WASHINGTON — An analysis authored by two economists with the American Bankers Association argues that credit unions have significantly expanded commercial lending activity in recent years, raising concerns about risk, regulatory oversight and alignment with their statutory mission.

The report, written by Daniel Brown and John Vermillion, states that credit unions were historically created to provide basic financial services to consumers of “modest means,” but policy changes beginning in the 1990s loosened membership requirements while placing limits on business lending.

Despite those limits, the authors contend commercial lending has grown substantially, particularly among larger institutions, low-income designated (LID) credit unions and those that have acquired banks. Credit unions that have purchased banks now hold nearly 20 times more commercial loans than those that have not, according to the analysis.

Statutory Cap Cited

The report points to a statutory cap on member business lending established under 1998’s Credit Union Membership Access Act as a key guardrail intended to keep credit unions focused on consumer lending. However, the authors argue that regulatory changes — including a 2016 rule by the National Credit Union Administration that eased the waiver process to exceed the cap — have contributed to increased commercial lending.

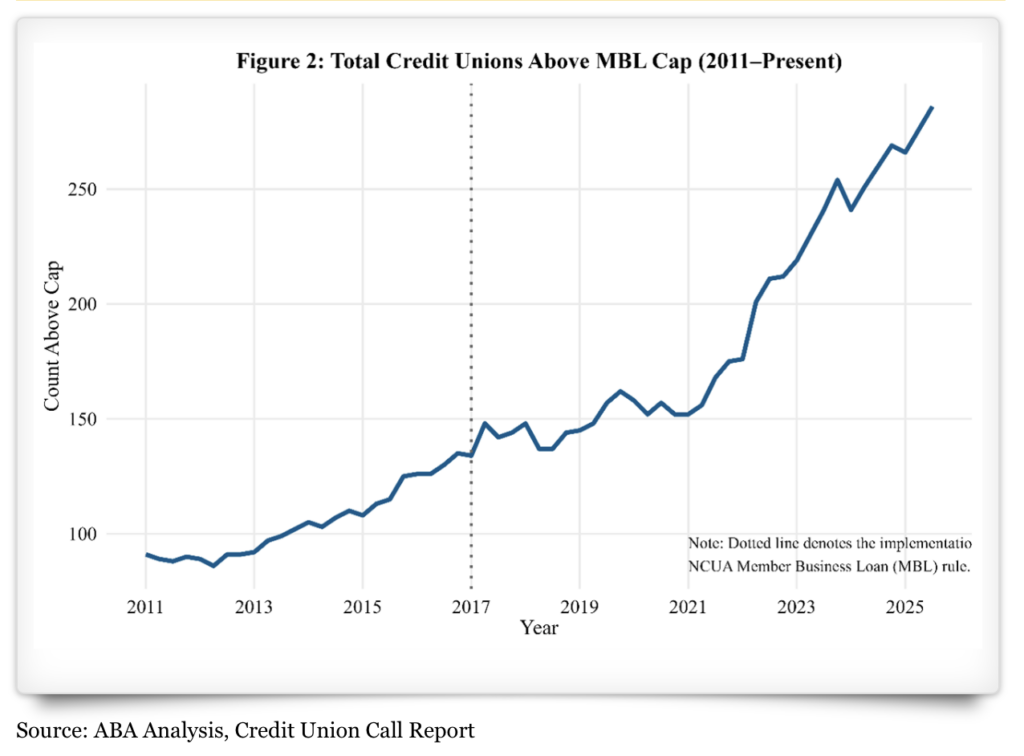

According to the analysis, the number of credit unions exceeding the lending cap rose from 126 in early 2016 to 286 by the third quarter of 2025. Growth has been concentrated among larger institutions, with a rising share of credit unions with more than $250 million in assets surpassing the cap.

Growing Number of LICUs

The report also highlights the growing use of the low-income designation status, which exempts credit unions from the cap. The share of credit unions with that designation increased from about 6% in 2000 to more than 54% by 2025, with those institutions holding significantly higher levels of commercial loans.

Brown and Vermillion warn that the expansion into commercial lending could introduce additional risks, noting that credit unions have limited experience managing such portfolios through economic downturns. They also argue that the NCUA does not have the same level of expertise in supervising commercial lending as bank regulators.

The authors cite guidance from the Office of the Comptroller of the Currency outlining the complexities and risks associated with commercial real estate lending, including market volatility, concentration risk and governance responsibilities.

Policy Recommendations Made

The report concludes with policy recommendations, urging Congress to conduct greater oversight of credit union activities and evaluate whether current practices align with their intended mission. It also suggests lawmakers consider whether changes to the industry’s tax status or regulatory framework may be warranted.

The analysis frames the issue as a shift in the role of credit unions, with the authors stating that increased commercial activity could move institutions away from their traditional focus on member-oriented financial services and toward a more complex and potentially riskier business model.