WASHINGTON–Are rising delinquencies on buy now, pay later (BNPL) loans a reason for concern? The data would suggest yes, but the biggest companies in the BNPL space say no.

When BNPL lending began to grow in popularity in recent years there were warnings that consumers would accumulate many small loans for frivolous purchases—meals from Door Dash or spur-of-the-moment impulse buys—that would add up and suddenly sock the consumer with accumulated debt and interest after not paying off the balance during the interest-free four installments period.

For credit unions, the risks were considered two-fold: the loss of card interchange as members turned to easy BNPL financing that was often embedded in online applications or available at point of sale, and risks presented by members whose pile of debt that didn’t appear on credit reports.

More recently, some of the most popular BNPL solutions have begun to report to the bureaus.

Growing Crisis?

Now, as companies like Klarna, Afterpay, Affirm, Zip, and Sezzle have become big players and competitors to credit unions for their members’ business, some new consumer data would seem to indicate a growing crisis as there are a rising number of defaults on BNPL loans.

The rise in defaults, of course, would not be a surprise, given the growth in lending. As of Dec 31, 2024 BNPL purchase volume was expected to total $132.7 billion, up 14.1% YoY. But critics say more is at work.

New Survey Findings

A new survey released by LendingTree found (41%) users of BNPL borrowers say they paid late on one of their loans in the past year, up from 34% just a year earlier.

“That’s just one of several troubling findings from our survey that asked people about their behaviors and perspectives around these popular loans,” Lending Tree said in releasing its findings. “Along with increased late payments, we found a significant number of borrowers who take on these loans use them to buy groceries or takeout and believe that successfully managing one will boost their credit score. (Spoiler: It won’t … at least not yet.”

The Findings

According to LendingTree, its survey found:

- “Surprisingly,” high-income borrowers are among the most likely to pay late, along with men, young people and parents of young kids. However, 76% of late payers were late by no more than a week or so.

- 23% say they’ve had three or more active BNPL loans at one time. “High-income people are the most likely income bracket to say so. Also, Gen Zers and millennials are twice as likely as baby boomers to say so. Meanwhile, 40% say they’ve never had more than one at a time,” Lending Tree reported.

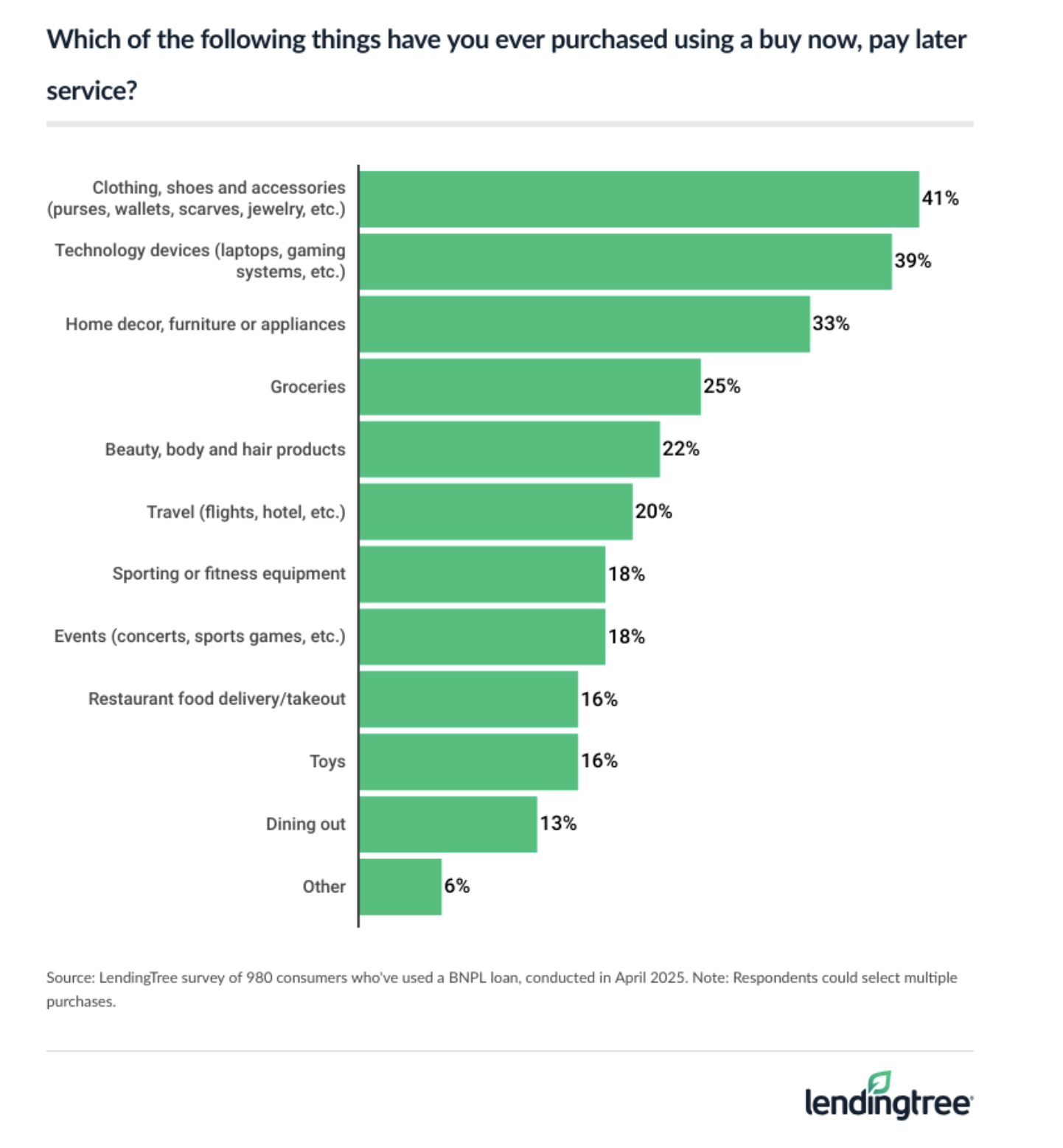

- 25% of BNPL users say they’ve used the loans to buy groceries. That’s up from 14% just a year ago. One-third of Gen Z BNPL users say they’ve done so, making it the fourth-most common BNPL purchase for that age group, trailing clothing, technology and home decor.

- Two-thirds of BNPL users say they’d consider using it for food delivery, and many are putting their money where their mouth is. DoorDash and BNPL giant Klarna recently announced a partnership to allow customers to pay for DoorDash deliveries with BNPL. “However, we found that 16% of BNPL users say they’ve already used BNPL for restaurant food delivery or takeout,” LendingTree reported.

- 33% of users see BNPL as a “bridge” to their next paycheck, up from 30% last year and 27% the year before. High earners, men, younger Americans and parents of young kids are among the most likely to say so, the survey found.

- 62%) incorrectly believe making on-time payments on BNPL loans helps your credit score. “Only 13% say they don’t help your credit score, which is correct, while 26% aren’t sure. Men and high-income earners are among the most likely to believe this falsehood. Younger Americans are more likely to believe it than their older counterparts, but even 54% of boomers do,” according to LendingTree.

- BNPL is everywhere. Almost half of our survey’s respondents say they’ve used a BNPL loan service such as Affirm or Klarna, including 11% who say they’ve used them at least six times.

- Men are more likely than women (53% versus 46%) to have used a BNPL loan. Also, the younger you are, the more likely you are to have used one: 64% of Gen Zers ages 18 to 28 say they’ve used one, compared with 29% of baby boomers ages 61 to 79. That 64% includes 16% who’ve used them six or more times.

- LendingTree said its May 2025 BNPL Tracker, which is fielded separately, shows that 39% of Americans are at least considering applying for a BNPL this month. That’s unchanged from April.

CFPB Shared Concerns, But…

Although the Consumer Financial Protection Bureau had been warning for years that customers would be especially vulnerable if the economy worsened, and called for measures to safeguard them, it has been largely dismantled by the Trump Administration.

As The CU Daily reported earlier, the CFPB has now announced it will not enforce a Biden-era rule that sought to treat pay-later lenders like credit card companies, such as by requiring them to provide monthly billing statements to customers and to offer protections to customers seeking refunds.

The New York Times reported that Democrats on the Senate Banking Committee plan to intervene and intend to call for more oversight of pay-later lenders, including pushing for more robust reporting on their loan losses.

‘Nothing Troubling’

But the BNPL industry itself says it sees no reason for alarm, according to the Times.

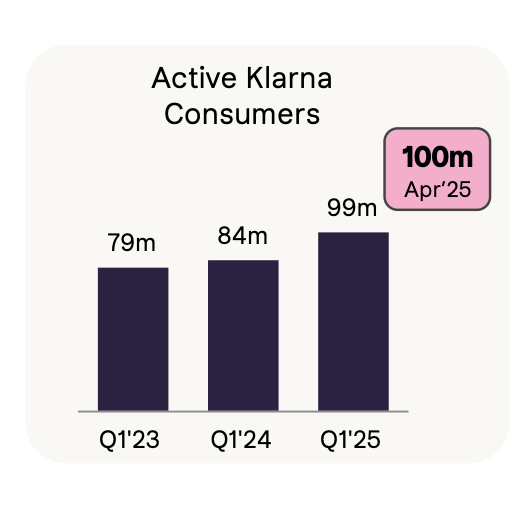

“That’s despite Klarna, one of the biggest providers, reporting a 17 percent year-on-year rise in credit losses this month,” the Times reported.

The company acknowledged that its losses were growing, but said that its default rate rose only marginally and represented a tiny share of its total loans, the report added. “There’s nothing troubling or worrisome from this data,” Clare Nordstrom, a spokeswoman, told DealBook, a publication of the Times.

Affirm, one of Klarna’s rivals, had a similar response: “We really aren’t seeing anything we would label as signs of stress with our borrowers,” CFO Rob O’Hare told the news outlet.

One Person’s Worries

But at least one person is worried.

“Consumers are going to be squeezed and more reliant on these products,” Julie Margetta Morgan, a former bureau official who is now president of the Century Foundation, told the New York Times , “and the companies are being offered a free pass to construct those products in ways that are the most profitable to them.”