KENNEWICK, Wash. — A survey conducted by the Endangered Small Credit Union Defense (ESCUD) has reinforced the widely held belief that regulatory requirements tied to the Home Mortgage Disclosure Act are imposing significant costs on small credit unions and, in some cases, influencing their lending practices.

The survey, led by Doug Wadsworth, president of Tri-Cities Community Credit Union, gathered responses from leaders of small credit unions, many of which are not currently required to comply with HMDA reporting due to low asset size, limited mortgage volume, or geographic factors.

Wadsworth said the effort aims to provide data regulators could use to revisit HMDA reporting thresholds for smaller institutions.

“HMDA…makes sense for big CUs, but what about the impact on small, low volume credit union lenders?” Wadsworth said in a statement. “ESCUD wants to correct that, allowing the CFPB to again modify the thresholds at small CUs, freeing us up to offer more mortgage services to our small communities and memberships, consistent with the March 2026 Executive Order promoting Mortgage Access.”

Compliance Burden Viewed as Significant

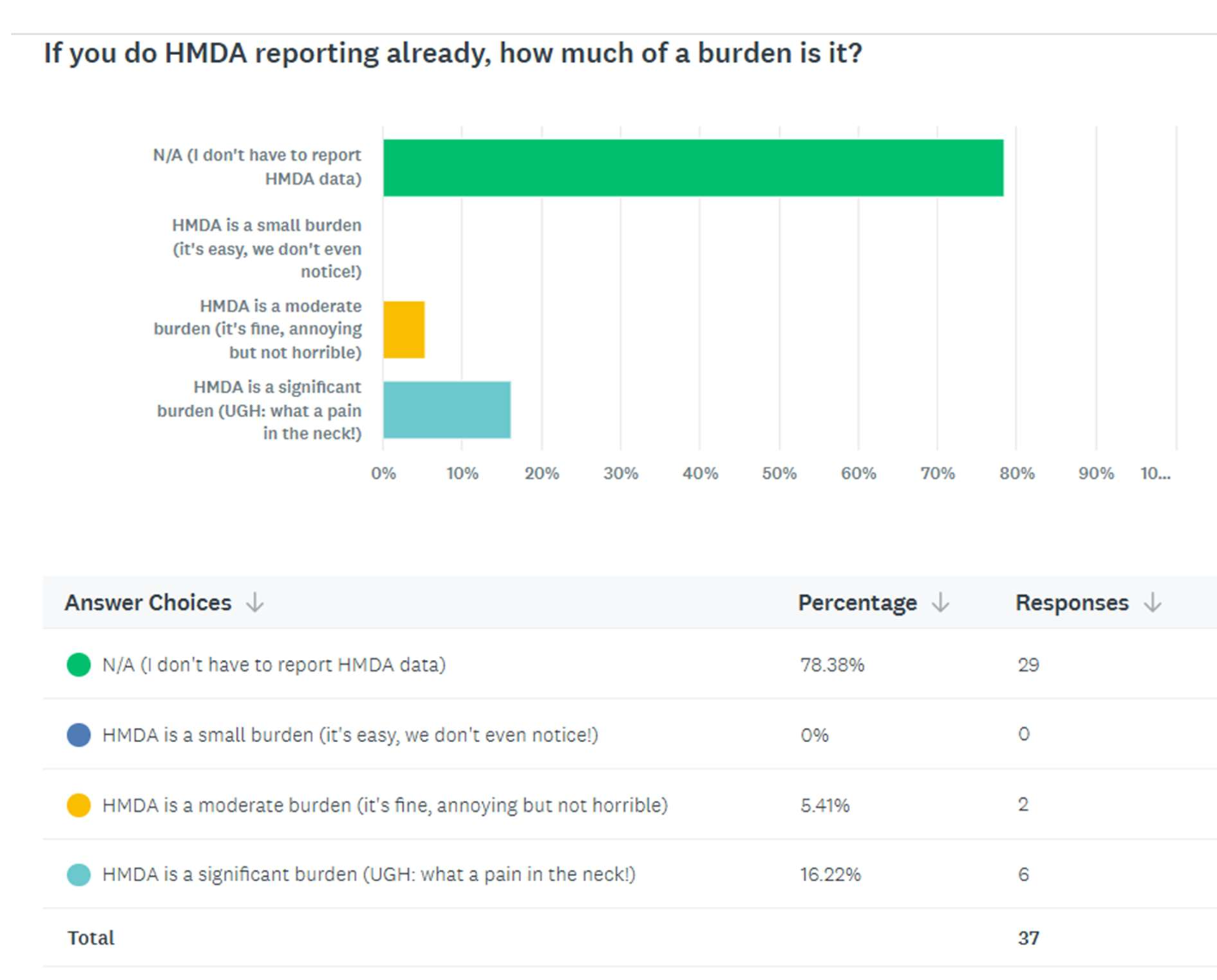

Among respondents already subject to HMDA reporting requirements:

- 75% described the compliance burden as “significant.”

- No respondents characterized compliance as easy or inexpensive.

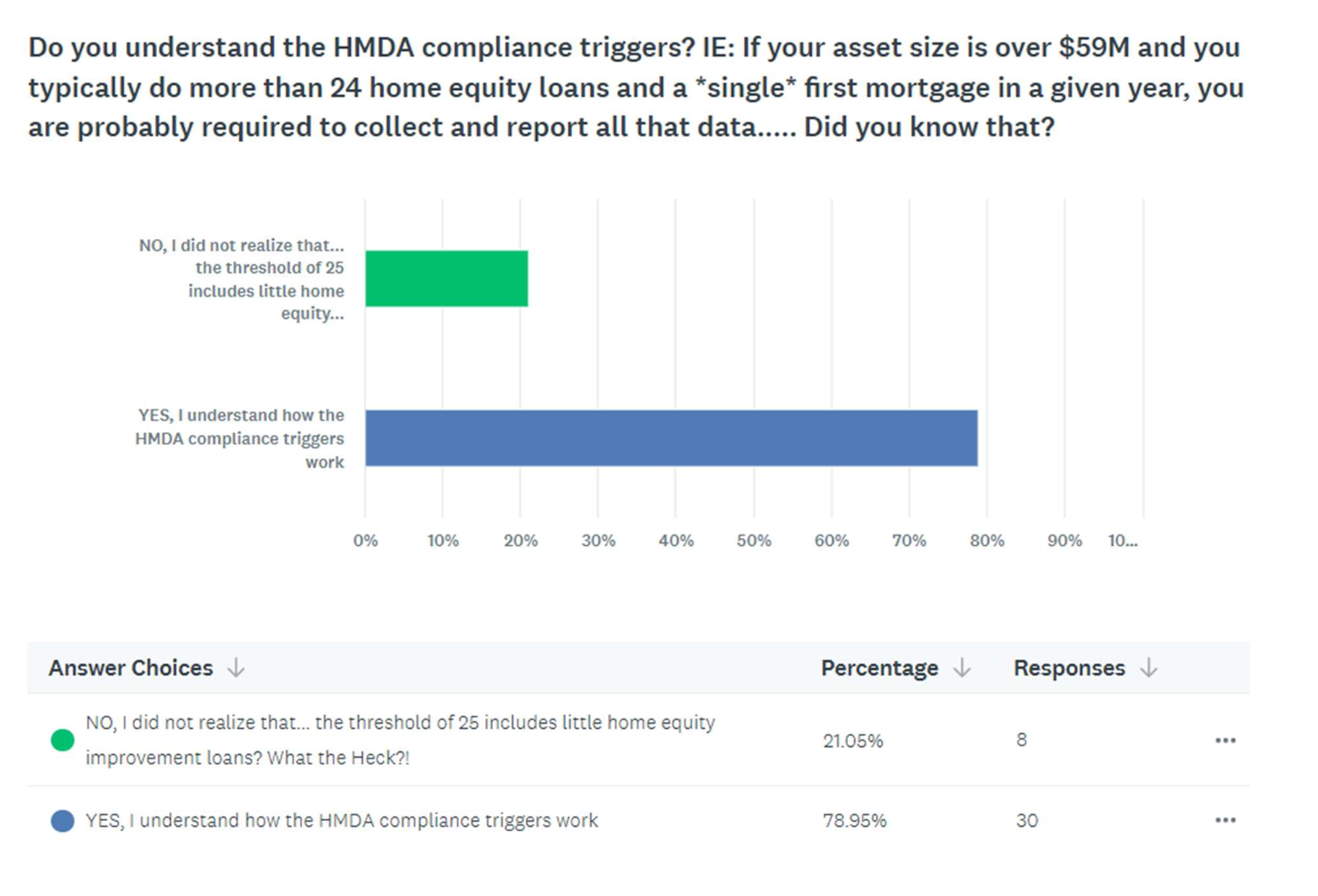

The survey also highlighted confusion around reporting thresholds. About 20% of respondents were unaware that small home equity loans count toward HMDA thresholds, with some realizing during the survey that they may already be required to report.

Wadsworth cited his own experience as an example.

“An NCUA examiner noted that as my asset size had just reached $50 million it had triggered compliance for me, even though I did only about a dozen in-house first mortgages per year,” he said. “So yeah, that was depressing.”

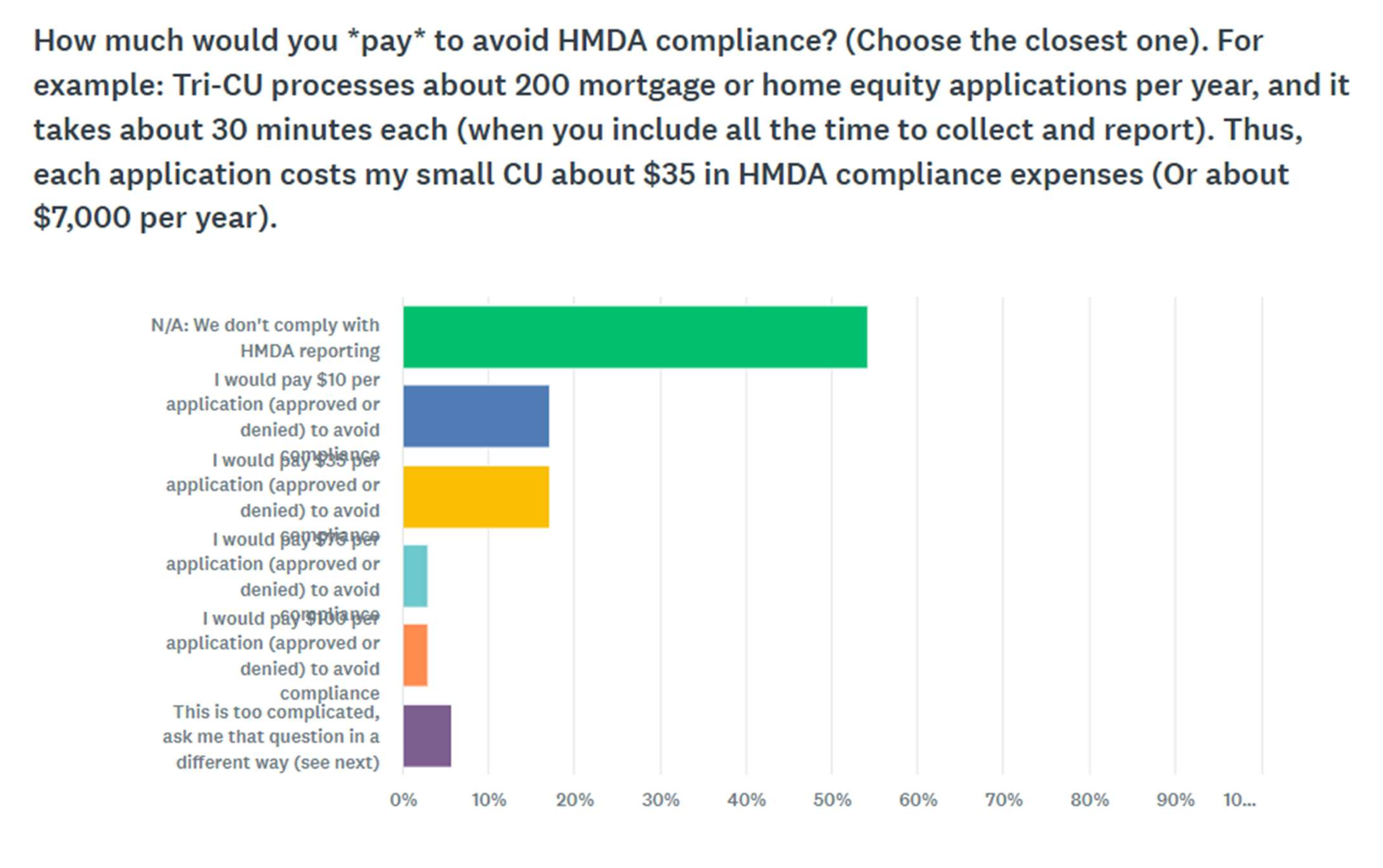

Wide Range of Estimated Costs

Respondents reported a wide range of estimated costs associated with HMDA compliance:

- Some estimated they would pay $10 per application to avoid compliance.

- Others cited $35 per application.

- Some said costs could reach as high as $100 per application.

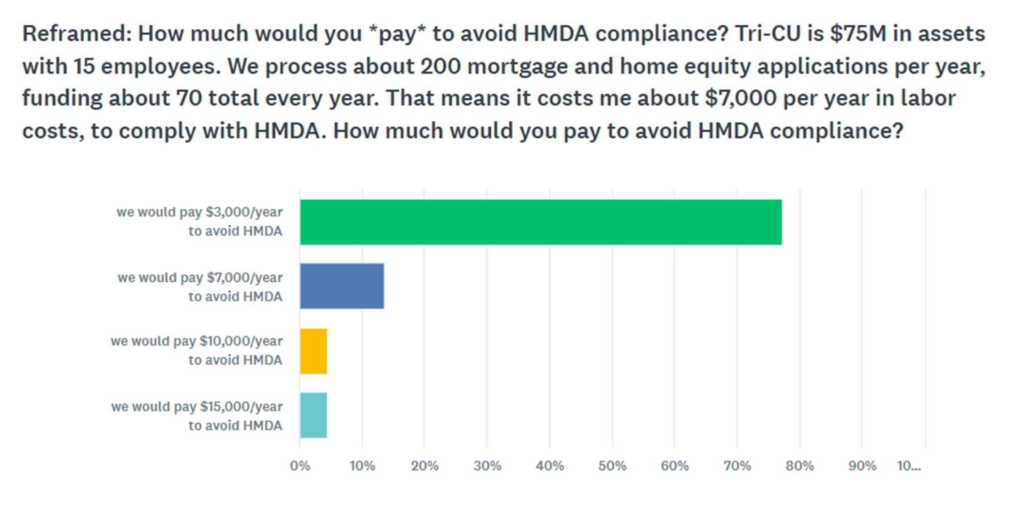

Wadsworth said his own credit union incurs about $35 per application, totaling nearly $7,000 annually based on roughly 200 applications per year.

When asked about total annual costs they would be willing to pay to avoid compliance:

- Many respondents cited about $3,000 annually.

- One small credit union indicated it would pay up to $15,000.

Wadsworth noted that for some institutions, even modest compliance costs can have an outsized impact.

“At many small CUs, $5,000 could represent 5% to 10% of their net income, especially if they are struggling with profitability,” he said.

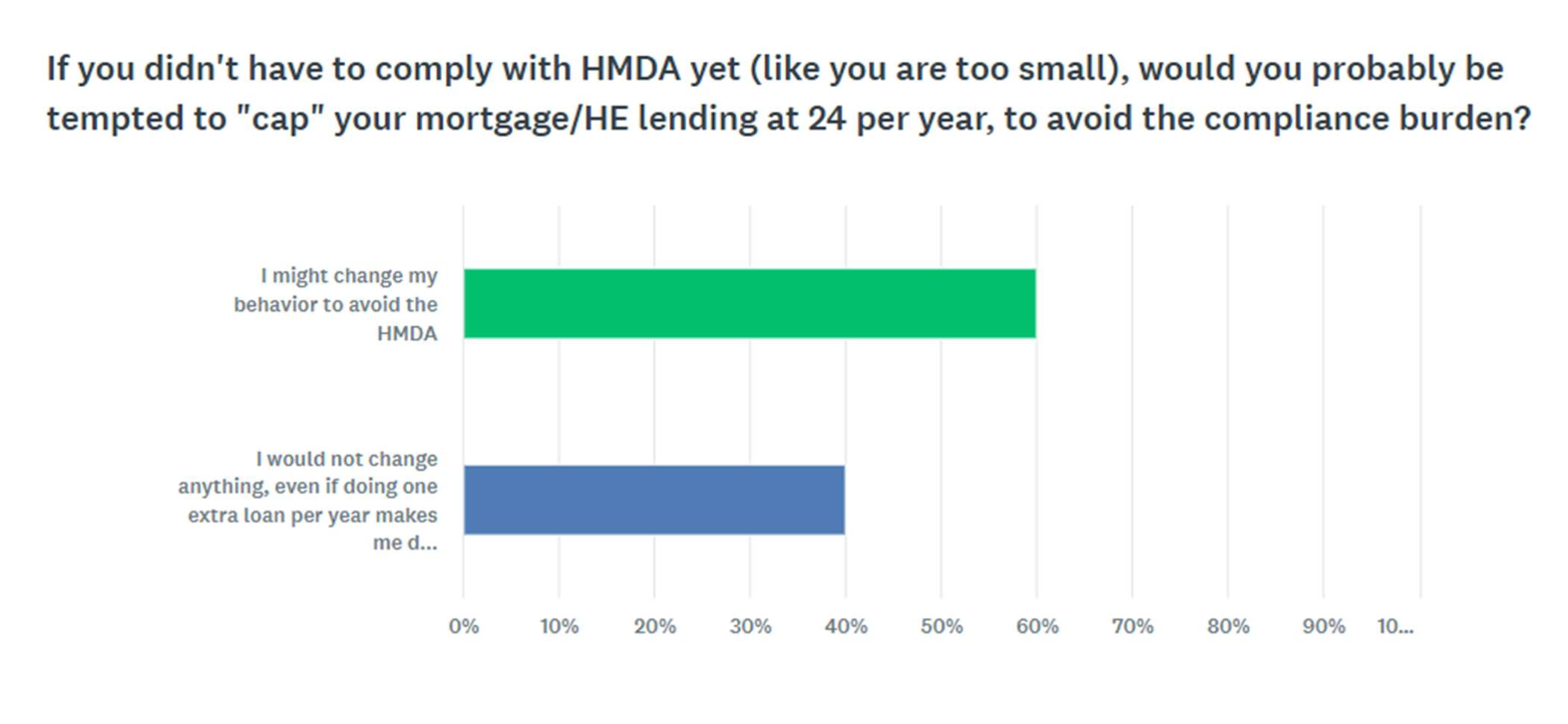

Survey Points to Changes in Lending Behavior

The survey also found that 60% of respondents said they would likely alter their behavior to avoid reaching HMDA reporting thresholds.

Wadsworth said his own credit union adjusted its lending practices in response to the requirements.

“We dropped deeds as security for many of our home improvement loans, switching to UCC instead, despite UCC being a less secure alternative, to try and avoid the compliance burden,” he said.

Another respondent, identified as a small credit union CEO, reported similar changes.

“I do not have the budget to hire people to process and comply with HMDA reporting,” the CEO said. “We changed our practices to avoid HMDA reporting. We stopped doing purchase mortgage loans and watch our volume on seconds and refinances.”

Wadsworth said such changes suggest broader implications for consumers.

“The HMDA compliance burden is literally reducing mortgage availability to the public, from the most hyper-local community institutions: small credit unions,” he said. “Fewer options and less competition are bad for everyone.”

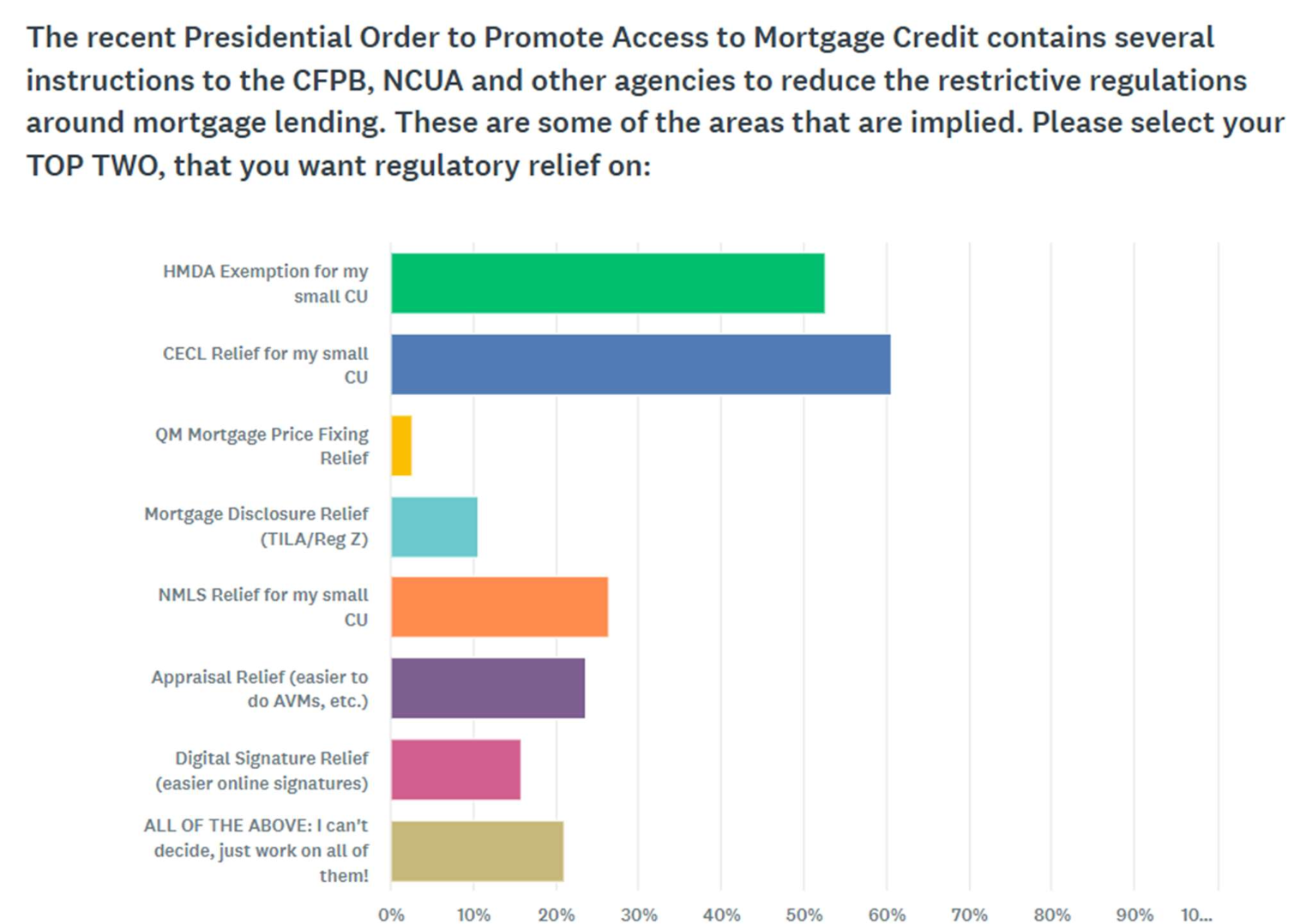

Regulatory Relief Priorities

The survey also asked respondents to identify regulatory relief priorities in light of a March 2026 executive order focused on expanding mortgage access.

HMDA relief ranked as the top priority among respondents, according to Wadsworth, with other regulatory concerns cited less frequently.

He added that the survey results also underscored frustration with other compliance requirements.

“I made an error by including CECL on the list, which isn’t implied anywhere in the executive order, but it sure demonstrated how frustrating of a burden CECL is to small CUs,” Wadsworth said.

ESCUD said it plans to use the survey findings to advocate for changes to HMDA reporting thresholds for smaller credit unions, arguing that current requirements may be limiting mortgage availability in local communities served by those institutions.

One Response

You can’t report 12 mortgages? HMDA data isn’t as meaningful unless everyone does it. The survey wasn’t really needed to know people think it’s a hassle. Large CU’s would say the same thing. We should support having the data to ensure fair lending, access to credit, that everyone’s being served, etc.