WASHINGTON–Does your CU really know how to make a loan organically? Are you missing a market that is a country within the country? Is your budget your strategic plan?

Those questions and others were discussed as part of a panel titled “You Don’t Know Until You Know” during Mitchell Stankovic’s Underground Conference, held in conjunction with America’s Credit Unions’ GAC.

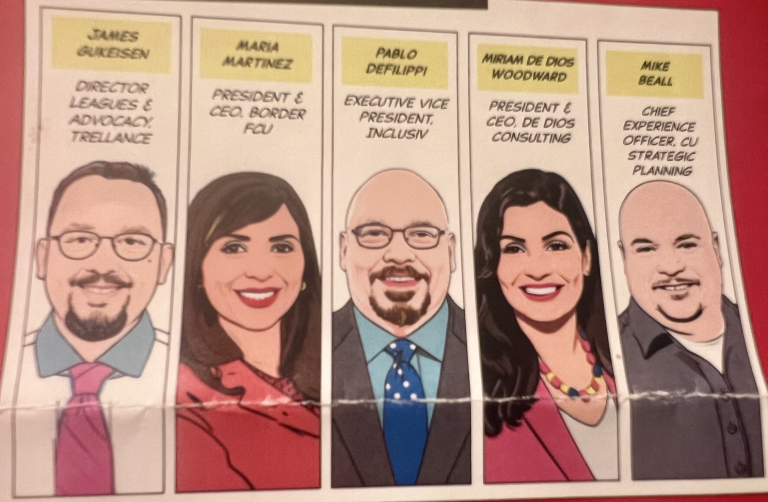

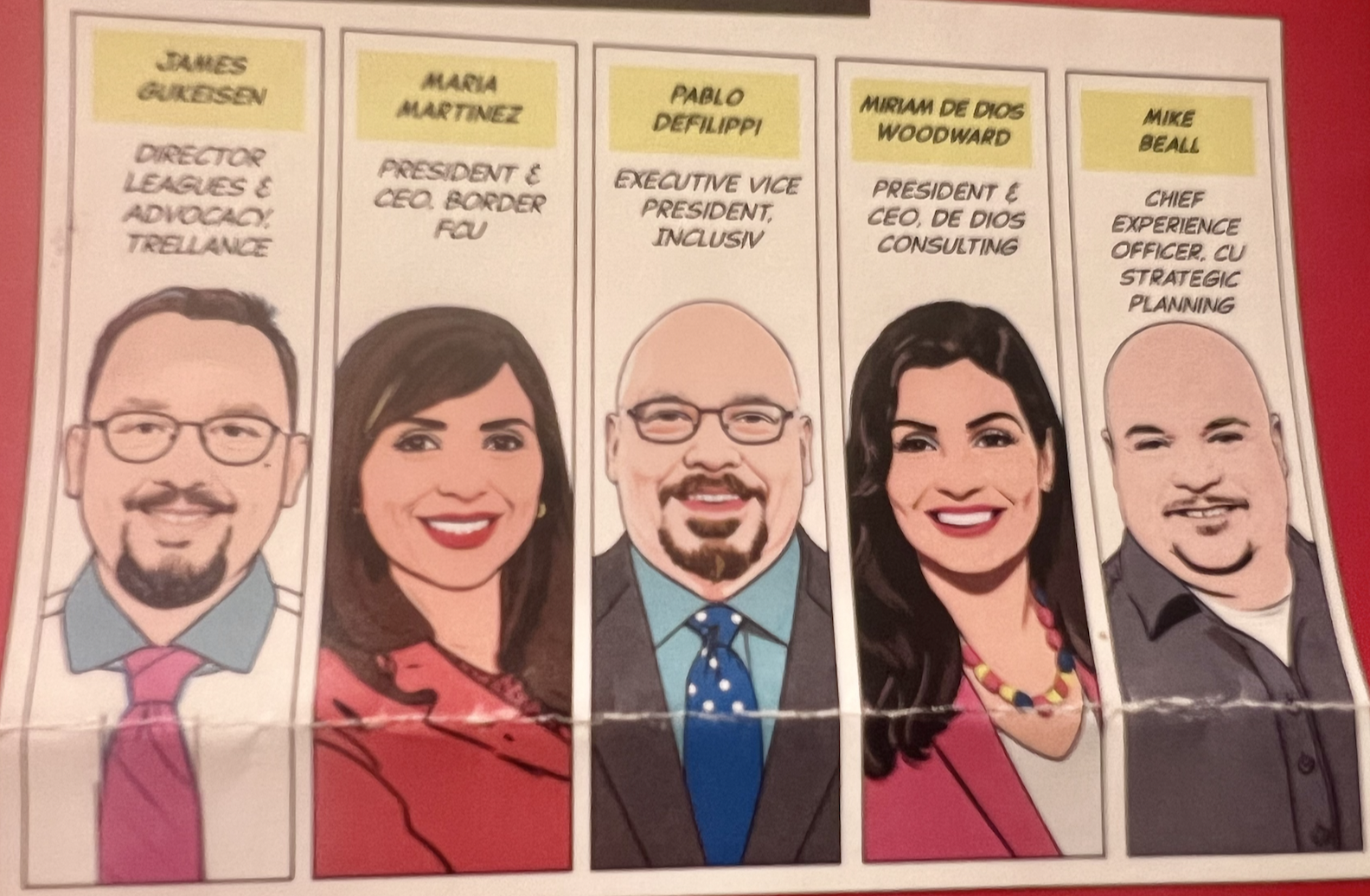

Participating as panelists were:

- James Gukeisen, director leagues and advocacy with Trellance (moderator)

- Maria Martinez, president and CEO of Border FCU

- Pablo Defilippi, EVP with Inclusiv

- Miriam de Dios Woodward, president and CEO of De Dios Consulting

- Mike Beall, CEO of CU Strategic Planning

Here’s a look at some of what was discussed?

Gukeisen: What do you know?

Beall: I loved that question from the first panel today that asked are we relevant? I work in the CDFI land where we tried to really look at resources for credit unions. We really look to try to help credit unions really focus on low- to moderate-income consumers.

Now, we’re facing potential cuts to Medicaid and VA benefits and Social Security. The safety net that that we’ve all as a country looked at is in jeopardy,” said Beall. “Are we even ready with products and services? Are we prepared in any way to help folks who are in the 20% of folks that receive Medicaid? I look at this and say that relevance is in question. I am a board member on a $90 million credit union, DC FCU. My challenge to you in this room, and I see it every day in conversations with credit unions, is do you actually know how to make an organic loan? So many credit unions are buying loans to fill their lending. I think it is an SOS. Does your staff have the expertise, the experience? Do you allow them to say yes to members and their loans?

A Pending Crisis

I think this is a crisis that we’re going to learn about over the next several years in in a way that means we’ve got to not only navigate what’s going on, but we’ve got to also figure out whether we have the products and services, with loans being a significant part of that.

I sat with my own board and said, ‘Look, I’m not going to simply vote for raising our deposit rates if we don’t have products that are going to bring in new deposits. We raised the rates and deposits went down! We didn’t have the products or we haven’t explained them well enough to our members.

Huge Market Outside the Financial Mainstream

DeFilippi: We have a whole market of more than 100 million people who are basically outside the financial mainstream.

The number of people who are unbanked and underbanked has grown exponentially and an existential crisis is unfolding right in front of us. That is only going to accelerate.

So, one question for you all to think about is what does it mean when we talk about poverty, because what I’m hearing on the news now is that everyone has the same access, everyone is equal. There have been efforts to address those inequalities in the marketplace and those efforts are being systematically eliminated. That’s going to create more need and more people struggling, because they won’t have access to equitable financial services.

If don’t know how to make loans in that market we’re going to be even less irrelevant so one thought is we have to go back to basics we have to remember how we serve our members. Yes, digital channels are great but it’s not the only way that you connect with these communities.

A Country Within a Country

I want you to remember that we have a whole country within this country that has no access to the financial mainstream.

We blame people for being poor and especially now we’re hearing a lot more that if you’re poor it is your fault. Poor people pay more for everything. It’s expensive to be poor. We can do this and we should be doing this…

The second thing is immigrants. What’s going to happen these people? These people are our neighbors…We hear all this news that all this is illegal. There’s nothing in the financial system that says that serving an immigrant is illegal…You can do it, you should do it. People don’t forget. I came to this country as an immigrant and I tell you the first credit card they gave me I still have in my pocket.

Time to Step Up

Martinez: I think this is the time to step forward and start doing more. I think a lot of credit unions are scared that these (immigrants) are going to take off and they’re not going to pay, but trust me, they’ll be back. They’ll come back even if they deport them because they’re so used to our system in the U.S.

One of the things I learned as a CEO is–I have an accounting degree– I used to do my budgets and I would always look for the bottom line because you want to report to your board that you have a good bottom line. My strategic plan was my budget. But I stopped doing that many, many years ago. What I started working on was programs that were going to work for my community. When I started doing that—such as the VITA program, the financial counseling for members and non-members in our community and we were the only ones in the area, and because of that my income started growing because I concentrated so much on serving others versus making sure that I had a bottom line.

‘A Tough Job’

We serve 13 rural counties and most of them are underserved and the majority of them are considered low-income communities. I have a tough job because I want to make sure that those people that were not banked are being banked. The biggest fight that we have in our community is with payday lenders because there’s 30 of them and there’s only one credit union in my community. We have to continue fighting in order for us to bring the services to them

This is not a time to relax, this is a time for us to be out there making sure that we’re making I think that’s still important thank you so much for your help absolutely well what happens when you get three let me

The Question of Relevance

De Dios: Talking about the immigrant situation today I want to come back to the question of relevance. Right now we have an opportunity to be relevant to the communities you’re serving. Now is the time to act to provide that awareness of you as a credit union partner, a community partner for them to share resources on where folks can go.

This is impacting a variety of families–undocumented, documented, mixed status households. This could be impacting some of your employees today, so provide awareness of basic things like potential joint ownership on accounts and looking at powers of attorney . That could mean referring folks to organizations where you can get additional information. But also prepare your employees to provide that information.

I’m thinking about something that really gets me fired up and that is how, largely, our credit union industry is missing the opportunity to serve the Latino market as a whole. I would venture to say we’re largely ignoring our Latino market. This is 65 million people. The Latino market has grown at twice the rate of that of the non-Latino white market. This will be $265 billion by 2030. How much of that is going to credit unions?

The ’Kicker’

The kicker is that Latinos need and want our services as an industry, so back to relevance. This is a market you can be very relevant. Fifty-five percent of Latinos are dissatisfied with their financial service providers and the products and services that they are being provided. I can attest to that having become a small business owner in the last year. I really wanted to start my small business account at a credit union and I struggled to find one that was relevant and that connected with me.

Did you know that Latinos are willing to pay more for the right financial products and services that are tailored to them, up to 10% more.