NEW YORK–Rising costs, property taxes and home insurance premiums have contributed to a jump in serious mortgage delinquencies in the U.S., especially in certain states.

Serious mortgage delinquency rates started climbing across the country in mid-2024, reversing a trend of steady declines established in the previous three years, according to a new report by Cotality.

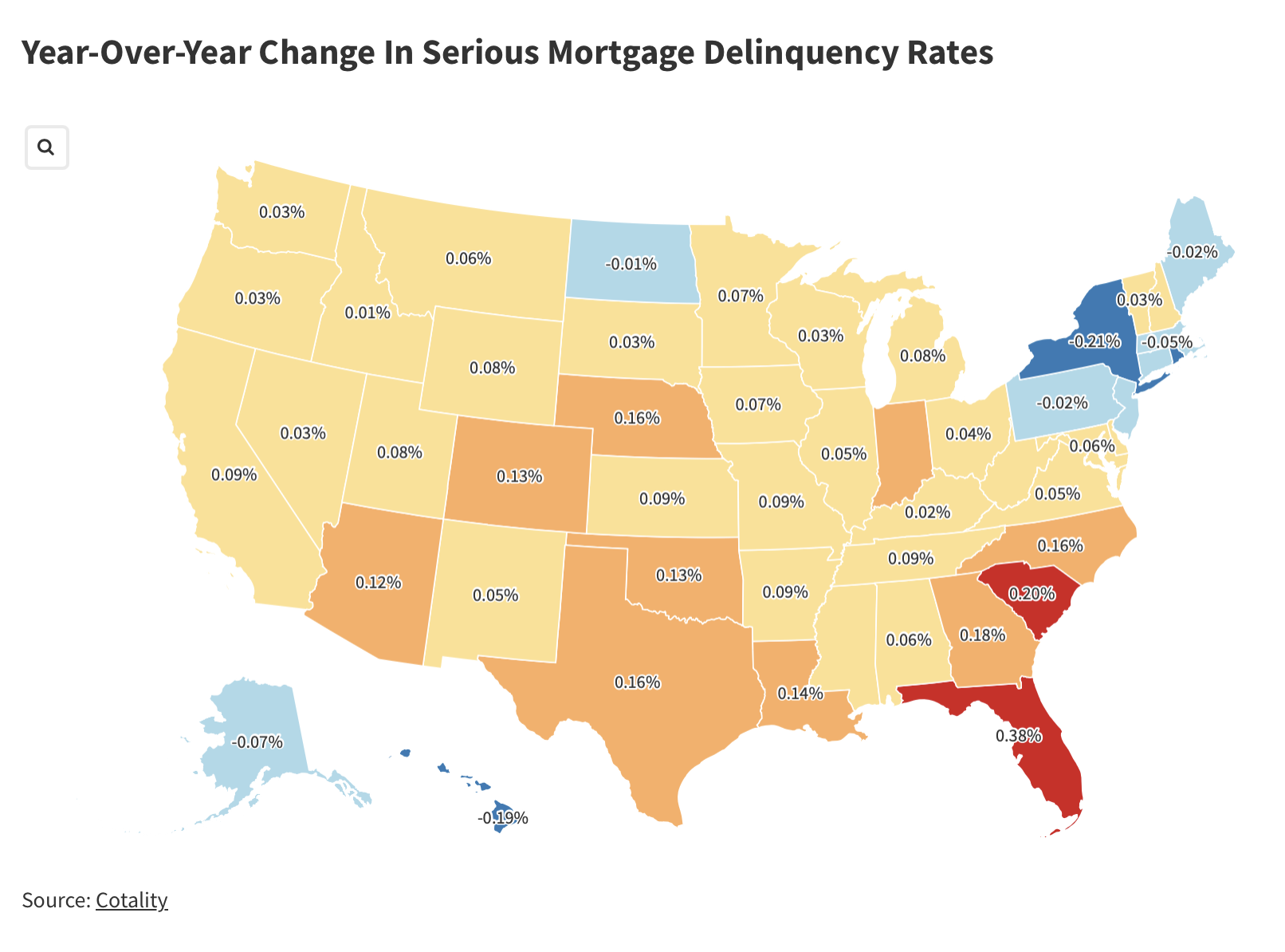

Nearly all states have seen a slight uptick, but in some, including Louisiana, Florida, and Georgia, delinquency rates have seen big jumps over the past year, according to the analysis.

Cotality defined “serious delinquency” as any mortgage loan that is 90 days or more past due.

Troubled States

According to Cotality:

- The biggest year-over-year increase in serious delinquencies in the nation was reported in Louisiana, where rates went up by an overall 1.87% for all loans. Specifically, conventional loans saw an uptick in serious delinquencies of 1.25%, FHA loans of 3.96%, and VA loans of 5.44%.

- It was followed by Florida, with a 1.43% year-over-year increase for all loans; Oklahoma, with 1.24%; Georgia, with 1.12%; Texas, with 1.11%; Indiana, with 1.09%; South Carolina, with 1.05%; North Carolina, with 0.83%; Nebraska, with 0.81%; and Colorado, with 0.55%.

Colorado, Georgia and Florida, which experienced the three highest year-over-year increases in serious delinquency rates between 2024 and 2025, also reported the highest jumps in property taxes between 2019 and 2024, according to Cotality analysis.

Insurers Exit States

Those states have also seen a big increase in home insurance rates as natural disasters have struck. Many states have also seen insurers exit their markets, leaving homeowners scrambling to find coverage.