LAWRENCEVILLE, Ga.–With some market analysts forecasting sharp price increases on vehicles from President Trump’s new tariffs, Black Book is offering some specific ways it believes auto manufacturers may respond to mute those increases.

In a new report the company is providing an overview of potential outcomes for sales and transaction prices at the industry level, along with commentary on nuanced dynamics due to these import tariffs.

New Vehicle Average Transaction Price (ATP) Impact Overview

To forecast the impact to ATP at the industry level, Black Book said it used the following assumptions:

OEMs Will Seek to Maintain Current Relative Pricing in the Showroom

“Transaction prices are established and continually refined by supply and demand dynamics and market factors including consumer preferences, macroeconomic factors (gas prices) and, more recently, supply chain dynamics,” Black Book said. “A key component of OEM pricing strategy is relative positioning versus other vehicles in a brand showroom and competitive set. Simply put, a Honda Civic (made in Canada and subject to the 25% tariff) cannot coexist at a higher price alongside the Honda Accord (made in the US). Black Book believes automakers will spread out the incremental cost of tariffed vehicles across their entire showroom to retain relative vehicle transaction prices.”

Automakers Will Absorb as Much of The Tariff Impact as Possible

Black Book noted the automotive industry requires massive investment in vehicle development and fixed operations that take years to amortize over the lifecycle of a vehicle.

“Keeping production steady is a critical part of the financial calculation driving long term profitability and Black Book believes automakers will sacrifice ~80% of existing margin on post-tariff production to avoid or minimize long term losses towards amortization of fixed costs,” the company said.

Shift in 2025 Market Share by Sector and Segment

Black Book said its analysis applied a modest adjustment in the market share of sector and segment categories in response to the launch of tariffs and the mix of import versus domestically produced vehicles in each group.

“Black Book expects the market share of domestically produced pickup trucks to increase at the expense of Premium passenger cars (which are predominantly imported and higher priced) and Mainstream passenger cars (which have a heavy mix of imported vehicles and rental fleet sales),” it said.

Margin and Import Mix Vary Across Sectors and Segments

As part of the transaction price impact assessment, Black Book said it considered the mix of vehicles in each sector and segment that are imported versus. domestically assembled. The company further said it assumes overall profit margin is higher for Premium brands versus Mainstream brands and higher for Truck/Utilities vs. Passenger Car segments.

No Consideration of Cross-Elasticity Impacts for Non-Affected Vehicles

According to Black Book, it has not considered unique shifts in vehicle market share for non-affected vehicles versus vehicles subjected to the 25% tariff.

“This approach extends to automakers who are more insulated from tariff impact due to heavy domestic production (Ford) compared to automakers who are heavily reliant on import vehicles (Volkswagen Group of America),” it said.

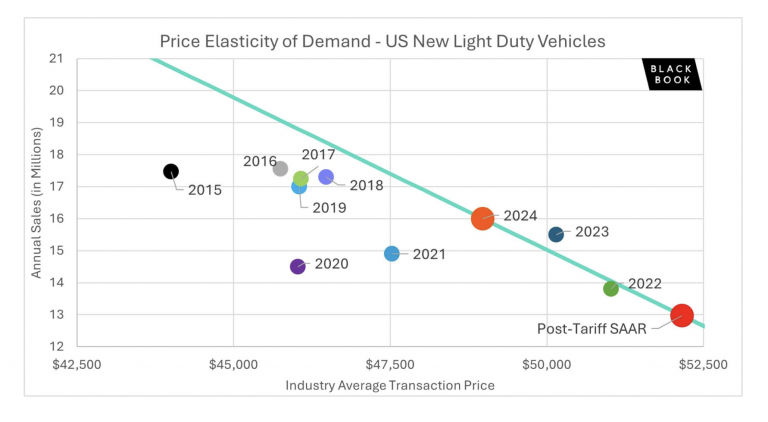

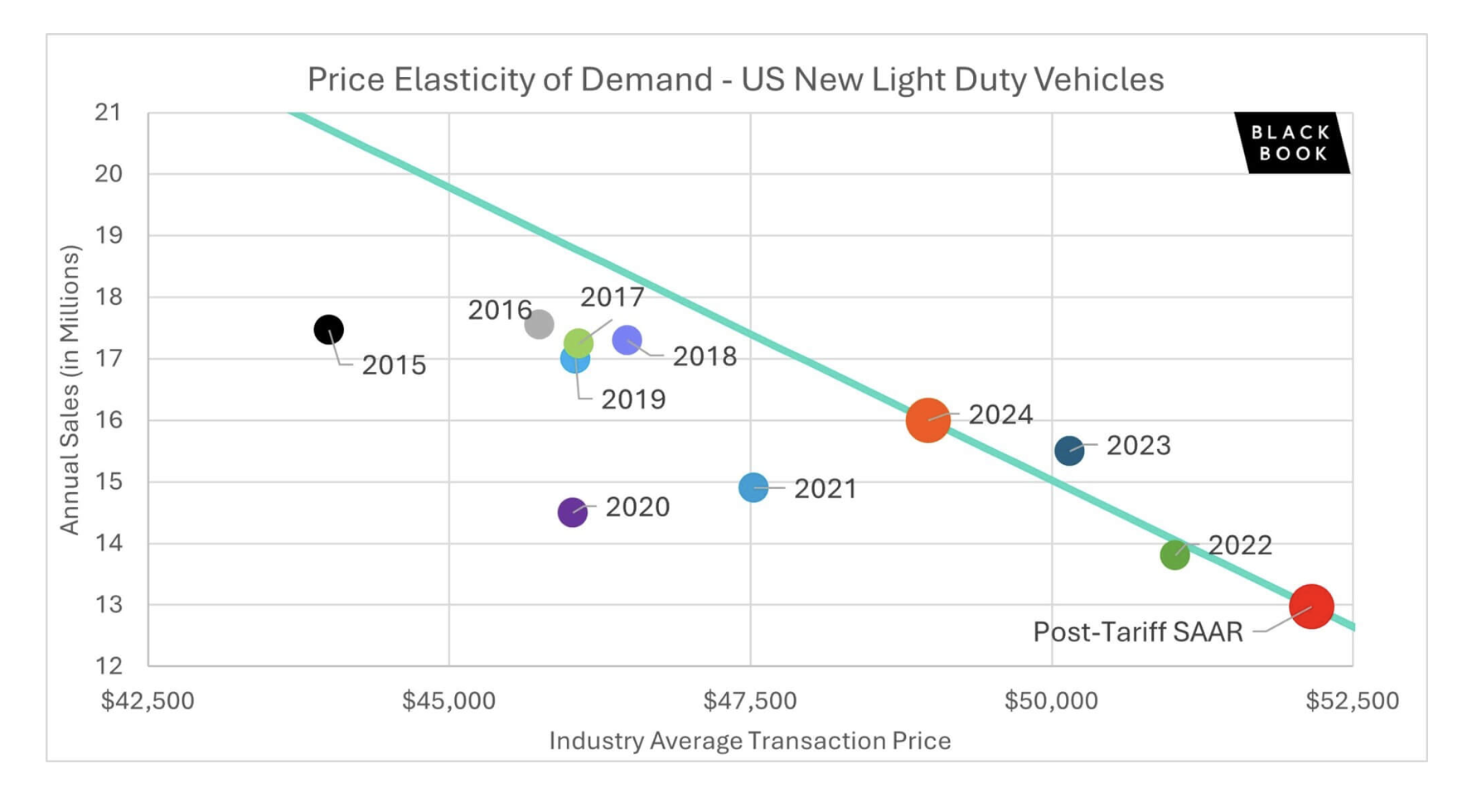

US Light Vehicle Price Elasticity of Demand

Black Book noted it established an elasticity curve based on 2021-2024 annual sales and pricing performance (adjusted for inflation). Below is a graphic that shows this elasticity benchmarked against 2024 results. Sales results going back to 2015 are also provided but were not included in the elasticity calculation given changes in recent market conditions.

The Forecast for ATP

Considering all factors, Black Book said it expects ATP to increase to $52,250, a 5% rise from the 2024 year-end figure of $49,750. Additional scenarios are also highlighted below alongside storylines that Black Book expects will develop as the full impact of tariffs emerge.

Black Book said it expects an ATP of $52,250 will result in a 12.9 million unit Seasonally Adjusted Annual Rate (SAAR) of sales.

“This forecast aligns with the sales and pricing performance of 2022 at the height of the supply chain crisis,” the company said. “However, during that year the significant rise in incomes went into the pockets of dealers and automakers. In a post-tariff environment, the incremental revenues will go to the federal government at the expense of automakers.

“For context, vehicle sales in the US fell sharply during the Great Recession, dropping to 13.2 million in 2008 and 10.4 million in 2009,” Black Book continued. “Production was also curtailed significantly due to the bankruptcies of GM and Fiat Chrysler Automobiles (now Stellantis). Sales began to recover but were weak in 2010 (11.6M) and 2011 (12.8M). They steadily increased to over 17 million in 2015 and remained strong for the rest of the decade.

Sales to Fall

“In January 2025, prior to the announcement of tariffs, Black Book forecasted 16.4 million sales for the full calendar year,” Black Book stated. “If tariffs are…active through the remainder of the year, Black Book expects sales to fall to 13.7 million cars and trucks in 2025, a roughly 17% overall annual decrease.

For the full report, go here: