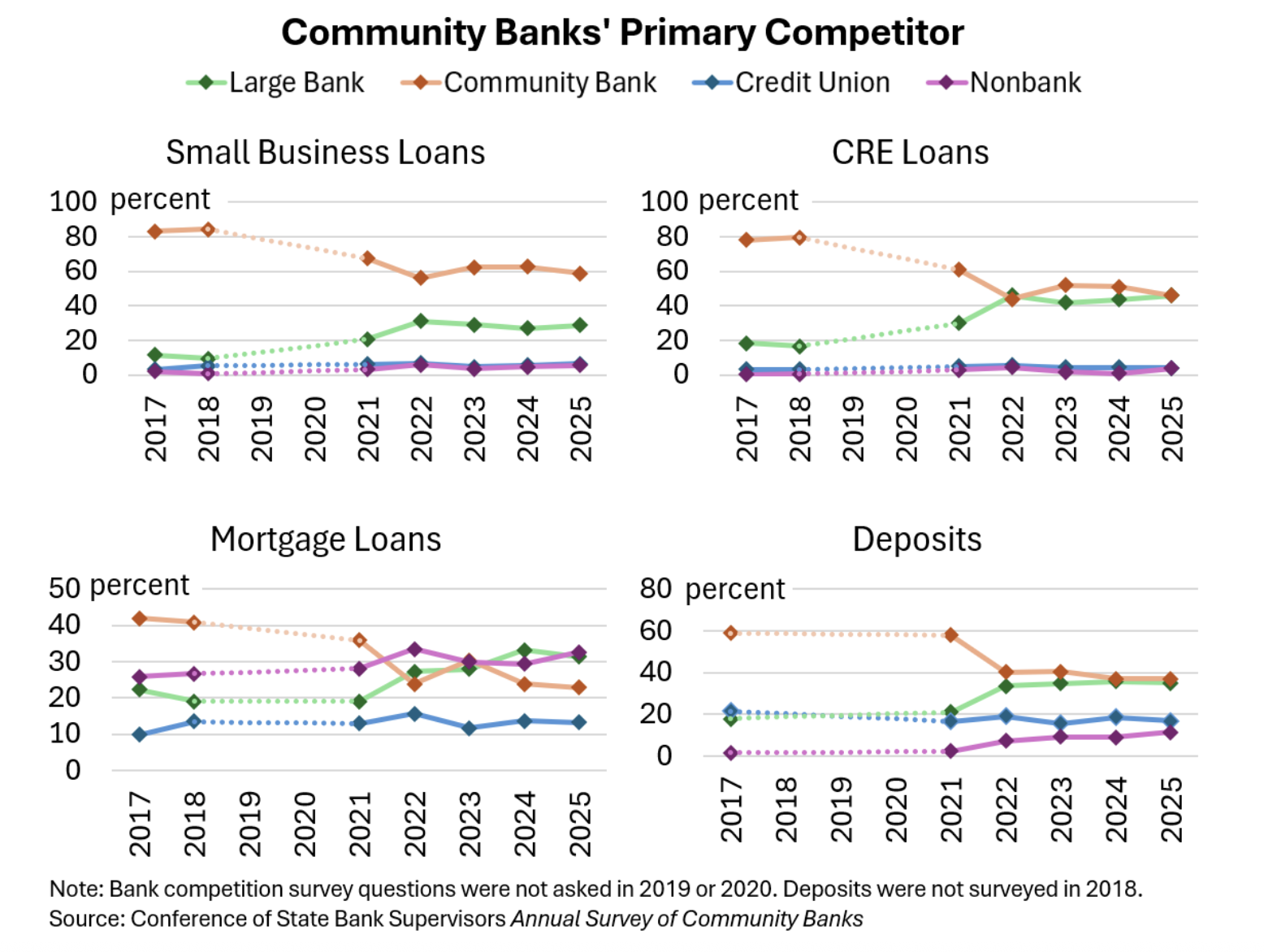

The Annual Survey of Community Banks released by the Conference of State Bank Supervisors (CSBS) indicates credit unions are generally rated significantly below other providers as the biggest competitive threat, a s the chart below shows.

Following release of the survey, America’s Credit Unions issued a statement saying that despite what the survey shows, “…community bank trade groups continue to push a false narrative that credit unions are ‘creeping into their space.’ The data tells a different story.”

Height of Hypocrisy

“It’s the height of hypocrisy,” ACU President and CEO Jim Nussle said in a statement. “Community banks tell Congress that credit unions are a threat, while telling regulators that they’re not even on their radar. Credit unions don’t compete for profits, they compete for people. They serve Main Street families, small businesses, and rural communities that Wall Street ignores and community banks can’t always reach.”

As the report states, “Community banks continued to cite other community banks as their largest competitor—in seven of nine product and service lines—and reported local regional banks as their primary competitor for payment services and in-market nonbanks as their top competitor for wealth management and retirement services.”

Additional Findings

According to the report, key findings from the survey include:

- Net interest margins were cited as the most important external risk facing community banks in the 2025 CSBS Annual Survey. Core deposit growth ranked second among surveyed banks, followed by economic conditions, cost of technology, and cost of funds.

- Regulation, which had been a top external risk in last year’s survey, fell to the sixth spot, as community bankers expressed less concern over regulatory burden amid a changing political landscape.

- “Once again, cybersecurity held the top spot among internal risks facing community banks. Indeed, the share of community bankers reporting this as an extremely important risk (58%) surpassed all other risks—both external and internal—by a healthy margin. Technology implementation and related costs ranked second, while credit replaced liquidity in the third spot,” CSBS said in their statement.

- Bankers continue to report inflation-created challenges as persistent but manageable. While bankers still see the greatest impact from inflation on the cost of deposits, followed by personnel expenses, more respondents cited the effects of inflation on operating expenses in this year’s survey

- Payment services competition showed the largest year-over-year change, with competition from nonbanks without a physical presence in the market increasing by seven percentage points. Nonbanks are now the second-highest form of competition in this area.

- Respondents that received and seriously considered accepting an acquisition offer doubled between 2024 and 2025, rising to 12%. Inability to achieve economies of scale was cited as the primary reason for consideration.

- On average, respondents reported that adhering to safety and soundness practices accounts for the largest share of total compliance expenses, at 27%. Money laundering and consumer protection standards maintained the second- and third-largest shares, at 25% and 23%, respectively, CSBS said.

- Most respondents indicated they would support changing the current deposit insurance framework, with targeted unlimited coverage and increased coverage scoring the highest among alternative solutions. Of those survey respondents favoring an increase to the deposit insurance limit, the majority (72%) viewed a new limit of $500,000 as appropriate.

- According to this year’s survey, credit and debit card fraud was both the most common type of fraud reported and the largest source of dollar losses, followed by check fraud, and identity theft and account takeover, respectively. Together, these three types of fraud account for nearly 88% of total fraud cases and more than 80% of dollar losses.

The full report can be found here.