BOSTON — Higher credit card interest rates significantly reduce consumer spending, with the largest effects felt by financially constrained households, according to new research from the Federal Reserve Bank of Boston.

In a report authored by Boston Fed economists Falk Bräuning and Joanna Stavins, researchers found that a one percentage point increase in credit card annual percentage rates leads to an average 8.7% decline in card spending in the following month.

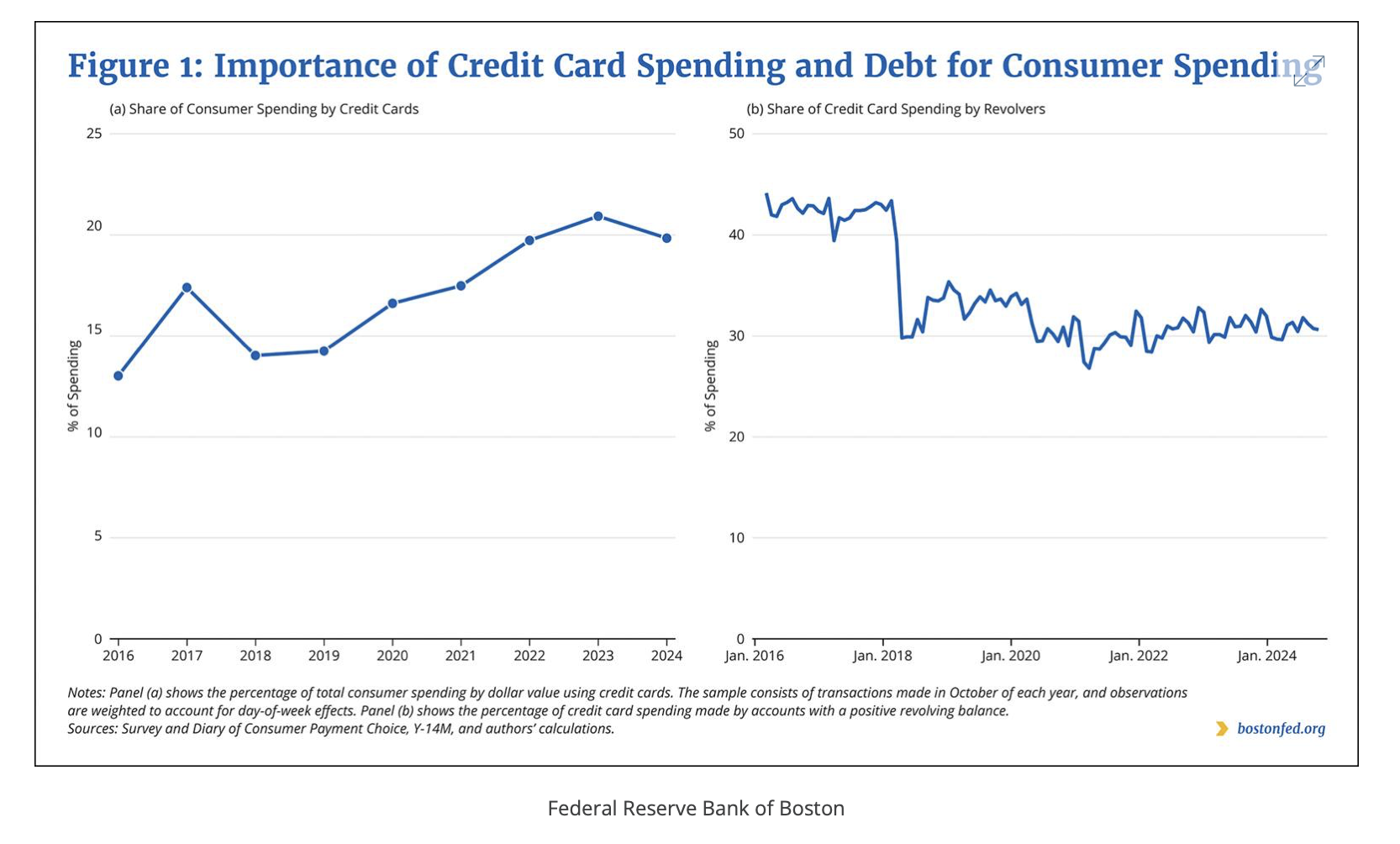

The findings highlight an important channel through which monetary policy affects the broader economy, as credit cards account for a substantial share of U.S. consumer spending, the Boston Fed said.

The report also found that higher borrowing costs lead consumers to reduce debt. A 1 percentage point increase in credit card interest rates results in about a 4% decline in revolving balances, according to the researchers.

Varied Impact

However, the impact varies significantly across different types of borrowers. Consumers who carry balances from month to month—known as “revolvers”—cut spending by about 15% following a rate increase, nearly double the overall average effect, the Boston Fed said. By contrast, consumers who pay off their balances each month show little change in spending behavior.

The response also differs by credit profile. According to the report, consumers with lower credit scores reduce spending by roughly 18% when interest rates rise, while higher-credit-score borrowers tend to maintain spending levels but instead pay down debt.

Researchers said these differences reflect varying levels of financial flexibility. Lower-credit-score households, which often have fewer savings and limited access to alternative credit, are more likely to cut spending when borrowing costs increase. Higher-credit-score consumers are better positioned to manage higher rates by adjusting their balance sheets, the Boston Fed said.

The analysis is based on supervisory data covering nearly 80% of U.S. credit card accounts from 2016 through 2025, including detailed monthly information on spending, balances, interest rates and borrower characteristics.

Disproportionate Effect

The researchers noted that because the strongest responses come from lower-credit-score borrowers and those carrying balances, monetary policy tightening may disproportionately affect households that are already financially constrained.

The report also cautioned that its findings focus specifically on credit card spending and do not fully capture whether consumers substitute other forms of credit or payment, meaning the overall effect on total consumer spending may be smaller, according to the Boston Fed.