CHICAGO–A new report from the Financial Health Network has found the share of households who are “financially healthy” has not meaningfully increased since 2022.

The organization said its analysis has uncovered a “mixed picture” of modest but fragile financial health improvements in the short term paired with a lack of progress and deep-seated disparities over the long term.

“These signals underscore the urgent need for sustained and substantial attention and investment to prevent any backward slide – especially as economic and policy conditions shift – and to move from incremental change to transformative improvement,” the Financial Health Network said in releasing its new “2025 U.S. Trends Report: Can Short-Term Gains Lead to Lasting Progress?”

The report includes a number of key findings, including:

Financial Health Challenges Remain Entrenched

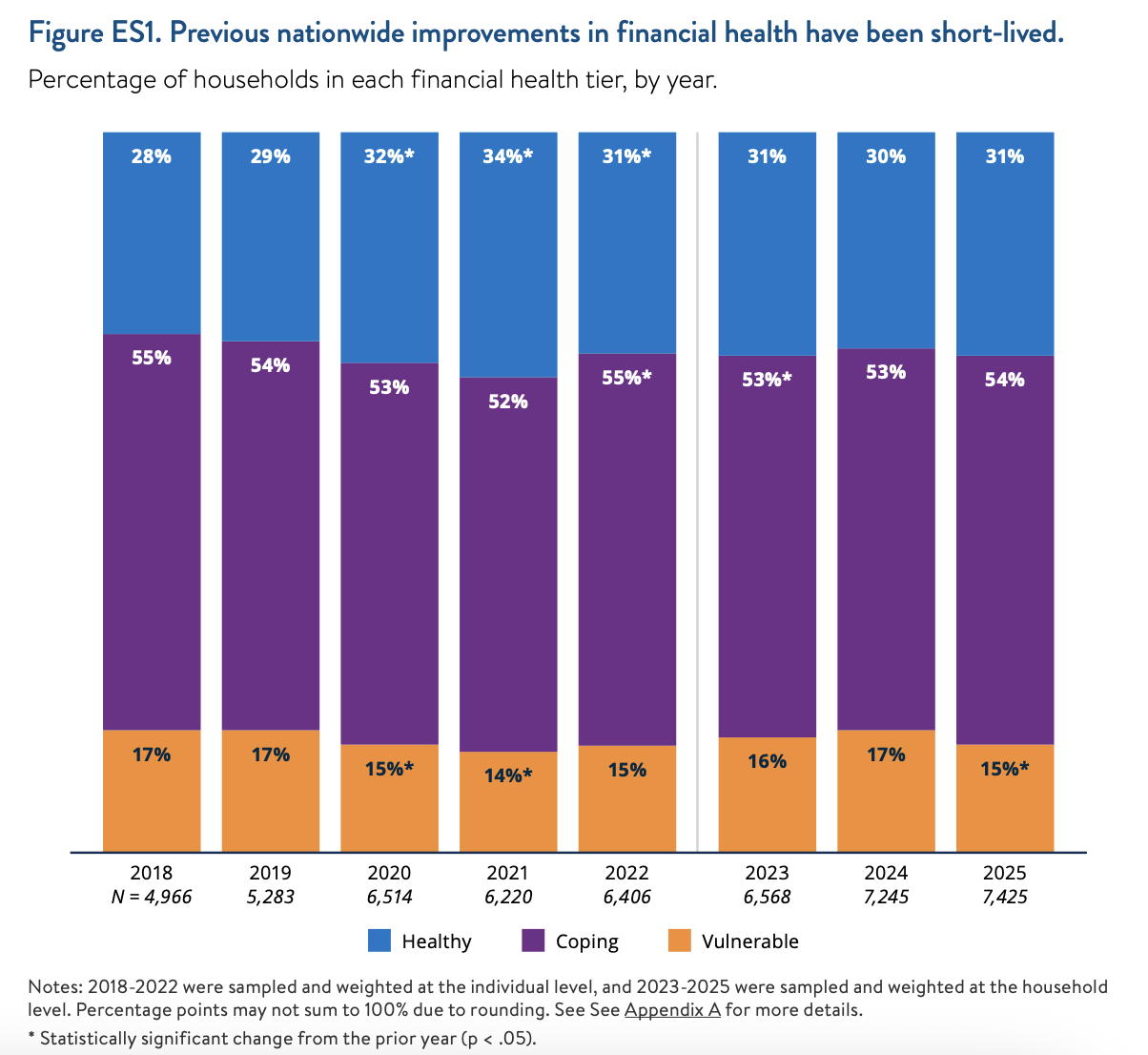

Eight years of Pulse data show that financial health improvements have proved fleeting, FHN said.

The report found:

• Only 31% of households were financially healthy in spring 2025, consistent with recent years and only slightly higher than pre-pandemic levels.

• The only time the share of financially healthy households increased substantially was in 2020 and 2021 – years characterized by unprecedented levels of government assistance and restricted consumer spending at the height of the COVID-19 pandemic.

• The financial health gains from these interventions wore off quickly as much of that government support ended.

A Modest Decrease in Financial Vulnerability

Savings ability and debt manageability both improved slightly, the report states.

It found:

• The percentage of households who spent less than their income over the past 12 months rose from 47% to 49%.

• Meanwhile, the share who spent more than their income declined from 24% to 23%.

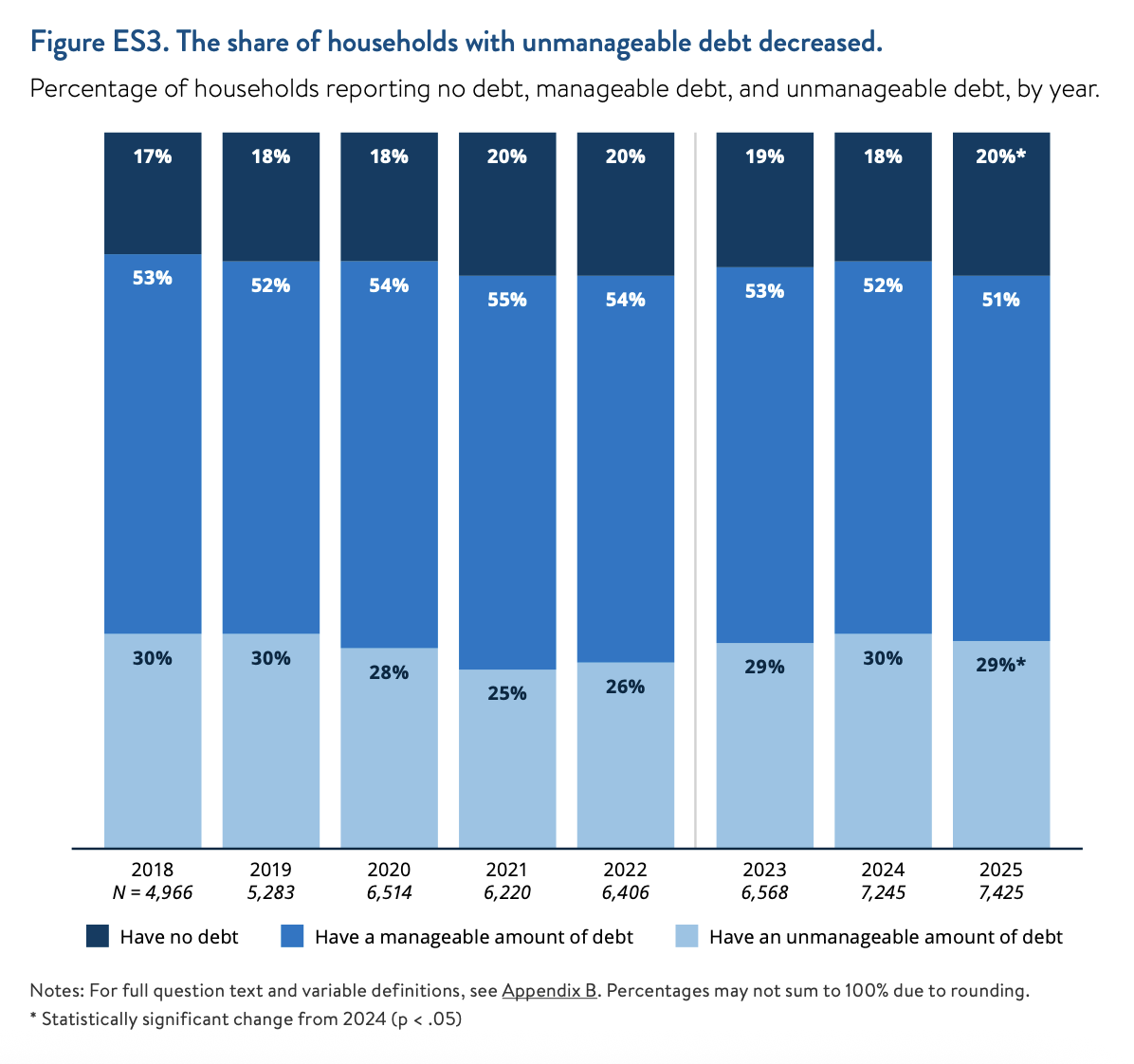

• The percentage of households reporting an unmanageable amount of debt decreased from 30% to 29%.

Growing Concerns About Insurance

Household confidence in insurance coverage continued to decline, the Financial Health Network reported.

The report shows:

• The share of households who were at least moderately confident that their insurance policies were sufficient to cover an emergency fell from 59% to 56%.

• This decline continues a gradual downward trend stretching back to at least 2018.

• Households who experienced natural disasters in the past year were even less confident in their insurance coverage.

Student Loan Borrowers’ Credit Scores Take a Hit

According to the report, loan servicers resumed reporting late payments, impacting borrowers’ credit scores.

• The percentage of households with student loans reporting that their credit score was “good,” “very good,” or “excellent” dropped from 69% to 65%.

• There was no statistically significant change in credit scores among households without student loans.

Turning Modest Gains Into Meaningful Progress

“After two years of rising distress, the past year’s modest decrease in financial vulnerability signals that cooling inflation and a stable job market have given some struggling households breathing room in their budgets,” the organization said in summarizing its findings. “Despite this progress, the share of households who are financially healthy has not meaningfully increased since 2022.

“More than two-thirds of U.S. households remain financially unhealthy, and Pulse data highlight other areas for concern. Consumer confidence in insurance is declining, struggling student loan borrowers face the resumption of collections activities, and forthcoming changes to Medicaid and SNAP are poised to reduce access to healthcare and food for millions,” the analysis continued. “Eight years of Pulse data have made one thing clear: Without substantial new investment in the financial health of the most vulnerable groups, meaningful progress is unlikely to last. We encourage industry, community, and policy leaders to use these findings to shape effective cross-sector strategies – working together to ensure that this year’s decline in financial vulnerability continues in 2026 and beyond.”