SAN FRANCISCO–Credit delinquencies in the 30–59 days past due (DPD) category rose year over year in May 2025 across VantageScore Nearprime, Prime and Superprime segments, according to a new report.

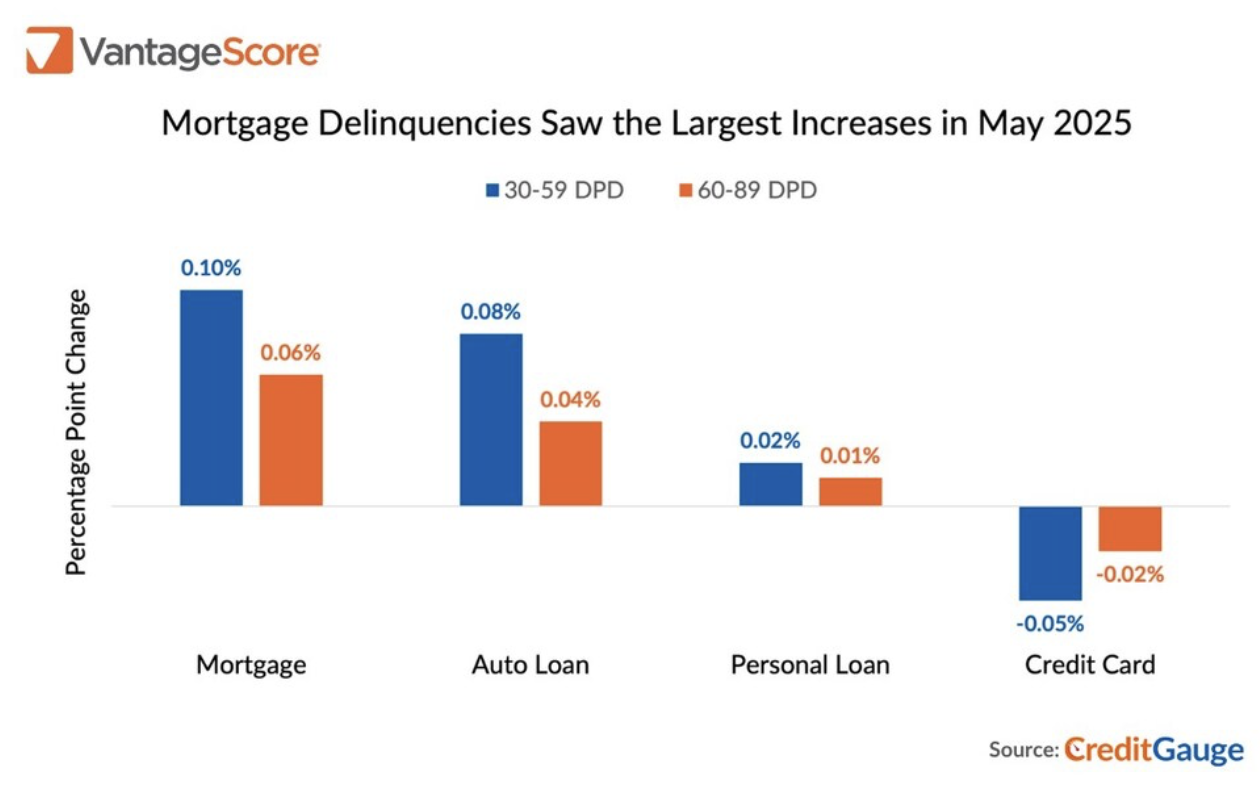

The largest annualized increase was in the early-stage delinquency category (30 to 59 days past due). Delinquencies rose from 0.92% in April to 1.03% in May, suggesting early signs of financial strain as borrowers seemingly deprioritized mortgage payments, according to VantageScore.

‘Potential Strain’

“The rise in early and mid-stage delinquencies this month indicates potential financial strain among some consumers,” Susan Fahy, executive vice president and chief digital officer at VantageScore, said in a statement. “While consumer behavior generally remains positive, particularly among younger borrowers, mortgages may be an area to watch for increasing credit stress, particularly for traditionally less-risky segments with credit scores above VantageScore 660.”

Other Borrowers Affected

The analysis further noted that although subprime delinquencies dropped slightly year over year, elevated late-payment rates in other VantageScore tiers suggest that short-term financial stress may be starting to impact even lower-risk borrowers, the company said in releasing its latest numbers.

According to the new report, in the 60–89 DPD category, mortgages recorded modest increases. In the 90–119 DPD bucket, delinquencies fell across all credit products from April to May, with credit cards and mortgages having the largest declines of 0.02%.

Additional Findings

In addition, the new data show:

- The average credit balance rose to $106,000 in May, marking an increase of $249 (+0.24%) from April — and the fifth straight month at a five-year high point. Year over year, balances grew by $1,479 (+1.4%) compared to May 2024. Mortgage balances showed the largest uptick among product lines, rising 2.8% year over year.

- The average VantageScore 4.0 held steady at 702 in May, inching up only 0.04 points from April.

- The share of VantageScore Prime and VantageScore Superprime borrowers has declined from 64.5% to 63.8% since May 2023, reflecting slight credit-quality deterioration in these segments.