WASHINGTON–According to a panel of credit union and industry leaders, there is a new four-letter word that has replaced “bank,” force-placed insurance is a product every CU should rethink, and fighting poverty is an issue every credit union should “lean into.”

During a session at Mitchell Stankovic’s Underground meeting here titled “Bullocks, Nonsense and Rubbish,” the panelists offered their takes on what they think fall beneath that umbrella.

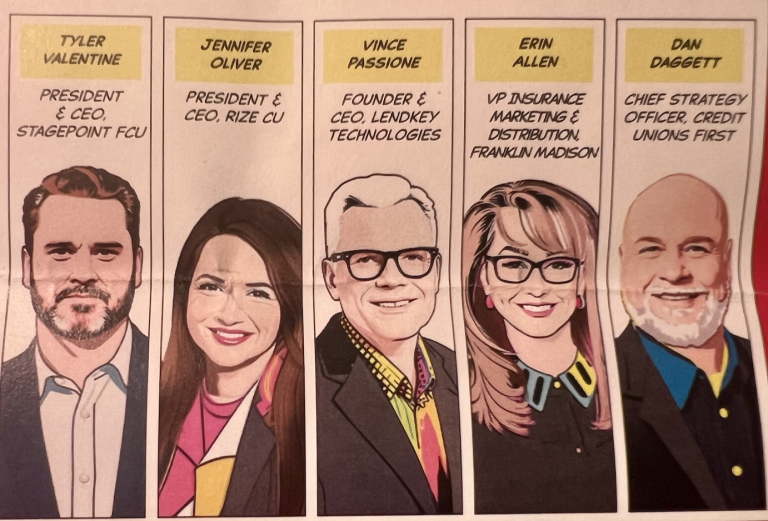

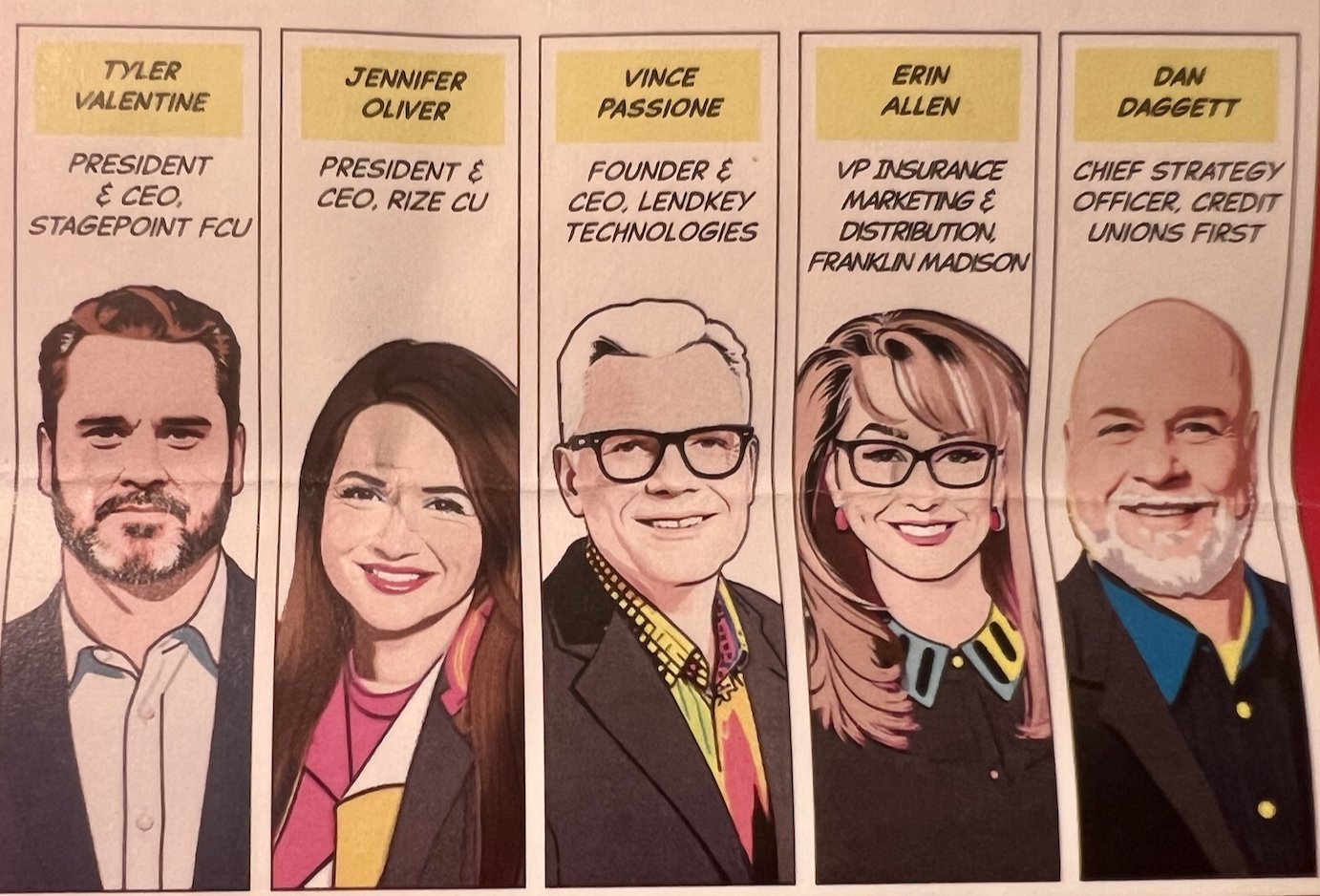

Participating as panelists were:

- Tyler Valentine, president and CEO of Stagepoint FCU (moderator)

- Jennifer Oliver, president and CEO of Rize CU

- Vince Passione, founder and CEO of Lendkey Technologies

- Erin Allen, VP-insurance marketplace and distribution with Franklin Madison

- Dan Daggett, chief strategy officer with Credit Unions First

Here is a look at some of what was discussed:

Valentine: Where are we missing the mark in lending?

Passione: We’re in the lending business. I have 400 clients, all of them are credit unions. My clients actually look like the credit union demographic–67% are under $250 million. When I look at this business the first thing I’d say is there’s a definitional discussion. I hear this word fintech thrown around all the time. A fintech to me is someone who actually goes out and uses technology to try to do what you do and actually competes with you. A partner or vendor is someone who supplies you with capability so you can do what you do now.

Earlier, another panel participant said credit unions need to learn how to organically make a loan again. In the last five years I’ve watched more credit unions buy fintech loans and put them on their balance sheets. I don’t really understand what’s happening.

Fourteen years ago we started collaborating with credit unions trying to figure out how to really give them access to markets and we came up with this interesting model that we kind of call network lending. It’s actually what you all have been doing for a very long time, which are loan participations. (The 26 credit unions that formed the company) agreed to come up with a commonly branded, commonly underwritten and commonly priced loan and they put it in the market. They originated for their members, they acquired new members and then they immediately syndicated the risk across all the participants.

Up Against (Much) Bigger Budgets

JP Morgan Chase is going to spend $15 billion on technology this year. PNC’s going to spend $3 billion. Collectively, you can’t keep up. But using the collaborative model why wouldn’t you commonly brand, commonly underwrite, and commonly price and then leverage the wisdom of all the people in this room, the wisdom of the crowd, to deliver that solution. You will lower the price of technology, you will lower the cost of implementation, you’ll leverage your collective knowledge and you’ll be able to you’ll deliver the kind of services that you’d like to deliver to your members.

Second, embedded finance is coming faster than we all expect. At the point of sale you can now check out (and make a large purchase) without going into a branch anymore. You don’t even know about the credit union. How do you get access to the point of sale if you’re a credit union that’s $10 million or $100 million in assets? The answer is a network lending approach.

Technology is now becoming much more expensive than it’s ever. AI quantum computing is going to be super-expensive. NIM is shrinking. The only way you are going to reduce fixed costs is by organizing yourselves in these kinds of consortiums

The Opportunity in Insurance

Q: From an insurance perspective, is there an opportunity for credit unions?

Allen: When I think about our industry it really comes down to a lot of talking, but we don’t do a lot of doing. I got in this industry almost 30 years ago when we talked about our aging demographic, we talked about the cost of technology and we talked about banks. And here we are talking about the same exact things.

What we forgot to think about was the other competition and that’s digital banks and they have come in and they are taking our members.

What I would say to you is the new four-letter word should be SOFI. In 2024, they grew by 2.6 million customers and surpassed 10 million total customers. Why does that matter to Franklin Madison? Because SOFI is getting into insurance. That revenue is going to let them continue to innovate and evolve.

The second thing is because they don’t want anyone leaving their ecosystem. They want to be the one-stop shop. Research shows 44% of consumers want insurance through their financial institution. That’s up from 33% just three years ago. The largest groups, the younger demographic and high-wealth, high-income consumers who we want, they don’t come to us. We’re not actively engaging with them; 48% will tell you they have not gotten insurance offer from their financial institution.

Where to Do Better

When I think about what we need to be doing better…I think we’re missing financial education, financial literacy, wealth management, or, with Franklin Madison, that protection piece–we’re really missing that.

‘Losing Sight’

Valentine: When you look at the future and position credit unions to be relevant and thriving, what are you looking at?

Daggett: The first mindset we all have to remember is that we’re here to work for the members of the credit union and sometimes we lose sight of that with the programs that we have in place.

One of the programs that we have in place, and majority of credit unions do, is automobile forced place collateral protection insurance programs. I don’t think anybody in the audience that’s familiar with those programs would say that’s in the mindset of our philosophy of people helping people.

Most of the contracts that you have with your current providers have something called the premium deficiency endorsement. Do any of the folks in the room understand what that endorsement means and the impact to your bottom line? That endorsement carries with it a loss ratio–sometimes it’s 50 or 60%–and you sign that agreement stating when your loss ratio hits a 60% ratio you’re going to treat some of your members differently than you treat other members.

An Example Cited

As an example: you have a member with a $6,000 loan balance and they let their insurance lapse for some reason. Why did they let their insurance lapse? That’s one question you should ask yourself. Second, typically the premiums are about 20% of the outstanding balance, so you’re going to add $1,200 to that loan balance. Let’s skip ahead six months. You repossess that collateral. The credit union loss ratio is 58%. They can then file a premium deficiency claim and get that $600 paid back on the member’s loan. Fast forward a few weeks and they have some losses. Their loss ratio is now at 62%. If that same member had their vehicle repossessed they wouldn’t have that $600 put back on their loan.

So, how are we treating those two members in the same vein favorably?

Let’s say your trusted financial provider Dan Daggett is going to call you and I’m going to ask you to write a check to me for $10,000 for a program you might be interested in and in 12 months’ time, if everything goes well, I’m going to send you a check back for $6,000 of that $10,000? Why are credit unions writing that exact same check on their members’ behalf ? If you wouldn’t write it personally why would you write if you remember

Size Doesn’t Matter

Valentine: What are you thinking about in lending, marketing, strategy and all of this?

Oliver: (Asset) size doesn’t really matter. All the things we’ve been talking about today…are challenges where size doesn’t matter in solving those big huge problems. It takes tremendous effort from all of us together.

I was thinking about the beginning of this year. We have this crazy flurry of administration changes. We have this crazy narrative happening right now and it’s everything all at once. I say WTF, stop the madness. We have got to get a lean in to the things that we can control. What I can control is my members. If half of Americans can’t afford $400, half of Americans are on the brink of poverty.

Why not change the narrative? Why not hit that straight in the face and say we are here to change poverty? Those are big words and you know it sounds scary, but this is how we can be really, really relative as credit unions. We are here to help the little guy. And the little guy could be making six figures and still be living paycheck to paycheck.

Changing the World

I think we can go out and we can change the world, but we’ve got to do it together.

In this crazy world of everything all at once I’m actually more optimistic than I’ve ever been, because what you lean in with the things that drive you; you lean into what is right and what is right is—goddamit– credit unions.