NEW YORK–Household debt in the United States continued to climb in the third quarter of 2025, reaching a record $18.59 trillion, according to the Federal Reserve Bank of New York’s latest Household Debt and Credit Report.

The data, which is drawn from the New York Fed’s Consumer Credit Panel, found a $197 billion increase from the previous quarter, with mortgage balances accounting for the lion’s share of the growth.

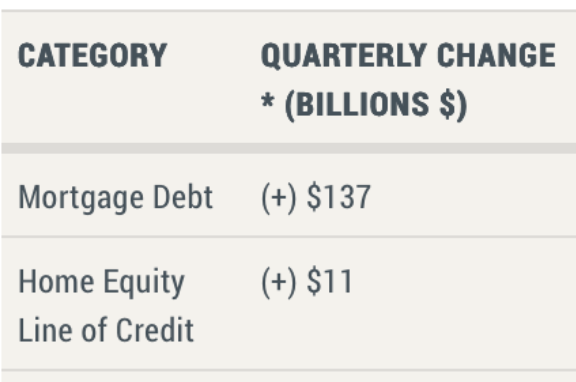

Mortgage balances rose by $137 billion to $13.07 trillion, while new mortgage originations ticked up to $512 billion for the quarter, the New York Fed reported.

“Household debt balances are growing at a moderate pace, with delinquency rates stabilizing,” Donghoon Lee, economic research advisor at the New York Fed, said in a statement. “The relatively low mortgage delinquency rates reflect the housing market’s resilience, driven by ample home equity and tight underwriting standards.”

What the Data Show

The New York Fed report reveals:

- Credit card balances also hit a new high, climbing $24 billion to $1.23 trillion

- Auto loan balances held steady at $1.66 trillion

- Home equity line of credit (HELOC) balances increased by $11 billion to $422 billion

- Student loan balances rose $15 billion to $1.65 trillion

- Non-housing balances overall grew by 1% from the previous quarter

Delinquency Details

The New York Fed data indicate delinquency rates remained elevated but largely stable, with 4.5% of outstanding debt in some stage of delinquency—levels not seen since early 2020, but still well below the 11% peak during the 2009 financial crisis.

Notably, the New York Fed noted that transitions into serious delinquency (90 days or more past due) increased for most debt types, but mortgages saw a slight decrease, underscoring the sector’s relative strength.

The report found, however, that younger borrowers are feeling more pressure, as the rate of serious delinquency among those aged 18 to 29 doubled from a year earlier, driven in part by missed student loan payments.

Student loan delinquencies spiked to 9.4% in Q3, up from 7.8% at the start of the year, as previously paused federal loan payments began appearing on credit reports.