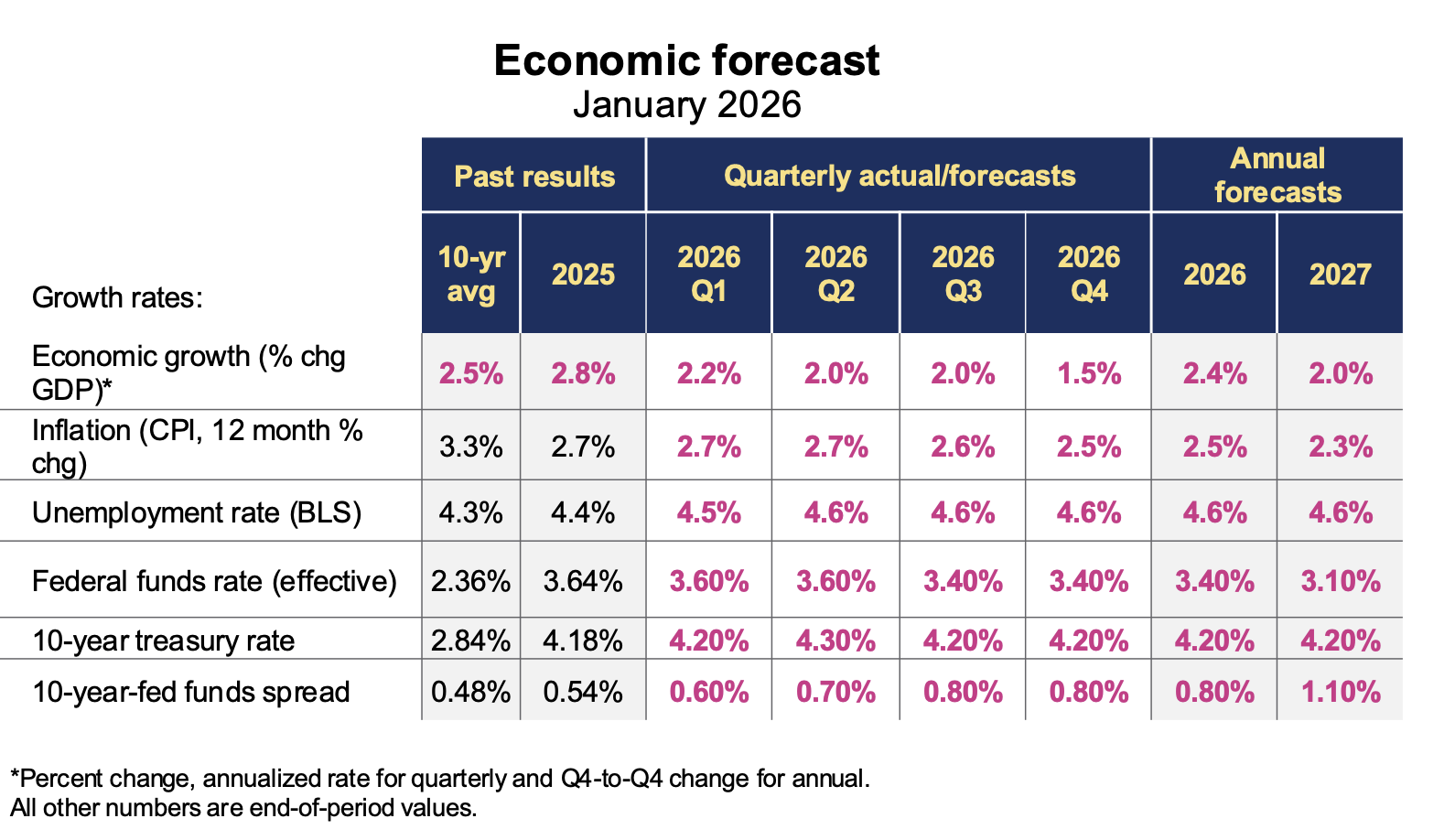

MADISON, Wis.— A new economic analysis from TruStage projects moderate economic growth, easing interest-rate pressure and improving credit union performance trends over the next two years, even as inflation and credit quality risks remain elevated.

The December 2025 Credit Union Trends Report, based on September 2025 data, examines macroeconomic conditions and their impact across lending, savings, real estate and industry structure.

Economic Trends

TruStage forecasts real gross domestic product to grow 2.4% in 2026, slower than 2025’s 2.8% pace but still above the long-run trend of about 2%.

Growth is expected to be supported by expansionary fiscal policy, less-restrictive monetary policy, deregulation and investment in artificial intelligence infrastructure, the analysis states.

Inflation is projected to remain stubbornly above the Federal Reserve’s 2% target, averaging 2.5% in 2026, as tariff-related costs and slow labor-force growth put upward pressure on wages.

The unemployment rate is expected to edge up to 4.6% by the end of 2026, reflecting slower labor-demand growth and constraints on labor supply, notes the foreocast, which adds that the Federal Reserve is expected to lower the federal funds rate by 25 to 50 basis points in 2026, bringing policy closer to a neutral stance near 3%.

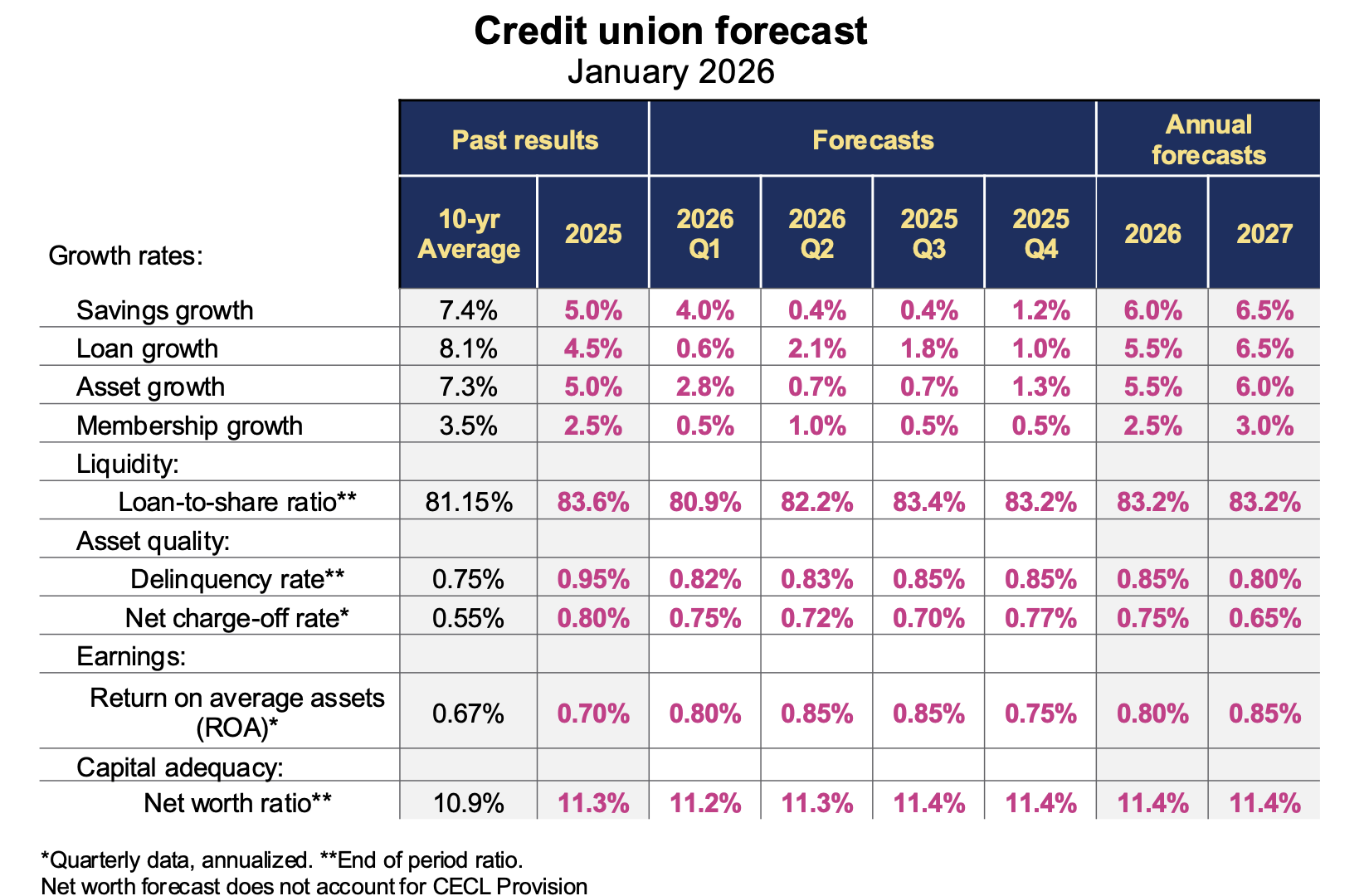

Below is a look at how TruStage said credit unions perfromed by category:

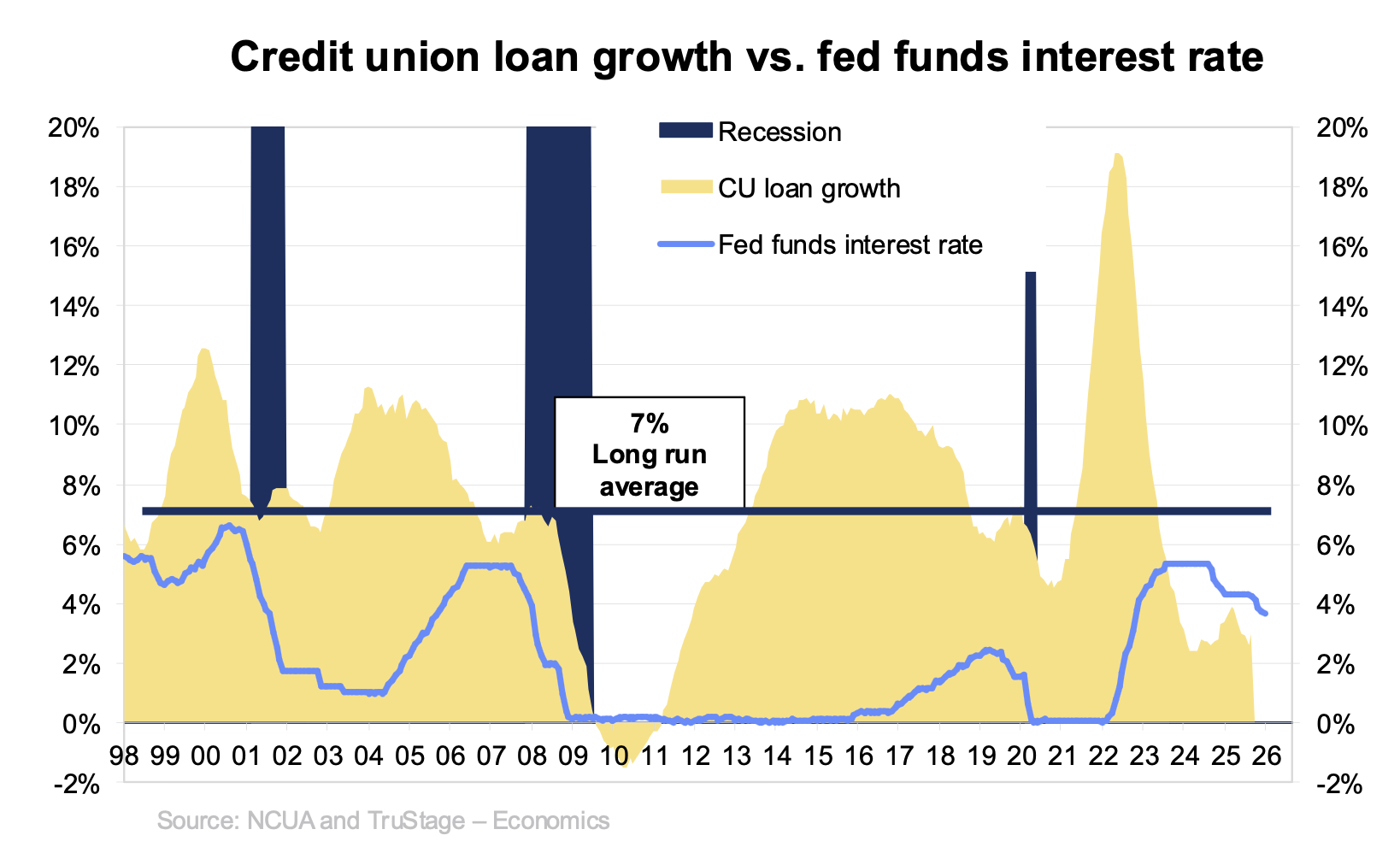

Total Credit Union Lending

Loan growth, currently below historical norms, is projected to strengthen as interest rates decline and repayment activity tied to the 2022 lending boom subsides.

Credit union loan balances are growing at roughly 3% today, compared with a long-run average near 7%, the report states.

TruStage forecasts loan growth to rise to 5.5% in 2026 and 6.5% in 2027, reflecting the delayed effects of monetary easing. The report notes that historically, a five-percentage-point decline in the federal funds rate boosts credit union loan growth by about 3.5 percentage points over two years, illustrating the lagged effect of rate cuts.

Consumer Installment Credit

Credit union credit card balances declined 1.9% in September on a seasonally adjusted annualized basis, well below the long-run average growth rate of roughly 5.5%.

According to the Trends Report, higher borrowing costs and economic uncertainty discouraged consumers from carrying balances, highlighting how restrictive monetary policy slows credit creation.

TruStage expects consumer credit growth to rebound in 2026 as job growth stabilizes and interest rates decline.

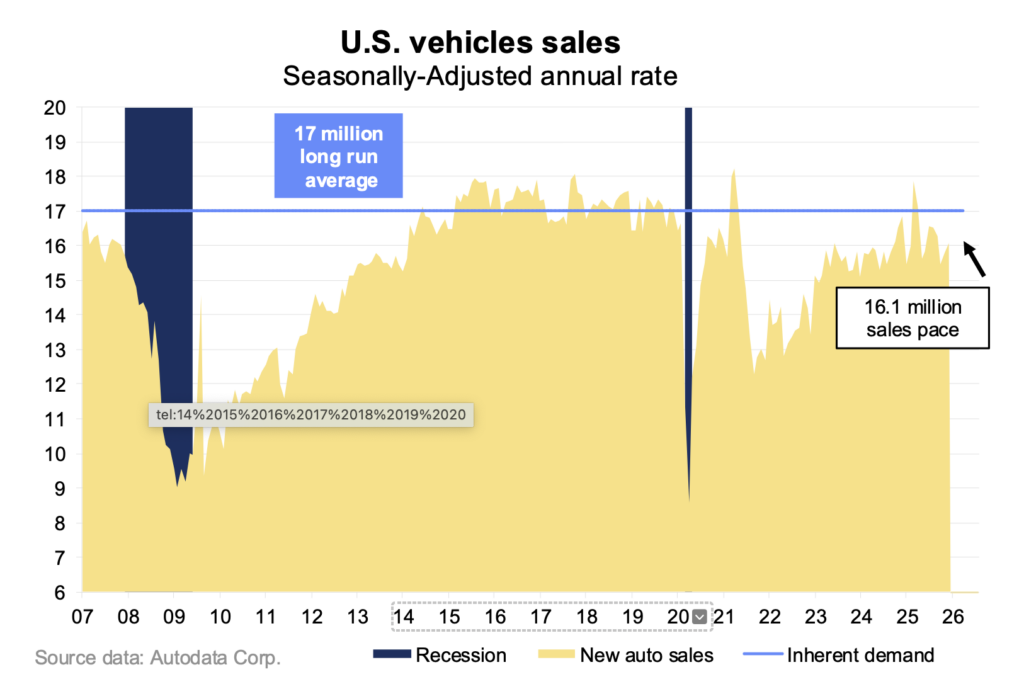

Vehicle Loans

New-auto loan balances fell 6% year over year, reflecting elevated repayments from the 2022 auto-loan surge and tighter underwriting amid rising delinquencies.

Liquidity pressures pushed loan-to-savings ratios to about 84%, prompting some credit unions to scale back lending, the report states.

Vehicle sales are expected to decline about 1% in 2026 due to higher auto prices, labor-market risks and weaker stock-market returns, according to the forecast.

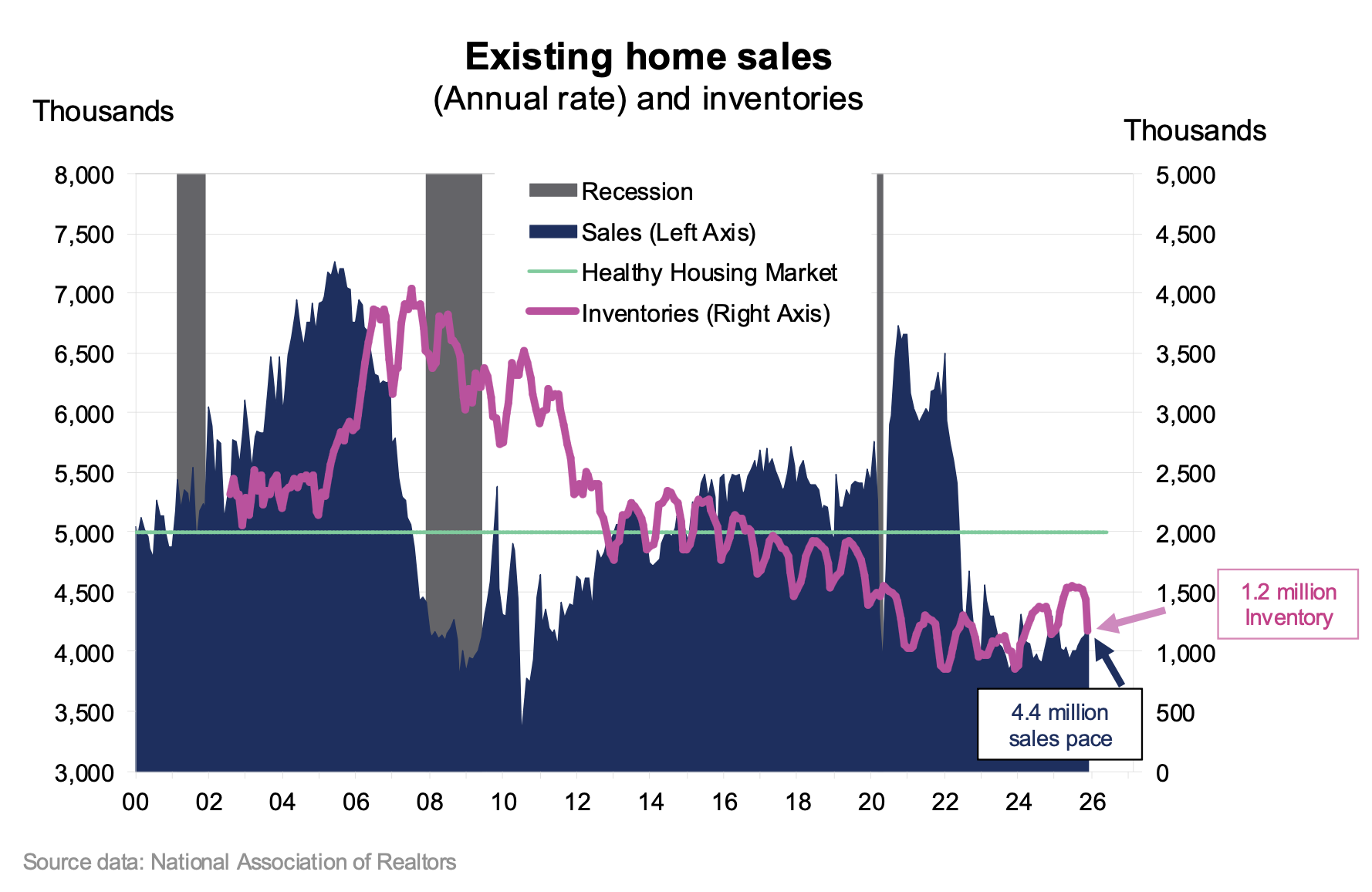

Real Estate Information

The Trends Report notes the housing market ended 2025 stronger, with existing-home sales rising to a 4.35 million annual rate in December.

Mortgage rates declined to 6.10% in January 2026, down from 6.96% a year earlier, helping draw buyers back into the market.

Despite price gains, real home prices are falling when adjusted for inflation, and housing demand is expected to remain below long-term averages due to affordability challenges, the forecast is projecting.

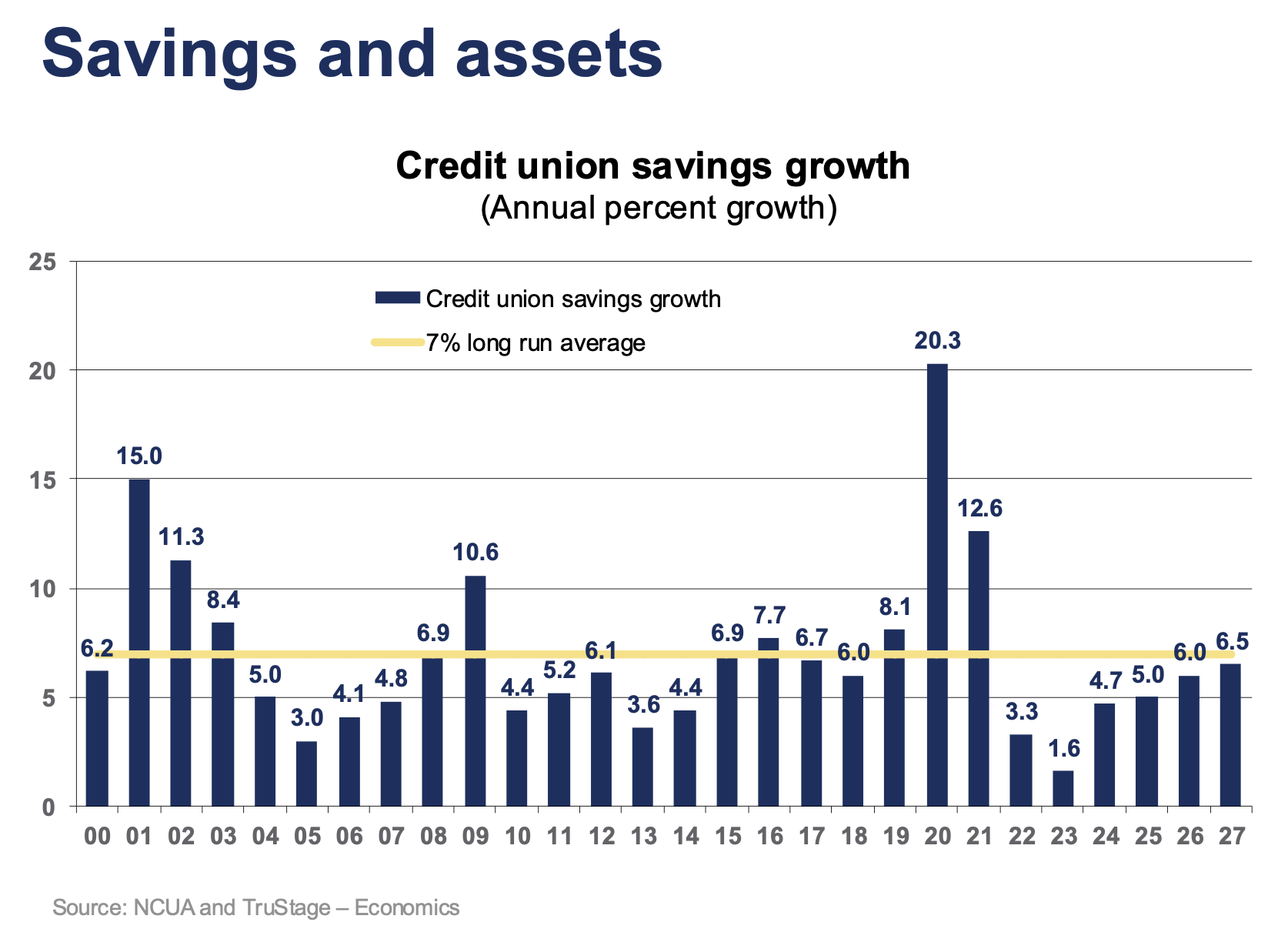

Savings and Assets

Savings growth has lagged historic norms, with balances rising 5% year over year, below the 7% long-run average.

The Trends Report shows a shift toward higher-cost share certificates—now nearly 29% of deposits compared with 14% in 2021—has increased funding costs for credit unions.

Savings are projected to grow 6% in 2026, supported by rising real incomes and more competitive deposit rates, providing needed liquidity after tight conditions in 2025, the report adds.

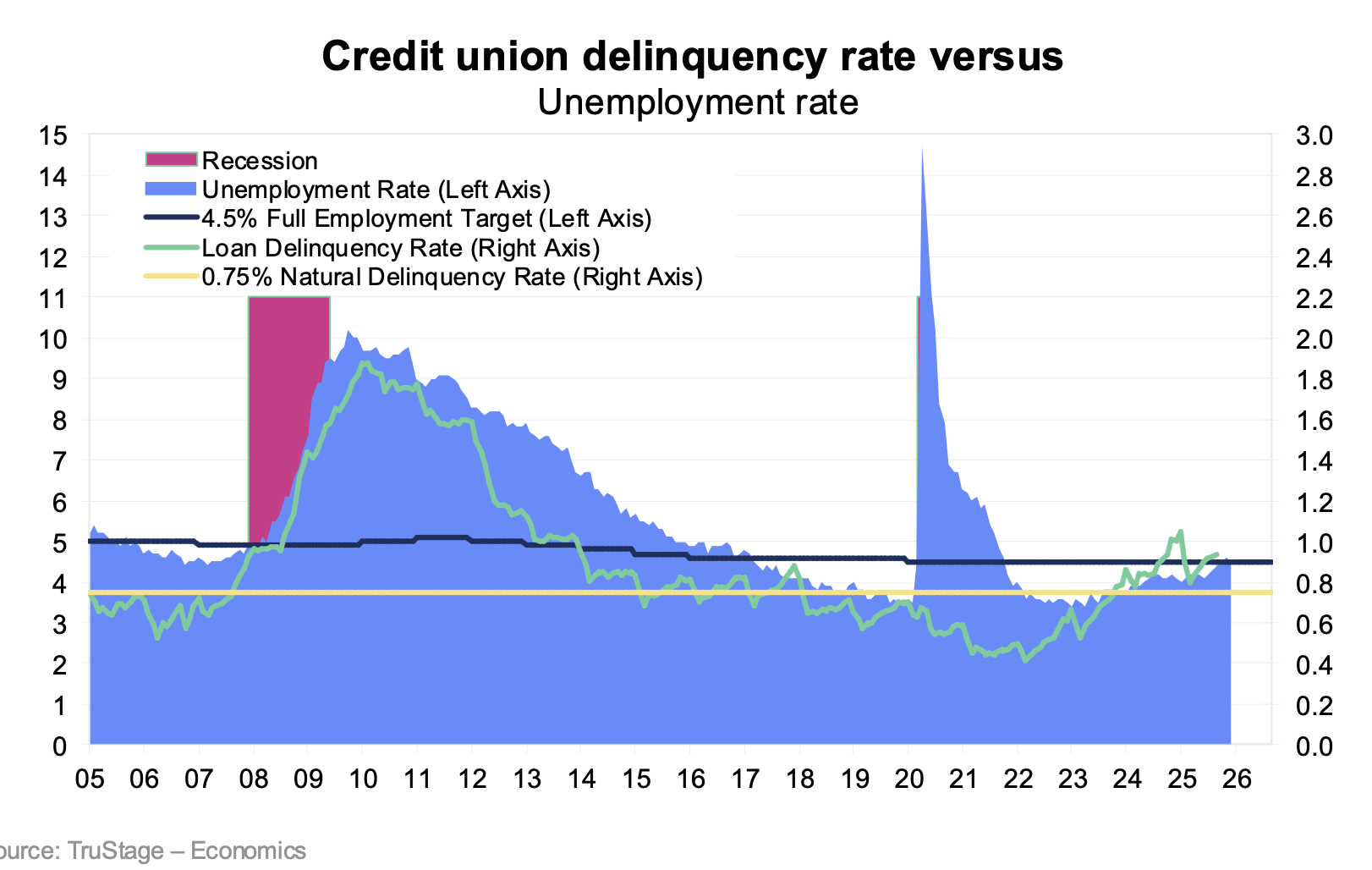

Equity and Other Key Measures

Delinquency rates rose to 0.94% in the third quarter of 2025, above the long-run “natural rate” of 0.75%, driven by factors including rising unemployment, higher living costs and the resumption of student-loan payments, according to the Trends Report

Loan quality is expected to improve as higher-risk 2022–23 loan vintages age out of portfolios. Delinquencies are forecast to decline to 0.85% in 2026 and 0.80% in 2027, while charge-offs are projected to fall but remain above historical averages, the report says.

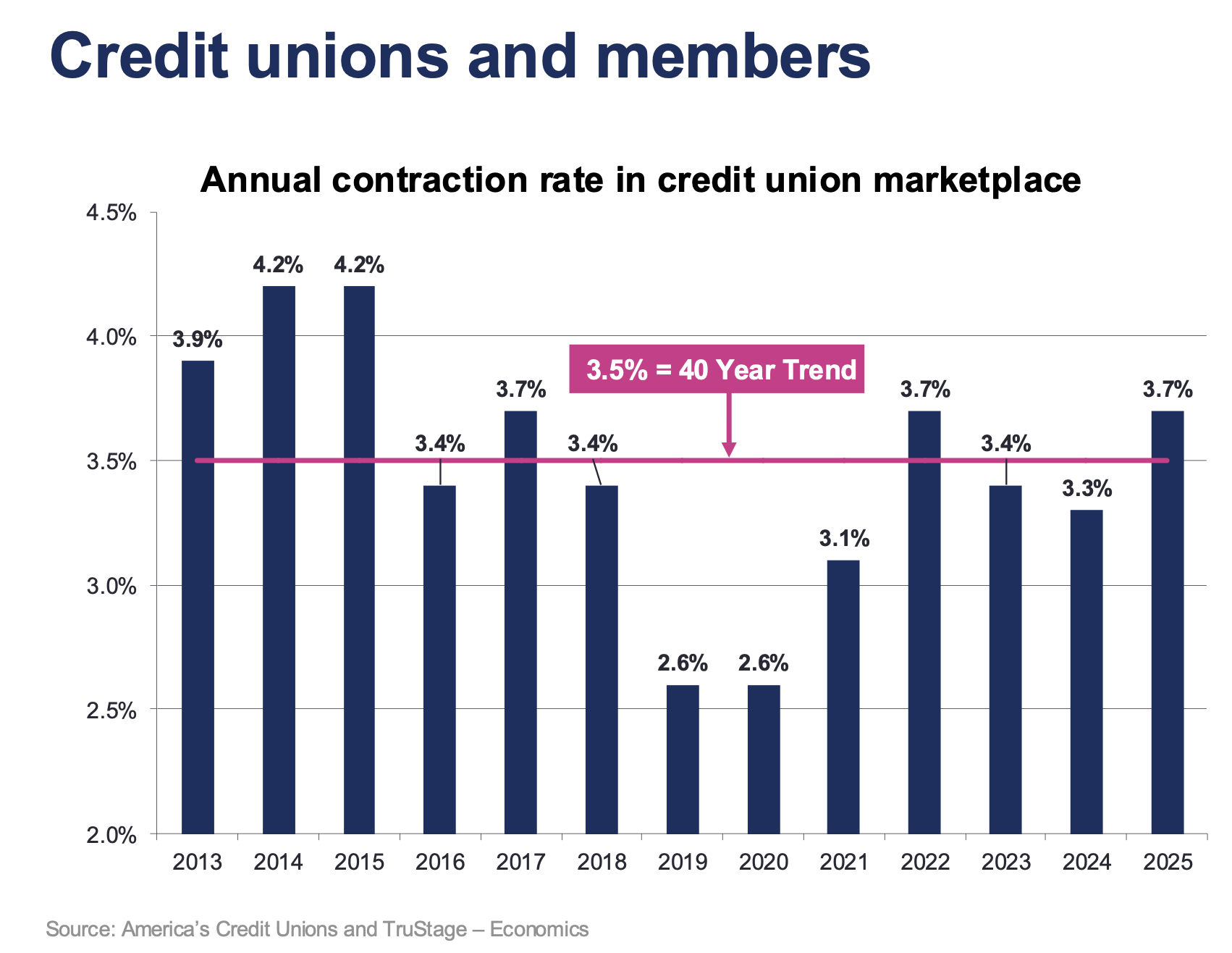

Credit Unions and Members

Industry consolidation accelerated, with the number of credit unions falling 3.7% in 2025 to an estimated 4,419 institutions.

TruStage expects 170 to 175 mergers in 2026, largely driven by the need for scale to fund digital banking, artificial intelligence, instant payments and cybersecurity investments.

“If we forecast out a little further, according to the laws of exponential decay, there will only be 2,167 credit unions in 20 years, half as many as there are today,” the report states. “Fortunately, credit union assets follow an average annual exponential growth rate of 7%. This means the time that it takes for credit union assets to double (currently $2.420 trillion) is only 10 years. So, 20 years from now in the year 2045 credit union assets could be 3.9 times bigger than today, or $9.4 trillion.”