COLUMBIA, Mo.– The average new college graduate likely won’t be able to afford a home until April 2034 — nearly 10 years after graduation — due to a triple burden of surging home prices, student loan debt and modest entry-level salaries, according to a new analysis released by MortgageResearch.com.

The study, which uses average federal student loan amounts by state from EducationData.org, assumes a 6.53% interest rate for undergraduate loans over a 10-year term, according to the company, and estimates how long it would take graduates in each state to save for a 10% down payment, factoring in average starting salaries, home prices and student loan payments.

Some Wide Differences

The report found, however, some wide differences in the timeline depending on where a person is buying.

For example, MortgaggeResearch.com said that in West Virginia, 2025 college graduates could expect to purchase a home by April 2030 — in about five years. But in Hawaii, where the average 10% down payment tops $98,000, it could take nearly 18 years, which would delay homeownership until February 2043.

“These numbers highlight how geography influences the path to homeownership for first-time buyers,” Tim Lucas, lead analyst at MortgageResearch.com said in a statement. “Where you land your first job and choose to live can be just as important as your degree. But it’s not just about home prices. Even in more affordable markets, it’s the weight of student loan debt that often dictates how long new grads will wait before they can buy a home.”

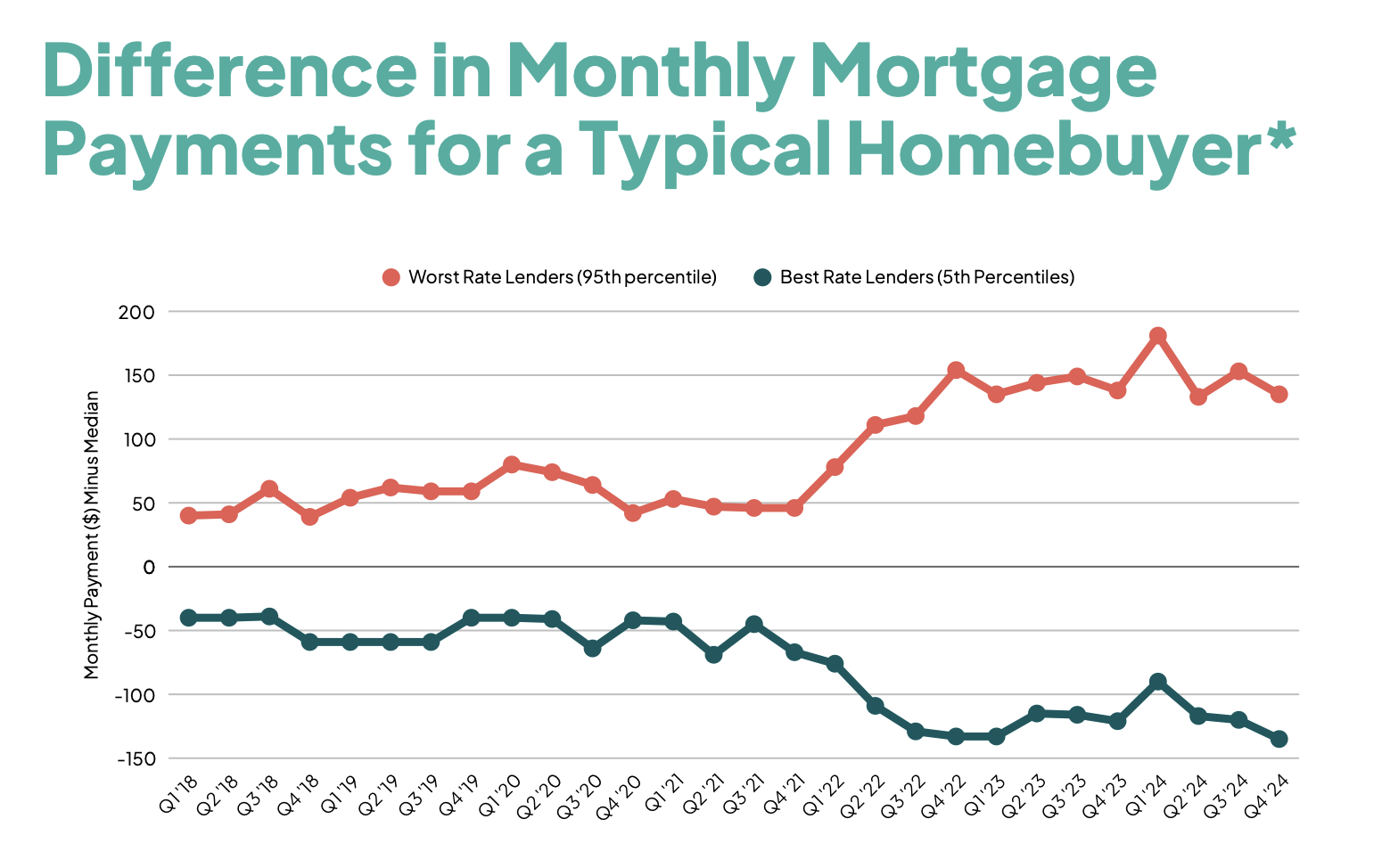

Another Factor

The availability of mortgage credit is another factor playing a role. The company cited an April update on mortgage credit availability released as part of the Mortgage Bankers Association’s Mortgage Credit Availability Index (MCAI) showed that while credit conditions have loosened since 2023, they’re still relatively tight.

To arrive at its forecast, MortgageResearh.com said its study assumes graduates save 13.8% of their gross income — triple the national average, according to the U.S. Bureau of Economic Analysis — toward student loans and a future down payment.

“With an estimated annual salary of $64,598, this year’s graduates who don’t have student loans could save $743 per month. But based on a typical loan payment of $410, they would only have $333 left to put towards a down payment,” the company said. “As a result, the analysis suggests that student loan debt delays homeownership by an average of four years and eight months. Without student debt, a graduate could buy a home by August 2029. With debt, the target shifts to April 2034.

A Significant Delay

MortgageResearch.com further noted that even in markets with lower home prices, student loan debt can significantly delay homeownership. In Mississippi and West Virginia, affordable housing is offset by modest starting salaries and limited savings, leaving grads years away from affording a down payment.