SAN JOSE, Calif.–Another proposed credit union merger in which executives will receive more than $2.5 million in payouts—with no net worth distribution to members—and where there has also been an unusually high level of member comment (nearly all negative) can be found in the latest review of CU mergers by the CU Daily.

The payout to management is not unusual among CUs in this, the second of a three-part series on the latest member disclosure forms filed with NCUA. In addition, as the CU Daily reported here, new details from the proposed merger between Minnesota-based Wings Financial Credit Union and Colorado-based Ent Credit Union reveal nearly $10 million in payments is slated to go to executives in that deal.

The first part of this three-part series can be found here.

Below, the country-spanning combination between California-based First Tech FCU and Massachusetts-based DCU to create a $30-billion operation leads the way in the latest reporting.

A Coast-to-Coast Combo, Payouts for Execs, Lots of Comments From Members

Merging Credit Union: First Technology FCU, San Jose, Calif.

Assets: $16.87 billion

Members: 712,057

Year Chartered: 1970

Date of Member Vote: Dec. 8

Acquiring Credit Union: Digital FCU, Marlborough, Mass.

Assets: $12.86 billion

Members: 1,189,016

In one of the largest mergers ever proposed in terms of assets and national reach, First Technology FCU told members a combination with Digital FCU would create an “even brighter future” for the institution.

Benefits of the merger, according to First Technology, include:

- Service and Simplicity: “While First Tech will reach $30 billion in assets serving nearly two-million members, we’ll remain obsessed with making the banking experience simple while delivering personalized experiences.”

- Improved Experiences: “Significant annual reinvestments will be made into research and development aimed at accelerating and simplifying technology, products and digital experiences for members across the globe.”

- Expanded Access: “You’ll have access to an expanded branch network, including 54 branches operating in eight states, extended service hours, best-in-class technologies, access to premier financial products and a dedicated team ready to serve your needs now and into the future.”

- Strength and Stability: “First Tech and DCU are two of the strongest credit unions in the country. If combined, we will continue to have very strong capital and loan-to-deposit ratios, ensuring members’ savings are safe and secure.”

- Positive Community Impact: “Our new organization will become the largest philanthropic leader in the industry, investing over $4 million to improve the lives of others in our communities.”

- Employee Growth: “The expanded organization will allow opportunities for career development with robust employee benefits.”

Payouts to Management

First Technology said in its disclosure to members there will be no payout of net worth to members, but four of its C-suite executives will receive merger-related financial benefits. President and CEO Greg Mitchell will not be among them, the credit union said, as Mitchell is expected to retire on Dec. 31 upon completion of his employment contract.

More than $2.5 million will be distributed to members of First Tech management if the merger is approved, including:

- CFO Marita Domingo. Domingo is to receive up to $1.365 million in merger-related compensation comprised of a possible bonus or severance payment and the accelerated vestment of any long-term incentive plan bonus.

- Chief Experience Officer Jason Heupel, who will receive up to $1.053 million in merger-related compensation comprised of a possible bonus or severance payment and the accelerated vestment of any long-term incentive plan bonus.

- Chief Marketing Officer Brandon Hunt, who will receive up to $484,000 in merger-related compensation comprised of a possible bonus or severance payment and the accelerated vestment of any long-term incentive plan bonus.

- Chief People and Administrative Officer Monique Little, who will receive up to $875,000 in merger-related compensation comprised of a possible bonus or severance payment and the accelerated vestment of any long-term incentive plan bonus.

Financial Performance

First Technology, which has a significant presence in both California and Oregon, had $29.12-million in net income through Q3, with net worth of 10.06%. Digital FCU reported $78.4-million in net income and had net worth of 9.78% as of the same date.

Member Comments

Member comments filed on NCUA’s site include:

- After reading the notice received in the mail, I am leaning towards voting “Do not approve” as there is no real data shown. The information presented does not tell me, as a borrower, how I will be affected and when those changes would be. Will incentives be offered to us such as being able to skip payments for times like spring break or Christmas or will interest rates go down. Will I be able to refinance my loan for better terms. I see there are some who will make some good money off the merger, but what will I gain? Why should I as a borrower vote yes? No one has really showed any data on how members will be affected, good or bad.

- What Asad Aziz said. Why are we doing this, other than to further enrich a few already-millionaires?

- I started saving with First Tech in the mid-80’s when it was Hewlett Packard Credit Union on Hanover Street in Palo Alto, CA and have stayed with it through its transformation to Addison Avenue and then to First Tech. My favorite thing about it is that it has remained local and accessible. I don’t see that continuing after this merger.

- I received the merger election packet for the merger of First Tech and DCU. I have been a member of First Tech for more than 40 years and have been generally happy. I will be voting against this merger for the following reasons.

– The Merger election packet asking for my approval was woefully inadequate and lacking specifics for the business case for this merger.

– The financial section was just a spreadsheet combining the balance sheets of the two companies with no specific goals. This is inadequate to make the financial case for the merger. It seems that DCU has a higher leverage (and therefore risk and return) than FTFCU and the combination will increase risk and return for FTFCU members while lowering it for DCU members. That discussion is however missing.

– The case for ‘bigger is better’ was not made. The majority of credit union members have local banking needs, and the overwhelming majority of members conduct business online, as demonstrated by the redesign of First Tech branches some years ago – so the case for an improved member experience is weak at best. Is there data that shows that a significant number of members face significant inconvenience due to lack of a nationwide branch network?

– What is clear is that several senior executives stand to make around a million dollars each in accelerated vesting and bonuses if this merger goes through.

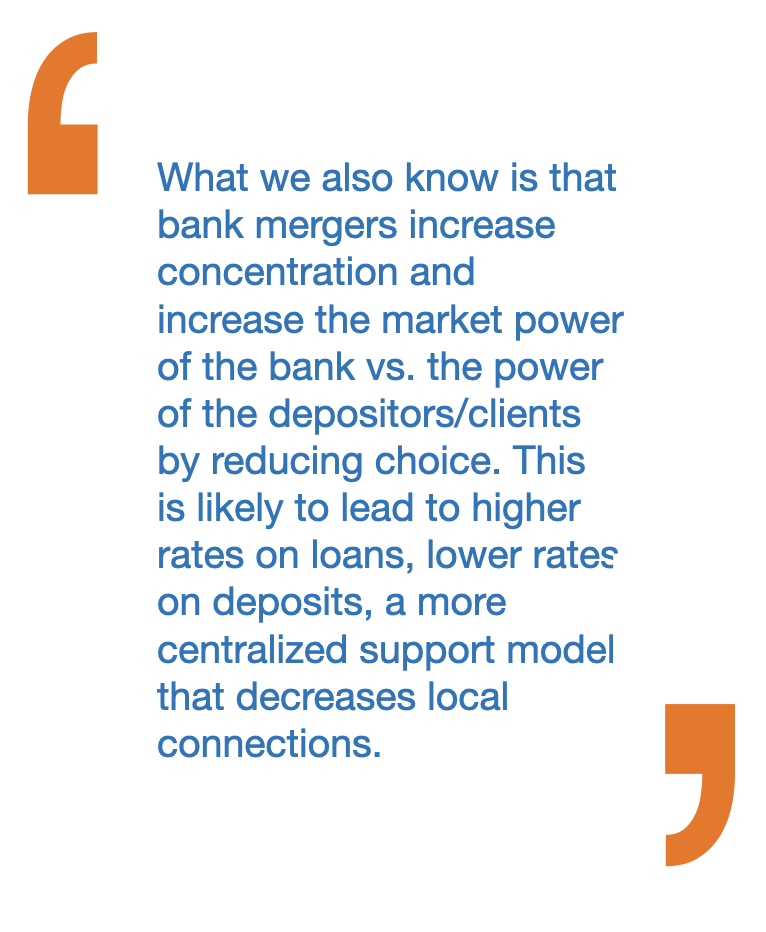

– What we also know is that bank mergers increase concentration and increase the market power of the bank vs. the power of the depositors/clients by reducing choice. This is likely to lead to higher rates on loans, lower rates on deposits, a more centralized support model that decreases local connections. The transition can also be quite disruptive as credit and debit cards, login and access protocols are changed.

Bottom line is that given all the downsides for the members for such a merger, the case has not been made as why this merger will be a net positive for the members. My recommendation is that the merger teams share the detailed information for the business case for this merger on their web sites and point members to that website so that this can be an informed vote.

Currently the business case is, “we’ll remain obsessed with making the banking experience simple”; “significant annual reinvestment…”; “continue to have a strong capital ratio …”; “access to an expanded branch network”. Of these – only the expanded branch network is tangible – but there is not data that suggests that members are asking for it. Might it not be easier if there is demand, to just open a branch or two in the most neglected areas?

Otherwise, the message is – you’ll keep getting what you are getting now.

So why are we doing this? - Why would First Tech members approve this? The shares of the merged credit union are 1:1 exchanges with the shares of the two credit unions and THE VALUES ARE NOT EQUALIZED. All the ratios of value-per-share go down for the First Tech members and up for the Digital members. The REAL STORY is that ALL THE FIRSTTECH C-SUITE PEOPLE (Domingo, Heupel, Hunt, & Little) GET MILLION DOLLAR PAYOUTS. That’s $4,000,000 of equity gone on day one. Of course they are in favor of the merger. The new credit union does not need two sets of CFOs, CEOs, COMs, and CPAOs – so there will be ADDITIONAL golden parachutes for the departing C-suite members, likely the First Tech members as the Digital CEO will be in charge and the name will be Digital Credit Union – why would he fire his team to keep the new guys? THIS IS A BAD DEAL FOR FIRSTTECH MEMBERS but a sweet deal for the 4 C-suite people urging the merger. VOTE NO!

- I agree with the comment above, well at least the one that has not been white washed. I for one am VERY tired of these mergers. I started with Hewlett Packard Credit union and have been through HPFAMILY CU, HPMEDFED, Addison Avenue, Then the merger wit First Tech, only because they wanted the ‘Federal’ Credit union status. I live in the mid-Atlantic states, specifically Wilmington Delaware. Months after that merger, the Credit union office at our ( now Agilent) site was closed up, even though we had about nine hundred employees on site. Now the closest office is up in the Boston Mass area . just a quick seven hour trip.

- This merger does nothing for me, except the continued growth of a portfolio of West coast mortgages That due to the over heated real estate market, and the risk the overtaxed citizens will default. It is simply adding risk! And as noted in the comment above, WHY ? So that the CEO can collect his golden parachute retirement in his contract, and an average cool million drain for the Finance execs who decided this is a good thing! I see NOTHING in the way of strategic planning or benefit for the FTFCU members. We are taking on risk for no given reason.

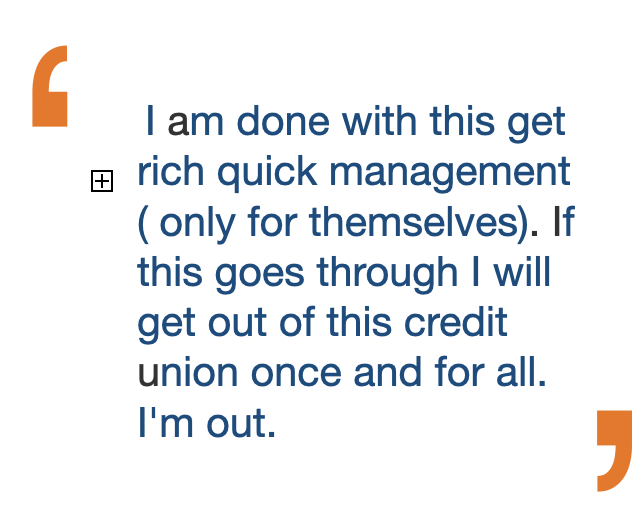

- This is a bad decision from the information given. The communication is very weak. It is obvious you believe you have the votes to push this through. It is sad. I joined the original HP credit union in 1979, and have had several mortgages, lines of credit, HELOC , savings, checking accounts, as well as account for my four children. I am done with this get rich quick management ( only for themselves) . If this goes through I will get out of this Credit Union once and for all. I’m out.

- I have been both a member and an employee of First Tech for more than 45 years. Over that time, I’ve watched our credit union grow from just three offices into a mature organization with the ability to serve members across the globe. Growth has always been part of our story—and this merger is the next chapter. I support it because I believe it delivers real, lasting value for both current and future members and employees. It’s about strengthening our ability to provide exceptional service, expand opportunities, and ensure we remain competitive in a rapidly changing financial landscape. I’ve heard the concerns shared by others, and I respect those perspectives. But from my experience, I see this merger as a way to preserve what makes First Tech special while giving us the scale and resources to do even more for our members, employees & communities. After more than four decades here, I can say with confidence: this is a decision rooted in progress, member benefit, and the long-term health of our credit union.

First Tech Employee Edward Powers Responds

An employee of First Tech responded to some of the statements made by members on the NCUA site.

“Thank you for your membership at First Tech! I am also a member and an employee at First Tech. We value the questions and comments you posed regarding the merger of First Tech and DCU. First Tech and DCU remain strong viable credit unions with capacity to serve the needs of existing members long-term,” the poost by Edward Powers reads. “Together, we can move beyond historical service and product standards to create lasting economic benefits for current and future members. By every metric, we are better together and committed to proving this point to members for generations to come.

“How will your financial life be improved by the merger?

- Lower Loan Rates – Members will continue to benefit from competitive loan rates that remain 50–75% below market averages. Even as rates rise elsewhere, ours should move more slowly, helping your family save more on auto loans, mortgages, and personal loans.

•Higher Share Rates – As you’ve probably noticed, DCU and First Tech pay above market rates on nearly all deposit accounts. This combination positions your credit union to maintain market-leading savings rates while investing in strategies that keep us competitive in a rapidly changing market. - Lower Fees on Everyday Transactions – We’re reducing or eliminating fees to make banking more affordable. That will be more money in members’ pockets.

- Simplified, Efficient Service – Expanded branch access while keeping the same accessibility you know and love today with the addition of streamlined processes to make managing your finances easier and more convenient. We’ll continue to support the Co-Op Shared Branch Network delivering access to more than 5,000 branches and 30,000 ATMs across America. That exceeds levels of convenience offered by most regional banks.

- Cutting-Edge Technology – We know that most members prefer to save time and money by transacting through digital channels. Through this merger, you’ll benefit from significant investments in digital tools and mobile experiences that ensure secure, seamless banking wherever you are.

- Strength to Compete without Losing Personal Connection – While membership will grow to more than two million members, we will remain focused on delivering highly personalized experiences to fully support you throughout all stages of your life.

- This is a transaction that enriches members! Neither Shruti Miyashiro, CEO of DCU, or Greg Mitchell, CEO of First Tech, will receive any special additional compensation as a result of the merger. Benefits payable to other First Tech executives listed in the Member Notice range from zero to the maximum listed number should they depart from the credit union and become eligible to receive previously vested retirement and other benefits.

Together, we’re building a stronger, smarter credit union that helps your household thrive.”

Payouts Proposed for 5 Execs in Pennsylvania Merger

Merging Credit Union: Benchmark FCU, West Chester, Penn.

Assets: $297.7 million

Members: 9.330

Year Chartered: 1940

Date of Member Vote: Dec. 2

Acquiring Credit Union: Franklin Mint FCU, Chadds Ford, Penn.

Assets: $1.87 billion

Members: 149,973

Benchmark FCU’s board told members the merger will allow it to provide a wider range of products and services and will also lead to economies of scale that will permit it to “better compete in an increasingly competitive financial services industry.”

It also cited increased branch locations as a benefit of the merger. If approved by members, the credit unions have set a March 1, 2026 date for the combo.

Payouts to Management

In its disclosure form, Benchmark FCU said five people (whom it listed by last name only) will be paid merger-related compensation, including, “previously accrued extended bank payout” and “retention bonus,” respectively, as shown below:

- President and CEO Daniel J. Machon: $25,539.49; $20,750.83

- CFO Ray Massi: $10,400.62; $20,030.82

- VP-Lending-Consumer Donna Filippone: $9,725.50; 14,874.29

- VP-Retail Services Christopher Breslin: 8.962.69; $14,680.69

- VP-Lending-Commercial Mark Pizzi: $8,337.54; $13,985.56

The payouts exceed Benchmark FCU’s net income for the first ninie months of the year.

Financial Performance

Through Sept. 30, Benchmark FCU had $56,987 in net income and net worth of 10.41%. Franklin Mint FCU posted $7.14 million in net income and net worth of 7.83% as of the same date.

Three C-Suiters Offered $125,000 Each

Merging Credit Union: U.S. Employees Credit Union, Chicago

Assets: $102.3 million

Members: 6,059

Year Chartered: 1953

Date of Member Vote: Dec. 2

Acquiring Credit Union: Credit Union 1, Lombard, Ill.

Assets: $2.29 billion

Members: 160,552

U.S. Employees’ message to members used the same language as the messages used by the numerous other credit unions that are merging into or have merged into Credit Union 1, including that the latter “operates with the technology and systems that align with are members’ needs: and that “internal core values align with our own and give us confidence our membership will experience the same quality of service, but with new and expanded service operations.”

It added that the merger would also bring “synergy.”

The form cited more than 40 new branch locations that will be available to USECU members, and said Credit Union 1 had agreed to retain all USECU employees for three years and to provide a minimum base salary increase of 5%. All employees will also be paid 50% of their accrued sick leave.

Merger-Related Compensation

Three people will be offered merger-related incentives—COO Nilda Padin, CFO Frank Nicholson, and VP-IT John Morin, of $125,000 at the completion of the merger.

President and CEO Eric Stiegel will be offered continued employment with Credit Union 1 until his retirement on April 19, 2028.

Financial Performance

U.S. Employees had $866,961 in net income and net worth of 12.46% as of Sept. 30. Credit Union 1 had $4.6 million in net income to go with net worth of 11.04% as of the same date.

A CU With $414 in Net Income Looks to New Partner

Merging Credit Union: Cecil County School Employees FCU, Elkton, Md.

Assets: $26 million

Members: 2,527

Year Chartered: 1953

Date of Member Vote: Dec. 3.

Acquiring Credit Union: First Financial of Maryland FCU, Sparks, Md.

Assets: $1.32 billion

Members: 77,094

Cecil County School Employees told members they should vote yes on the merger because the shared resources will “allow the combined credit union to enhance product and service offerings and member convenience through better technology, more product and loan offerings and more locations/ATMs.

It said it will also continue to have a “strong social responsibility: the communities it serves and that the two CUs share a “strong, value-based culture.”

Financial Performance

Cecil County School Employees FCU had $414 in net income through the first nine months of the year, and capital of 10.04%. First Financial reported $1.54 million in net income and net worth of 17.7% as of the same date.

The River is Red in Colorado

Merging Credit Union: Mountain River Credit Union, Salida, Colo.

Assets: $31.4 million

Members: 3,056

Year Chartered: 1960

Date of Member Vote: Dec. 6

Acquiring Credit Union: Power Credit Union, Pueblo, Colo.

Assets: $122.9 million

Members: 11,773

Mountain River CU told members it needs to merge because its merger partner will provide members with four new branch locations, along with new offerings that include checking, manufactured home loans, bankruptcy rebuilder loans, and more.

Mountain River posted a $252,250 loss through Sept. 30, with net worth of 7.33%. As of the same date, Power CU had $1.52 million in net income and net worth of 12.6%.

CCEFCU Pitches Combination as a High Point

Merging Credit Union: Cattaraugus County Employees FCU, Little Valley, N.Y.

Assets: $17.8 million

Members: 1,606

Year Chartered: 1968

Date of Member Vote:

Acquiring Credit Union: High Point FCU, Olean, N.Y.

Assets: $410 million

Members: 20,950

“This merger will deliver enhanced resources, employee support and infrastructure that come with being part of a larger institution,” Cattaraugus County EFCU told members. “Additionally, it will expand our product and service offerings across a broader membership base. Members will also gain increased access to branch locations, ATMs and ITMs situated within the larger field of membership.”

CCEFCU had $216,775 in net income through the first three quarters of 2025, with net worth of 11.72%. High Point FCU had $1.046 million in net income and net worth of 14.15% as of the same date.