ALEXANDRIA, Va.–With the NCUA chairman expressing some frustration that the agency even has to issue an FAQ document on brokered and reciprocal deposits was shared during the agency’s board meeting.

The frustration was over the fact the update is not an update at all. Instead, the new FAQs the agency has produced were created because credit unions were hesitant to participate because they had not been expressly told they could, even though NCUA has never said brokered and reciprocal deposits were prohibited, according to NCUA Chairman Kyle Hauptman and Frank Kressman, deputy general counsel with the agency.

Hauptman observed that it’s an ongoing issue that many credit unions “keep waiting for the affirmative,” part of what he called a “broader problem of “Mother, may I.”

“We did hear, whether we like it or not, that this useful thing that didn’t break any rules was not happening,” said Hauptman. “In speaking to some representatives of networks, they were saying the same thing, that they had quite a lot of interest from some credit unions, but they simply were afraid to put their toe in the water because they didn’t know what NCUA thought of it even though there wasn’t even the slightest hint anywhere (it was prohibited).”

What credit unions want to avoid, Hauptman said, is getting “even a raised eyebrow” during an exam.

He noted that in the new FAQs there is “literally no new information, no new interpretations, no updated language….Every single bit of it is regurgitating what was already known.”

He also said the benefits of brokered and reciprocal deposits are vast, but he added credit unions “should weigh the pros and cons for their specific institutions” because “an overreliance on brokered and reciprocal deposits can increase a FICU’s risk profile and lead to higher rates and downgrades in CAMELS ratings”.

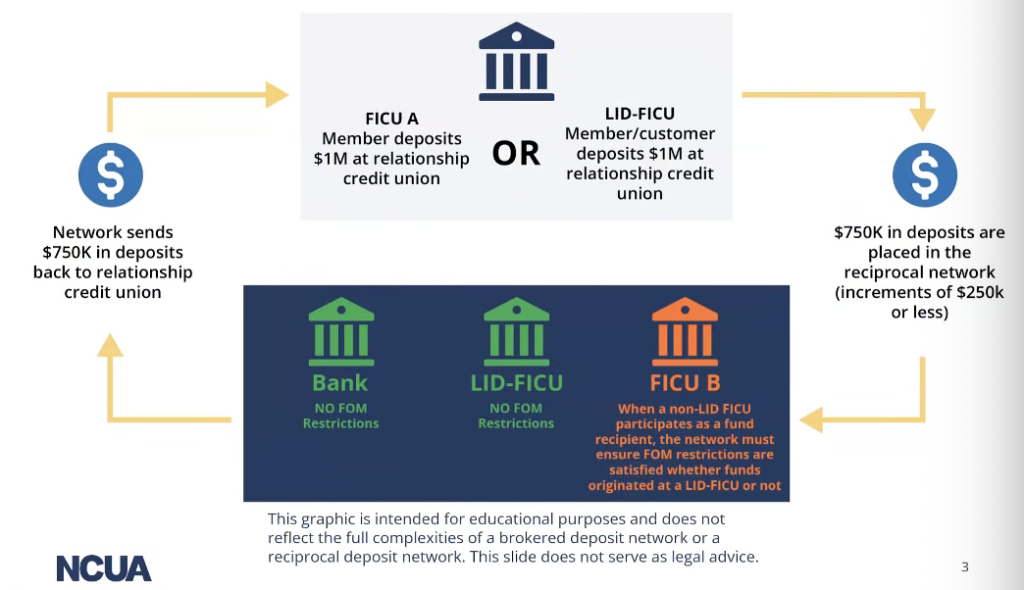

Details on the Q&A

In his remarks to the board meeting, Kressman said the FAQ should help federally insured credit unions (FICUs) “to better understand their options and remove any phantom barriers to entry.” Kressman noted some institutions had been hesitant because the NCUA had not previously stated explicitly that such activity was allowed.

Kressman emphasized the guidance does not advocate for participation, endorse any specific vendor or network, or provide a comprehensive review of how reciprocal deposits operate. Instead, it clarifies that the activity is legally permissible.

Kressman said NCUA defines brokered deposits as funds placed by a third party into a credit union, often to obtain higher rates or expanded insurance coverage. Reciprocal deposits, Kressman explained, are a subset of brokered deposits in which networks of credit unions and banks exchange matching deposits, allowing institutions to provide expanded insurance coverage while maintaining customer relationships.

According to Kressman, at least one credit union has reported that participation in such a network helped attract new members seeking additional share insurance and better serve existing members with larger balances.

Some Limits

However, he noted that participation is subject to statutory and regulatory limits. NCUA share insurance generally applies only to member accounts, as defined under the Federal Credit Union Act, though exceptions exist for certain entities, including nonmember deposits at low-income designated credit unions.

Those limitations can create logistical challenges for credit unions without a low-income designation, since deposits must come from members to qualify for insurance. By contrast, low-income designated institutions have greater flexibility to accept nonmember deposits.

About Pass-Through Insurance

Kressman also outlined how “pass-through” insurance works in reciprocal deposit arrangements, in which funds placed by an agent or nominee are insured on behalf of the underlying owner, up to the standard $250,000 limit in aggregate with other accounts.

He stressed that credit unions must comply with NCUA recordkeeping requirements to ensure insurance coverage applies.

While reciprocal deposits can expand services and coverage, Kressman cautioned that excessive reliance on them may increase risk, particularly if a credit union’s financial condition weakens. Such deposits can be more expensive and less stable than traditional funding sources, he said.