SACRAMENTO, Calif. — A Sacramento-area credit union member who first raised concerns in a letter to the the Sacramento Bee is now pressing state lawmakers to intervene in the proposed combination of Sacramento-based SAFE Credit Union and Seattle-based Boeing Employees Credit Union (BECU), saying recent meetings with legislators have heightened scrutiny of the deal.

Scott J. Rose, who said he is a longtime SAFE member, shared with the CU Daily that he has met with representatives of multiple California lawmakers to argue that the proposed transaction would harm the Sacramento region and should be blocked by the California Department of Financial Protection and Innovation (DFPI).

In a statement to the daily, Rose said he met March 24 with a field representative for Assemblywoman Maggy Krell, who he said, “appeared to understand that the SAFE-BECU transaction would have major adverse repercussions for our region” and described the timeline for potential approval as urgent. He also said the office of Assemblywoman Stephanie Nguyen requested additional information, including materials from a presentation he prepared outlining his objections.

A Need to Work Together

Rose shared with the CU Daily letters he wrote to both representatives.

Rose said legislative coordination will be critical, noting that “the three Sacramento legislators would need to work together” to influence the outcome.

The outreach follows Rose’s earlier letter, reported by CU Daily, in which he questioned who benefits from the proposed deal and argued SAFE members would not be compensated for their ownership stake.

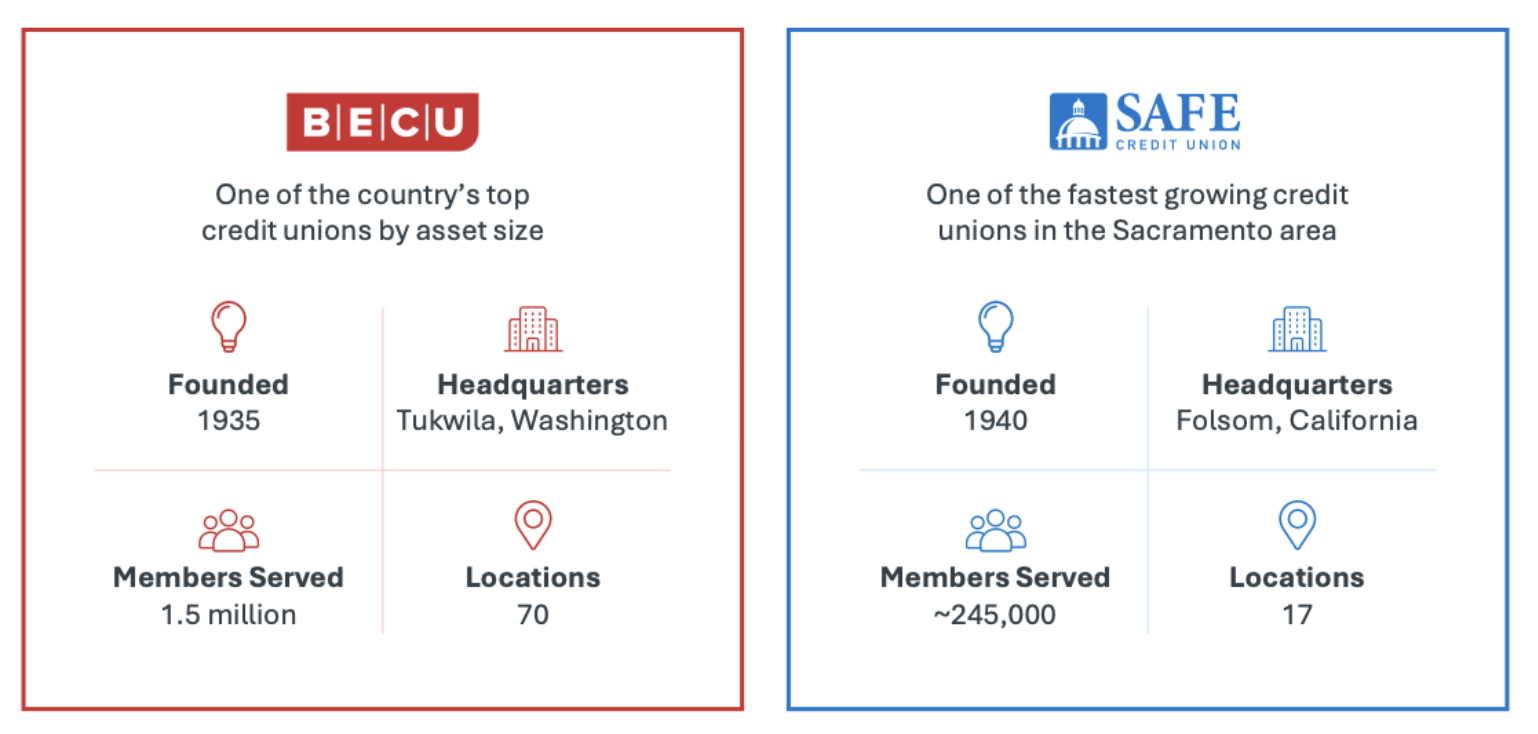

In materials shared with lawmakers, Rose contends the transaction would result in the termination of SAFE’s charter and the transfer of approximately $4.31 billion in assets — including about $345 million in member equity — to BECU without direct compensation to SAFE’s 245,000 members.

SAFE and BECU announced in November 2025 that they plan to combine, pending regulatory and member approval. The combined entity would have roughly 1.8 million members and more than $33 billion in assets, making it one of the largest credit unions in the United States.

‘Not a Merger of Equals’

Rose argues the transaction is not a merger of equals, noting BECU’s significantly larger size — about $29 billion in assets and 1.5 million members — and its lack of historical ties to the Sacramento region. He also claims BECU would not be required to make a capital investment to acquire SAFE, characterizing the deal as a “gift” of member-owned resources.

The Concerns Raised

Among the concerns raised in Rose’s presentation and fact sheet:

- Loss of California regulatory oversight, with authority shifting to Washington state regulators

- Potential layoffs among SAFE’s roughly 700 local employees

- Reduction or loss of local philanthropic contributions, which totaled more than $437,000 in 2024

- Transfer of governance and decision-making to an out-of-state board

‘Secret’ Discussions Alleged

Rose also alleges the SAFE board conducted merger discussions in secrecy and may have violated fiduciary duties to members, claims that have not been independently verified.

Supporters of the transaction, according to materials cited by Rose, have pointed to potential benefits including enhanced digital services, improved fraud prevention capabilities, expanded mortgage programs and possible rate advantages for members.

The proposal still requires approval from both SAFE members and the DFPI. Rose has urged lawmakers to press regulators to scrutinize the deal and require greater transparency.

“Without legislative or regulatory intervention Sacramento will lose an irreplaceable regional asset,” Rose said in his materials.

CEO’s Statement

As the CU Daily reported earlier, SAFE CU’s president and CEO, Faye Nabhani, has made his case in local media for why the combination should be approved.

One Response

It’s highly unlikely that the legislature will effectively intervene here, and the regulators have no basis not to approve this merger. Mr. Rose needs to mount a member campaign to influence SAFE members to vote against it. Boeing has lost its culture under the new CEO, execs are bailing, they can’t grow, their Board is very highly paid, and their leaders get bonuses based on revenue and profit measures. They have become a for-profit bank and SAFE might as well merge with Wells Fargo. They need this merger to mask their own inefficiency, which means job losses in California will be very high.