NEW YORK — Americans’ lack of emergency savings has been widely discussed in credit union circles and across the country in recent years, but a new Bankrate survey finds the overwhelming majority of households made little progress over the past year.

Eight in 10 Americans did not increase their emergency savings in 2025, according to Bankrate’s annual Emergency Savings Report, leaving most in no better position to handle a job loss, medical issue or other sudden financial shock. Those who failed to save were also more likely to report declining household earnings since the start of the year, Bankrate reported.

The survey, conducted in October by Bankrate with polling partners SSRS and YouGov Plc, has tracked U.S. adults’ debt and emergency savings since 2011. According to Bankrate, the latest responses highlight how persistent economic headwinds — high inflation, rising costs and a cooling labor market — continue to strain household budgets and impede Americans’ ability to prepare for unexpected expenses.

What Survey Found

Bankrate found that 32% of U.S. adults have less emergency savings now than at the start of 2025, while 31% have the same amount. Nineteen percent increased their savings, and 18% had no savings at the start of the year and still have none today.

Those who managed to grow their emergency savings were nearly four times more likely to report increased household earnings over the past year (47% vs. 13%). Conversely, those whose savings declined were four times more likely to say their income fell, according to Bankrate.

Spending Pressures Rise, Especially on Basic Necessities

More than half of all households increased spending on basic necessities in the past year, the survey found. Those with decreased emergency savings (69%) were more likely to report higher spending on essentials than those whose savings increased (59%). But people who increased their savings were more likely to spend more on big-ticket purchases like a car or house (25% vs. 14%), Bankrate reported.

Since 1976, Bankrate noted it has published personal finance data tracking consumer experiences with financial products. The latest survey again found disparities in who was able to save: men, younger adults, higher earners, those with college degrees and non-parents were more likely to have grown their emergency funds.

Among the related findings:

- 21% of men increased their savings, compared with 16% of women.

- 28% of Gen Z respondents increased their savings, compared with 19% of Millennials, 14% of Gen X and 15% of Baby Boomers.

- Among those with a four-year degree, 26% grew their savings, compared with 13% of those who never attended college.

- 21% of non-parents increased savings vs. 16% of parents.

- Among households earning $100,000 or more, 27% grew their savings, compared with 11% of those earning under $50,000 — who were also most likely to have no emergency savings.

Income Growth, Not Spending Cuts, Is the Biggest Factor

Bankrate said it found those who increased their emergency savings were nearly four times more likely to report higher household earnings over the past year (47% vs. 13%), while those whose savings fell were four times more likely to report reduced earnings (44% vs. 11%). Spending patterns, meanwhile, showed weaker correlation.

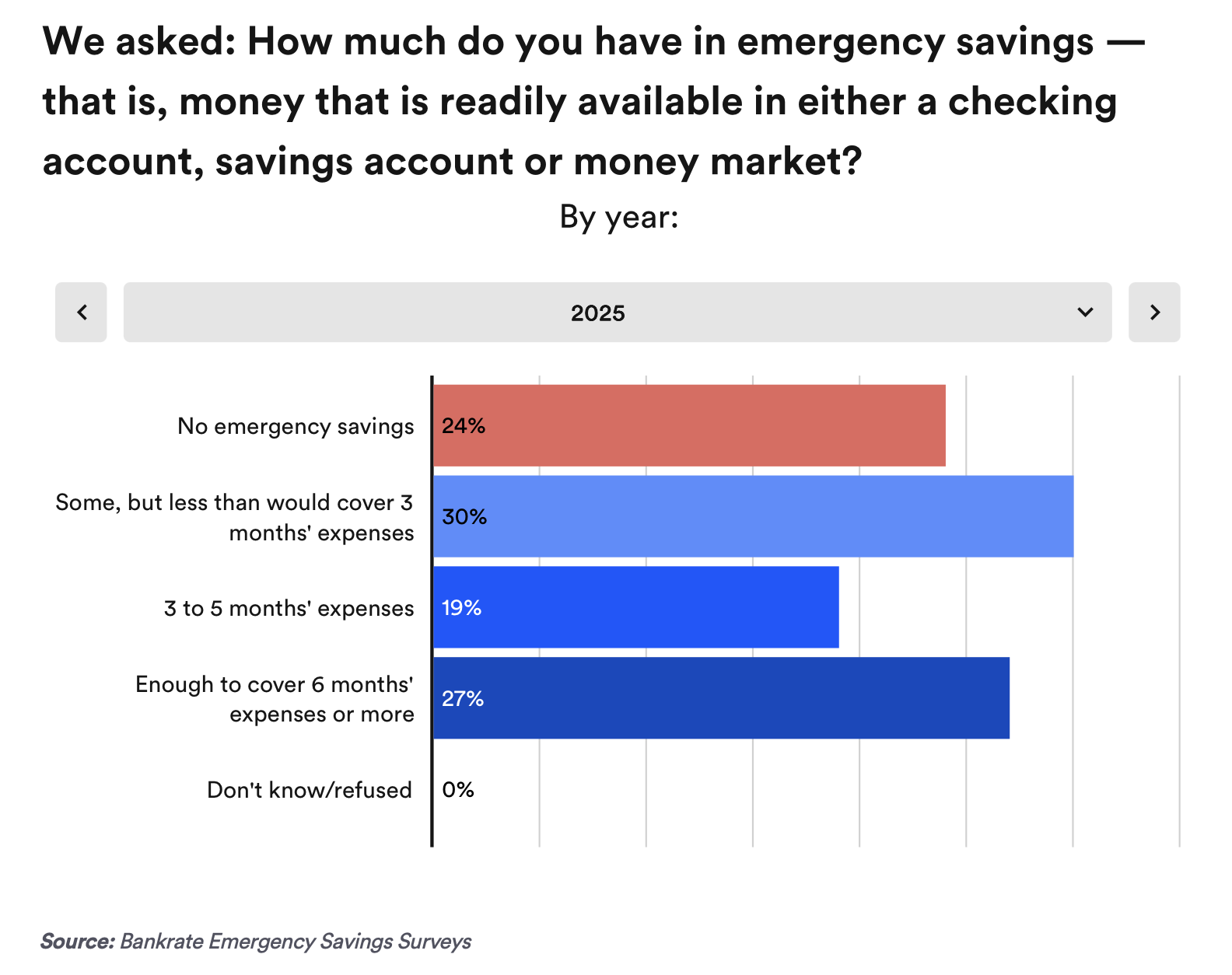

Nearly a Quarter of Americans Have No Emergency Savings

As the CU Daily has reported, experts typically recommend saving three to six months of expenses, yet only 46% of Americans have at least three months’ worth, the survey found. Thirty percent have some savings, but not enough to cover three months. Nineteen percent could cover three to five months, while 27% could cover six months. Nearly one in four Americans (24%) have no emergency savings, according to Bankrate.

Gen Z adults (ages 18–28) were most likely to lack meaningful savings.

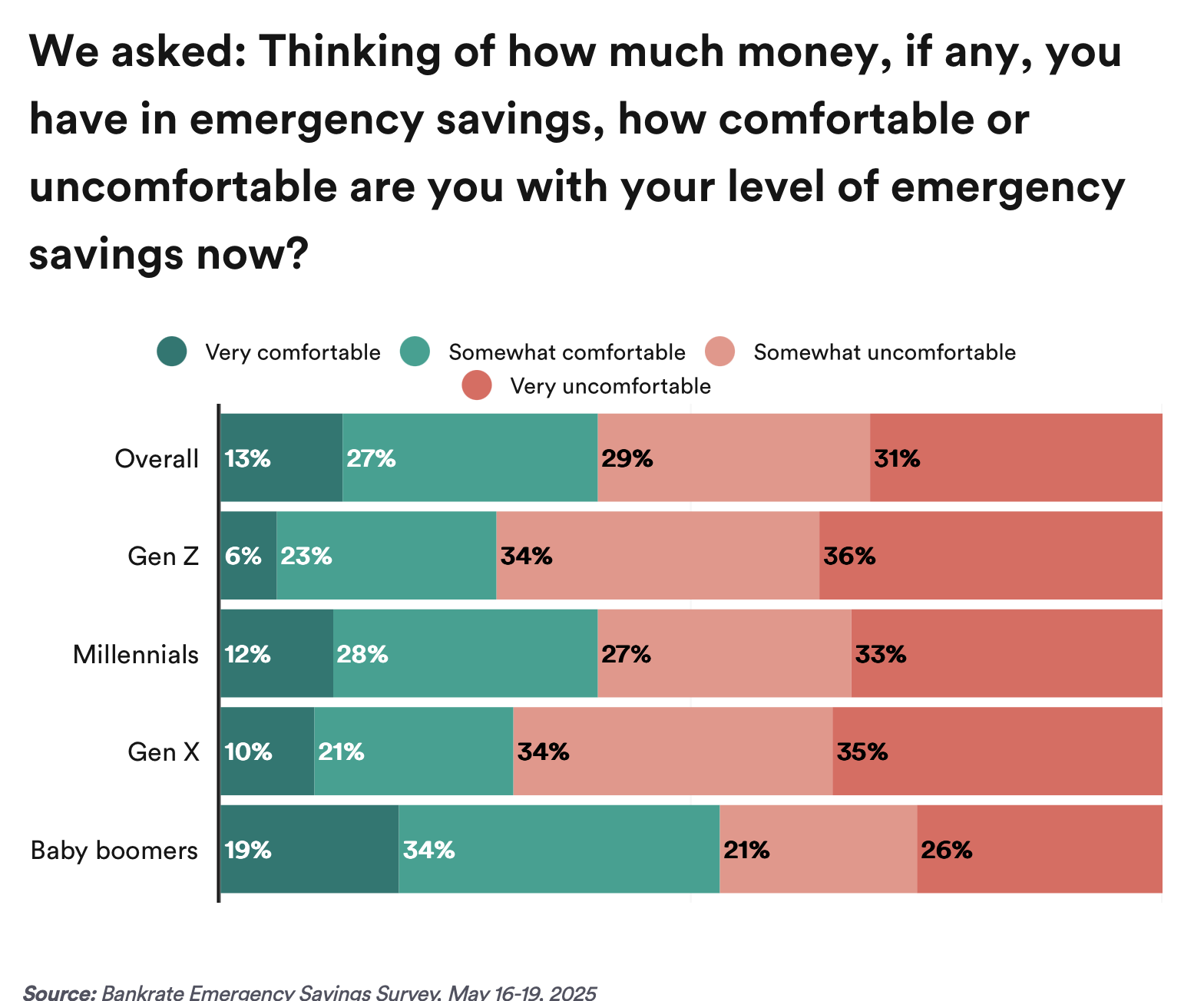

Most Americans Are Uncomfortable With Their Savings Level

Sixty percent of Americans are uncomfortable with their level of emergency savings — 31% very uncomfortable and 29% somewhat uncomfortable. Only 40% feel comfortable, including 27% who are somewhat comfortable and 13% who are very comfortable, according to the survey.

Among those comfortable with their emergency savings, 80% could cover at least three months of expenses, and 51% could cover six months. Among those uncomfortable with their savings, 76% could not cover three months, including 36% with no savings at all.

Gen Z and Gen X adults are least likely to feel comfortable with their savings (29% and 31%, respectively), compared with 40% of millennials and 52% of baby boomers.

The Savings Gap

Eighty-five percent of Americans say they would need at least three months of expenses saved to feel comfortable, but only 46% have that much. Sixty-three percent told Bankrate they need at least six months of savings, but only 27% have it.

Nearly one-third of Gen Z respondents say they need three to five months saved to feel comfortable, and half say they need at least six months. Sixty-one percent of millennials, 66% of Gen X and 70% of boomers say they would need six months saved, the survey found.

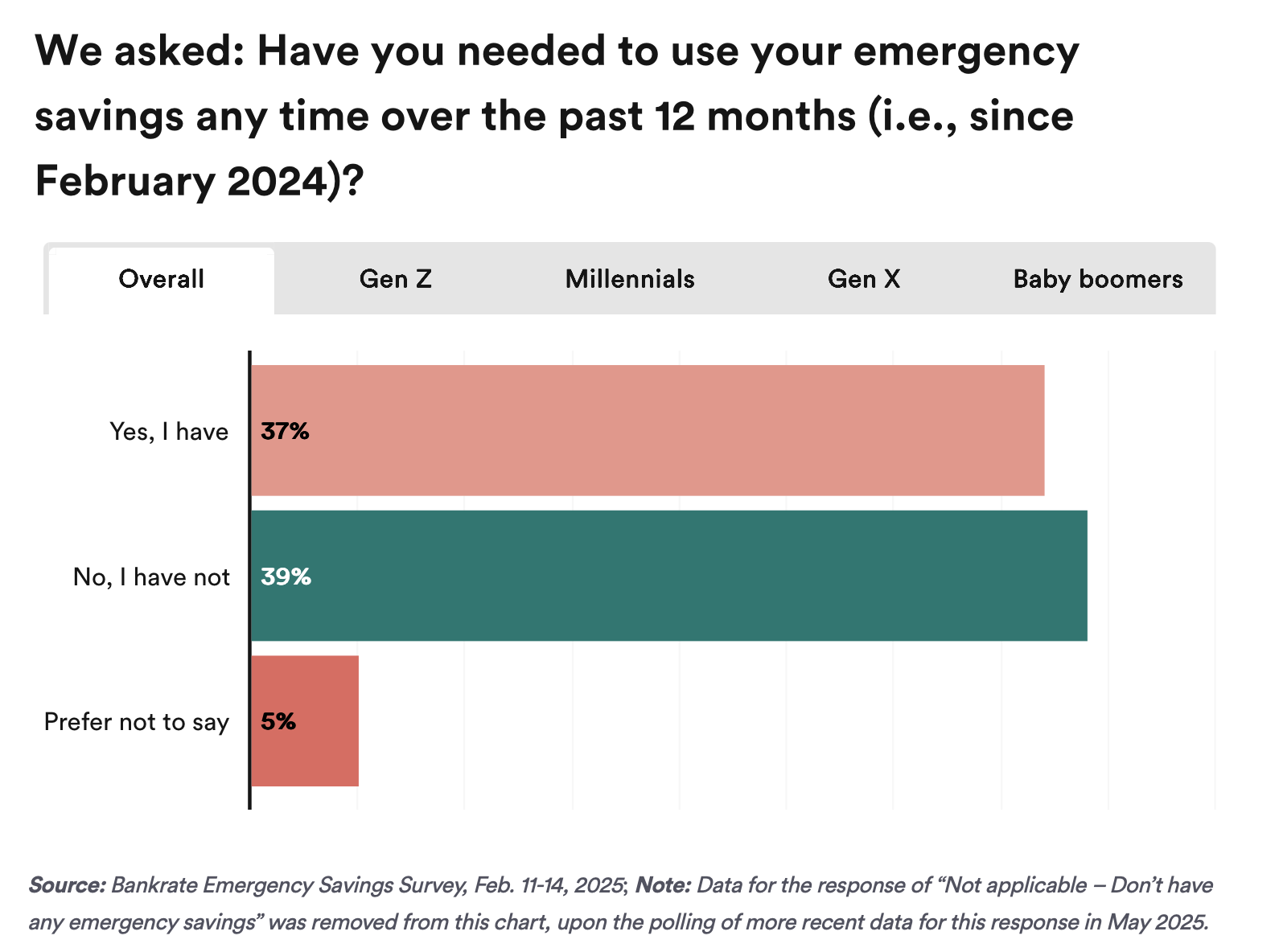

Millennials and Parents Most Likely to Tap Emergency Funds

Among the findings:

- More than one in three Americans (37%) tapped their emergency savings in the past year; 39% did not, as of February 2025.

- Millennials were most likely to have done so (42%), followed by Gen X (38%), Gen Z (34%) and baby boomers (33%).

- More than one in four adults (26%) who withdrew money took between $1,000 and $2,499 — the most common amount. Twenty-two percent withdrew $500 to $999, and 18% withdrew less than $500.

Most Withdrawals Were for Essential Expenses

Among the findings:

- 80% of those who dipped into emergency savings used the funds for essential needs.

- 51%paid for an unplanned emergency like a medical bill or car repair

- 38% covered monthly bills and 32% paid for day-to-day necessities.

- Others withdrew money to help family or friends (22%) or to pay down debt (21%).

- Only 19% withdrew funds for non-essential reasons such as vacations (9%), discretionary shopping (10%) or entertainment (7%).

More Credit Card Debt Than Savings

Bankrate reported that from 2011 through 2022, fewer than 30% of Americans had more credit card debt than emergency savings. But in 2023, amid high inflation, that figure jumped to 36% and remained there for two years, the company said.

In 2025, the percentage fell slightly to 33% but remains above pre-2023 levels, the survey found. Meanwhile, 53% have more emergency savings than credit card debt — a share that has hovered between 51% and 55% since 2021. Thirteen percent have neither credit card debt nor emergency savings.

Many Trying to Save and Pay Down Debt Simultaneously

Bankrate said its survey found paying down debt and building savings are both priorities, but only 35% of U.S. adults are doing both at once. Twenty-eight percent are focused solely on building emergency savings, and 24% are focused only on paying down debt.

Fewer Americans Would Use Savings for an Emergency Expense

Among the findings:

- 41% of Americans would use savings to pay a $1,000 emergency expense — down from 44% a year earlier and the lowest figure since 2021.

- 25% would use a credit card and pay it off over time, up from 21% a year ago.

- Another 13% would reduce spending, 13% would borrow from friends or family, 5% would take out a personal loan and 4% would find another solution.

Inflation Continues to Erode Americans’ Ability to Save

Bankrate said it found that although inflation has slowed, more Americans say economic conditions are hurting their ability to save. Nearly three in four (73%) say inflation, high interest rates or changes in income or employment have reduced their emergency savings contributions — up from 68% in 2024.

For the full survey, go here.