CHARLOTTE, N.C.–Should credit unions refocus the efforts to help sole female mortgage applicants get approved for loans? A new study shas found sole female applicants are 29.8% more likely to be denied a mortgage than sole males, according to a new study from Lending Tree.

Lending Tree’s study found:

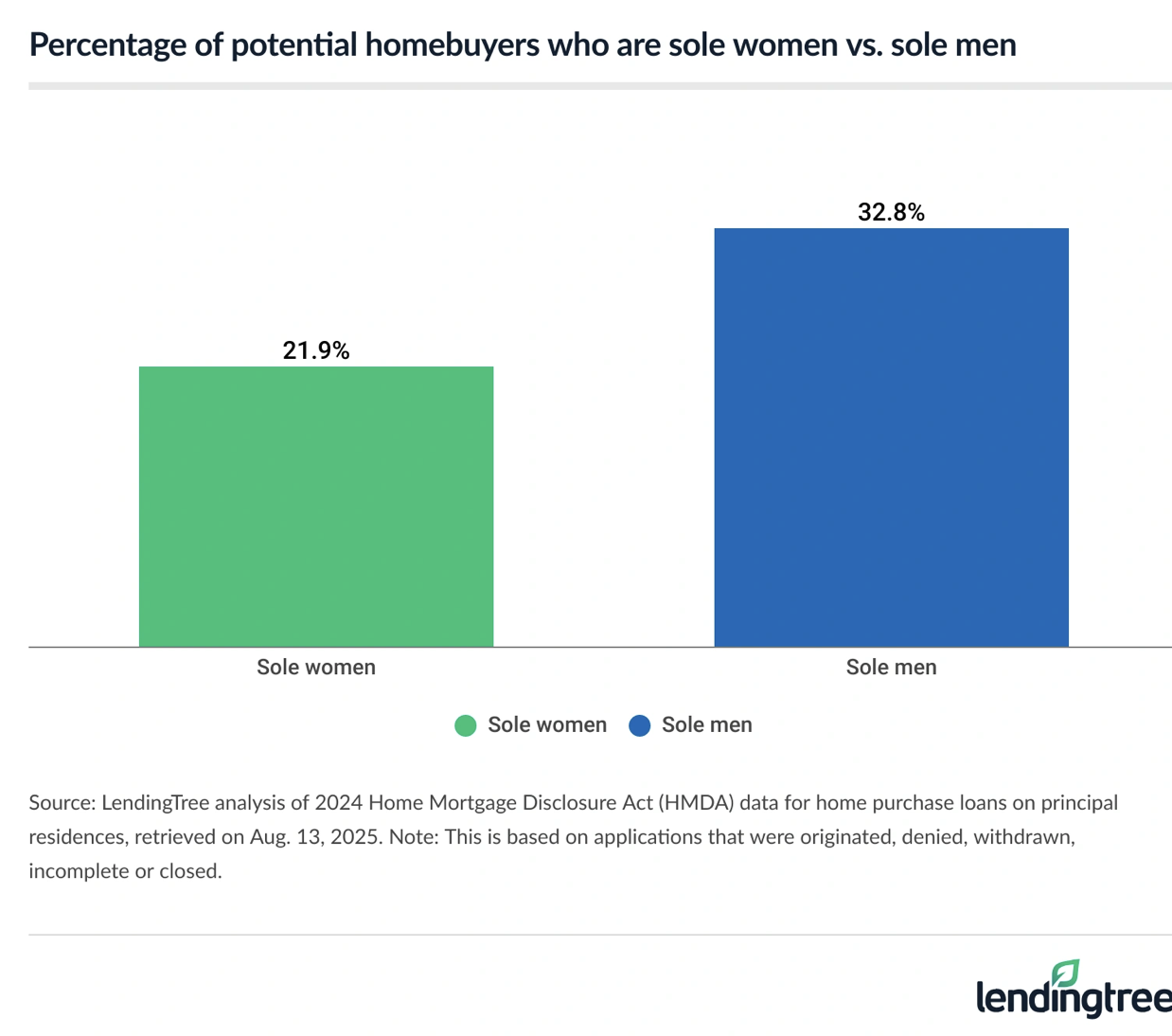

- Sole women made up 21.9% of potential homebuyers in 2024, compared with 32.8% for sole men — 1.5 men for every woman.

- Sole female applicants face higher denial rates but originate conventional 30-year, fixed-rate mortgages for smaller amounts, resulting in lower monthly payments amid slightly better average interest rates.

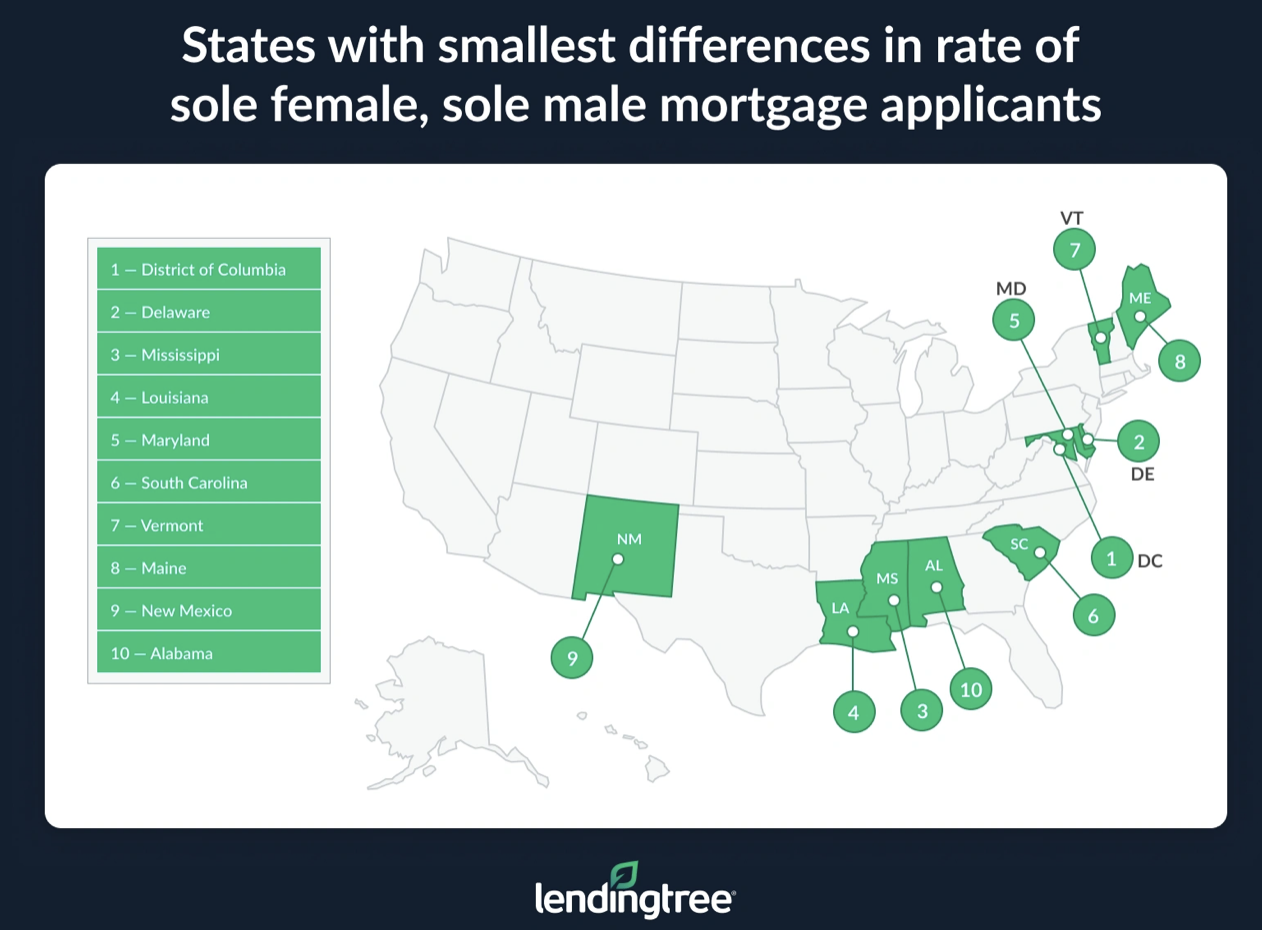

- The District of Columbia is the only state/region where the percentage of sole female applicants is higher than that among sole males (32.0% versus 29.2%). Utah has the largest gap (125.4%), with over twice as many sole men applying as sole women (30.2% versus 13.4%). Alaska (101.1% more sole male applicants than sole females) and North Dakota (100.0% more) follow.

- Sole female applicants are 29.8% more likely to be denied a mortgage than sole males (15.7% versus 12.1%). The largest disparities are in Louisiana (29.0% versus 18.1%), Mississippi (29.0% versus 19.8%) and Alabama (21.9% versus 14.8%).

- Denial rates among sole men exceed those among sole women in six states — D.C., Alaska, Hawaii, Vermont, Maine and Rhode Island.

- Sole men who originate mortgages pay more monthly than sole women in every state. Sole men originate conventional 30-year, fixed-rate mortgages with higher average loan amounts in every state. In Vermont, Iowa and Wyoming, the monthly payment differences are under $100. The largest gaps are in Hawaii ($649), California ($640) and Washington ($578).

- In 2024, sole women originated $173.3 billion in mortgage debt, while sole men originated a much more significant $328.7 billion. In total, sole women originated 600,817 loans, while men originated 949,477. (This is across all primary home purchases in 2024, not just those with conventional 30-year, fixed-rate mortgages.)

- Sole women less likely to be potential homebuyers. Sole female mortgage applicants made up 21.9% of potential homebuyers in 2024, while sole men accounted for 32.8%. That means there were 1.5 sole male applicants for every sole female applicant.

- Overall, sole female applicants face higher denial rates at 15.7%, compared with 12.1% among sole male applicants. Looking at originated conventional 30-year, fixed-rate mortgages, women take out smaller amounts (averaging $299,134, versus $356,550), resulting in lower monthly payments amid slightly better average interest rates.

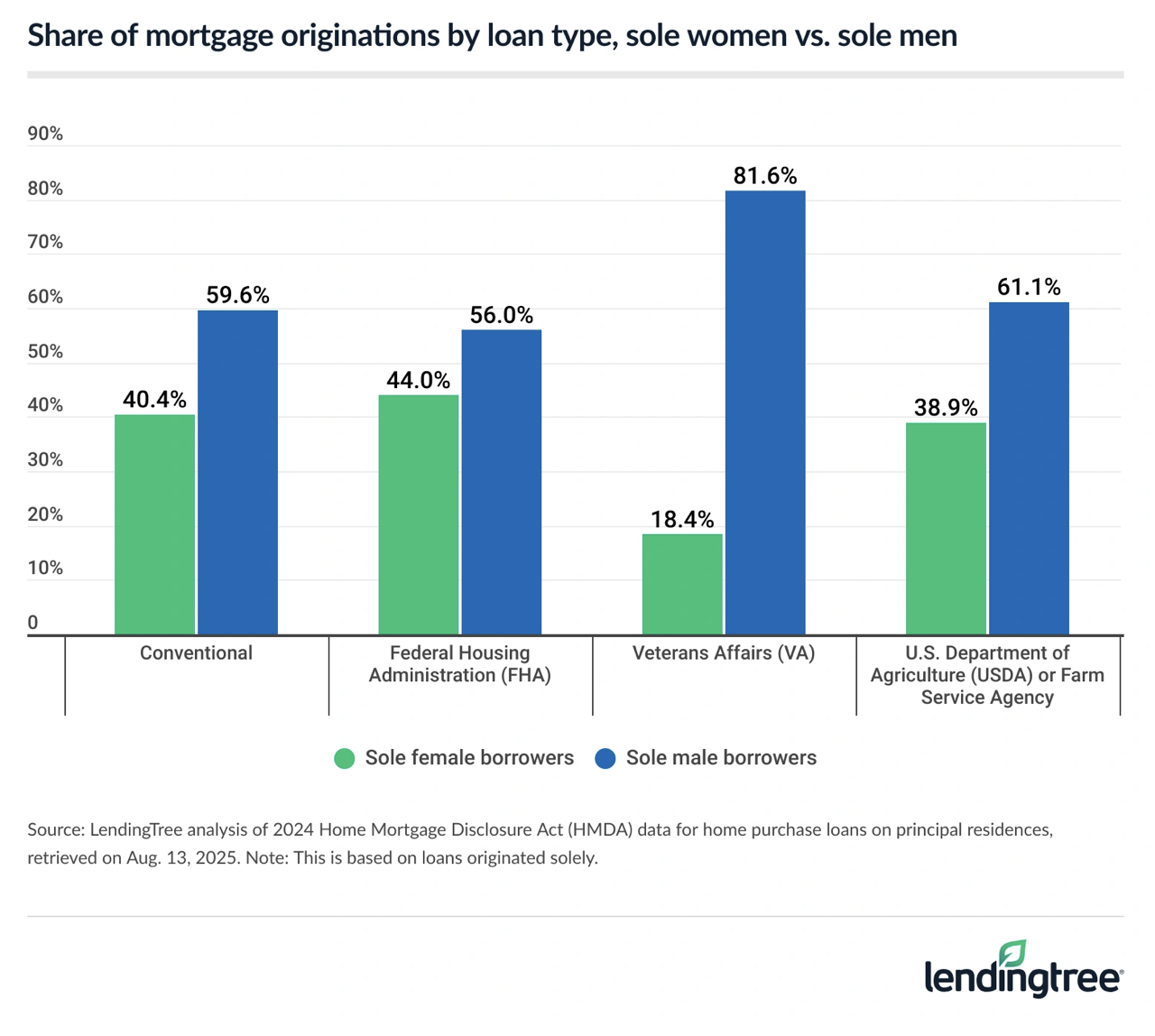

- By loan type originations, sole male applicants dominate across the board. Among just sole applicants, men originate a significant 81.6% of Veterans Affairs (VA) loans, compared with 18.4% among sole women.

The full Lending Tree study can be found here.