WASHINGTON–Is a merger the only option for a credit union that wants to ultimately be relevant? Perhaps, but it shouldn’t be, according to a panel that has weighed in on the question.

The issue was debated during Mitchell Stankovic’s Underground here, which was held at the Hay Adams Hotel in conjunction with America’s Credit Unions’ GAC.

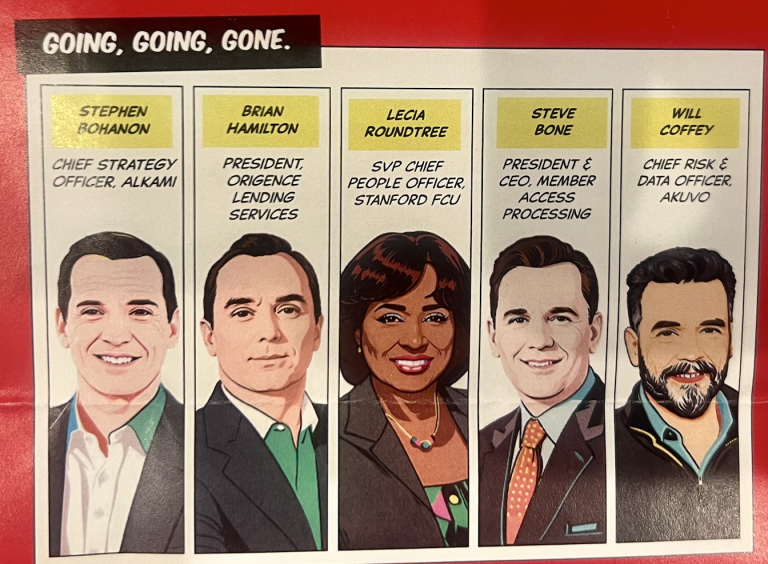

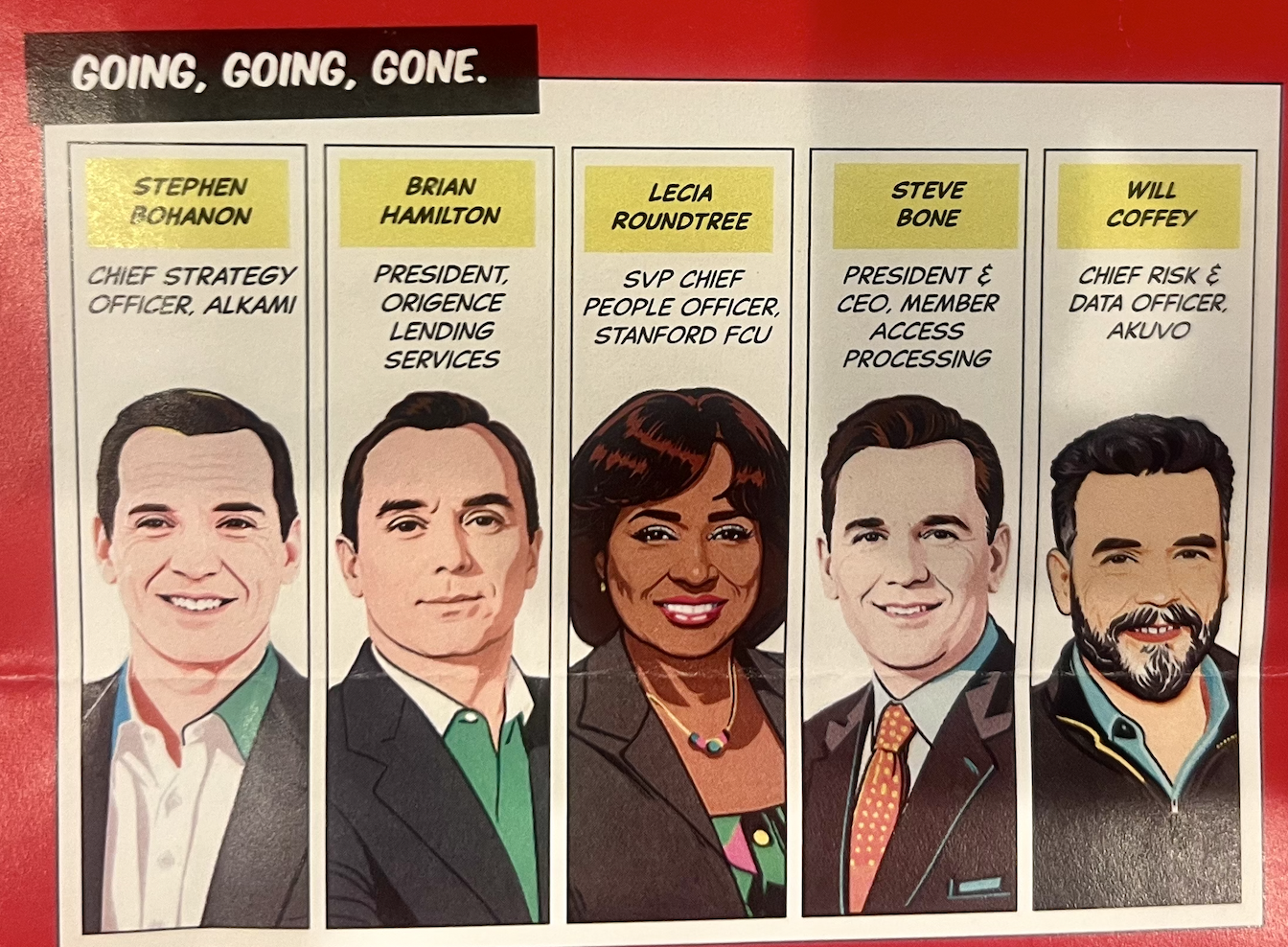

Participating in the session titled “Going, Going, Gone” were Brian Hamilton, president, Origence Lending Services (who acted as moderator); Lecia Roundtree, SVP-chief people officer with Stanford FCU; Steve Bone, president and CEO of Member Access Processing, and Will Coffey, chief risk and data officer with AKUVO.

Here is what panelists had to say:

‘It Depends’

Hamilton: What do we have to do and how do we stay relevant if it’s not through consolidation?

Coffey: The question of whether to consolidate or not to consolidate is one I’ve been hearing, and I think the answer is it depends. But what I think is also very relevant is the anxiety and the concern that folks have. You can be paralyzed by that.

One of my roles is risk and one of the risks that I’m hearing today is the risk of inaction. As far as how to take action, whether it’s to lean into a merger or to lean away from it, I think it’s really two things.

Attention to AI

One, I’m no stranger to technology. I grew up in technology. A thread I’ve heard in some of the discussions today was around how can we compete. In my opinion there’s nothing bigger right now than the impact of artificial intelligence. If you don’t have a project or you’re not working with a vendor that has artificial intelligence, you’re not stepping out into that, you’re behind, and I don’t want us to be behind.

If I were you I would say, ‘Hey, you know that sounds like a good idea but what does that mean?’ Over 70% of folks that are working with artificial intelligence right now at different companies, banks, credit unions, the idea is operational efficiency. Start there.

Whether you’re going through a merger or you’re considering one or you’re wanting to make yourself more robust to avoid a merger, look at your operational inefficiencies and leverage artificial intelligence to start down that path.

Regulators are Worried (For Themselves)

Two, the regulatory landscape. Whether it’s the uncertainty of which regulator I’m going to be partnering with or is there going to be a consolidation, lean in. One thing I’m hearing loud and clear through the discussions today is around how we’re relationship-focused and I’ve got to imagine that the folks who are sitting at the OCC or NCUA are nervous themselves. How do you get through the nerves? You lean in on your partnerships, your relationships, to help navigate.

A ’Different Perspective’

Roundtree: I have a little bit of a different perspective. When you ask how do we avoid the consolidation and the mergers of credit unions, my perspective is maybe you don’t unless we really start looking at the inner workings of our organizations.

I’m on the people side of the business and I look at it and I think of it in terms of how are we getting that message. I have no doubt that everyone in this room gets it, gets the importance of innovation, gets the importance of problem-solving and all of those things that are going to make the difference to our members so that they want to do business with us, so that they tell our friends and we grow.

Do They Get It?

I wonder how much of that message is getting translated to that next level down of leadership and maybe that frontline of leadership. I wonder about that because sometimes we are moving so fast and it shouldn’t be to the exclusion of communication. I wonder if we understand the purpose of the movement and everything that it is we’re trying to accomplish. Does that next level really get it? If not, I think we are missing something big,

Those people who are frontline talking to our membership–do they get that innovation and are they using best practices? Are we bringing them together to ask, ‘What are you hearing and how can we get better from the members’ perspective so that we can grow our credit unions?’

I think we need to pay attention to those people who are cream of the crop employees and let them help us grow

Need Everyone For Scale

Bone: Seventy-three percent of credit unions are under $250 million in assets and there aren’t a lot of (vendors) who are even going to talk to them. The six credit unions that own us have a very transparent not-for-profit financial model. We come to work every day…and we’re here to democratize technology and people and processes for small credit unions.

But the reality is we can’t do that without the fairly large credit unions that own us and are also our clients and customers. So, there’s a bifurcated approach to how we do that, meaning we have to be able to do certain things with large credit unions. But then our goal is to give the same level of service, the same technology access to a $23 million credit union and a $6 billion credit union.

The Good News

The good news is there’s lots of ways that we do that, they’re very straightforward, they’re very simple, they’re risk-mitigated.

Solving the challenges of small credit unions (means we will) need everyone in this room to help to scale them. There’s a lot of very practical things that can be done every day, whether it’s your debit and credit products, your lending, there are all sorts of solutions.

I would say as a big advocate for CUSOs that they are one mechanism to do that. There’s a certain enablement when you’re a CUSO. You have credit unions that want to help credit unions, there are tools that can enable a small credit union to be involved in the Netflix of banking. The rise of Netflix (was a) big model change. All of the same tools are needed to help small credit unions; they’re all available. It’s about making them accessible.

Getting Together for Scale

How do you get to the niches and the segments of the humans that need help? You help small credit unions be just as good at the large financial institutions.

One thing I’d ask you to take away is that everyone in this room has the community right here to democratize the capabilities that small credit unions need. We just need to get together and scale it.