WASHINGTON—As fall officially arrives, the question for many in credit unions is whether typical seasonal borrowing and spending patterns will arrive with the cooler weather, or whether all the economic flux will upend the seasons.

For many, the forecast is about as certain as the pattern with which leaves will hit the ground.

For financial institutions, the first day of autumn traditionally marks the start of a slower lending period compared with the high-volume summer months. Auto loans often taper off after strong sales fueled by summer travel and promotions, while mortgage applications typically decline as the housing market cools with the weather.

But while tariffs and job reductions have created negative drags on the economy, some have suggested the Fed’s recent move to lower rates could spur activity. A slow but steady decline in mortgage rates, for example, has helped to release some of the pent-up demand.

As the CU Daily has been reporting, mortgage refi’s saw a 58% leap in the most recent data and up 70% higher than the same period one year earlier.

Moreover, should lenders move to lower rates on certain products, consumers could look to consolidate debt ahead of holiday spending, especially credit card debt, which could be an opportunity for credit unions.

In Q2, total credit card balances in the U.S. rose by $27 billion to reach about $1.21 trillion, according to the Federal Reserve Bank of New York.

A ‘Clear Shift’

“As inflation persists and job growth slows, we’re seeing a clear shift in how consumers prioritize spending – especially in discretionary categories like Travel,” Norm Patrick, vice president, Advisors Plus Consulting with Velera, said in a statement accompanying the company’s recently released Payments Index (see related reporting). “While debit and credit activity showed modest gains overall in August, Travel purchases continued to decline for the second consecutive year, with Airlines and Lodging leading the pullback. These patterns reflect growing caution among consumers navigating higher prices and economic uncertainty. For credit unions, this is a critical moment to stay connected to member needs and deliver value through flexible, responsive financial solutions.”

Consumers Not Feeling the Pumpkin Spice

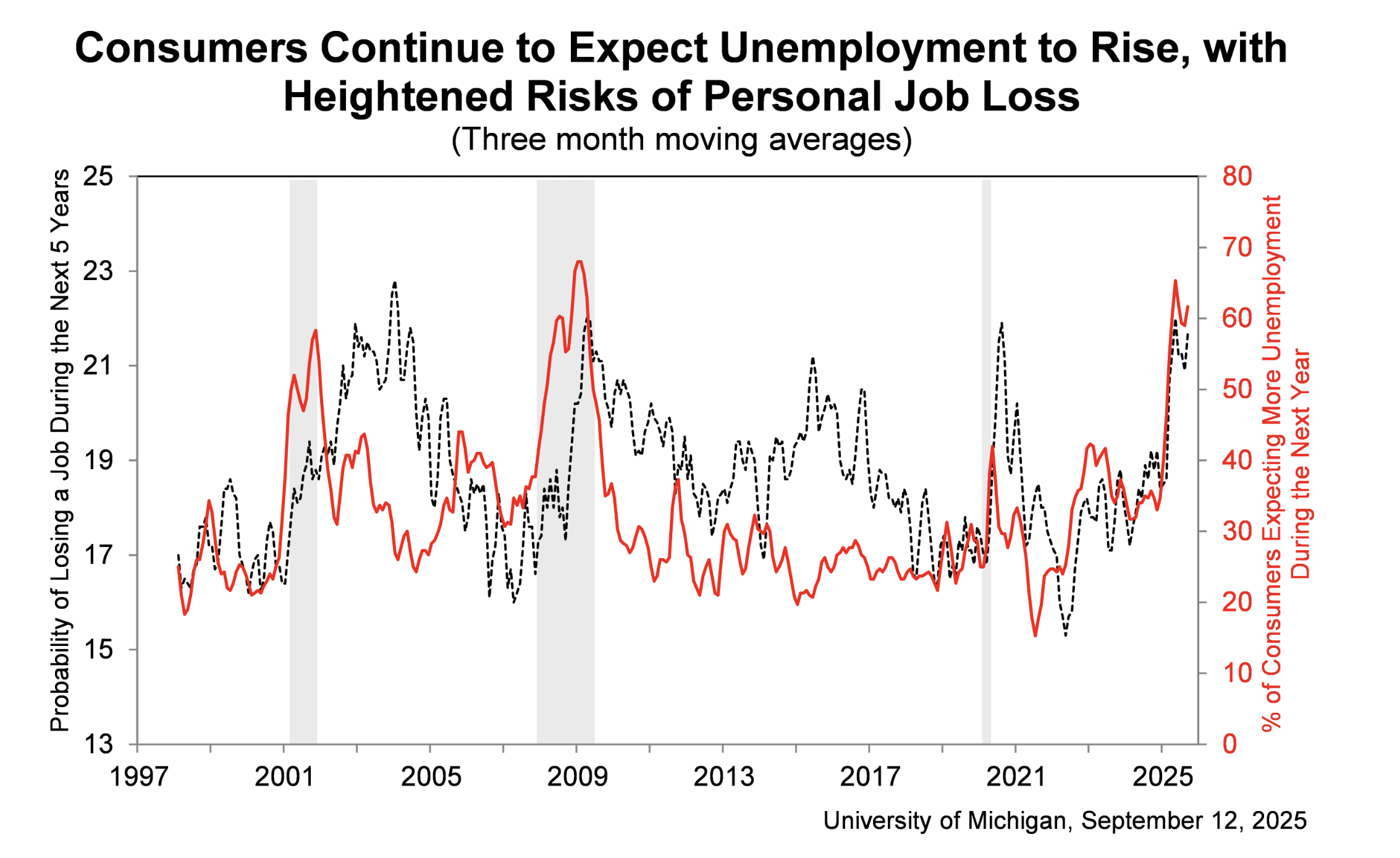

Meanwhile, consumer sentiment has also dropped like the leaves. The September 2025 University of Michigan Index of Consumer Sentiment decreased by 2.8 points, or 5%, compared to August, finishing at 55.4. The drop is strongest amongst middle- and lower-income consumers, according to the Index.

For the eighth consecutive month, there is a decline in consumers’ assessment of current job availability, contributing to the lower score and offset by stronger expectations for future business conditions.

Falling FICOs

A big question, of course, is how many consumers will qualify for the best loan rates this Autumn, or whether lower credit scores will discourage them.

As the CU Daily reported here, credit scores continue to fall at the fastest pace since the Great Recession as Americans struggle to keep up with the high cost of living and the return of student debt payments, according to a new report.

The national average FICO score dropped by two points this year, the most since 2009, according to data released by FICO.

Although credit scores remain significantly higher than during the Great Recession, they are down for the second year in a row.

Changes in the Ag Market

Most consumers may only know farming from their annual visit to the pumpkin patch, but credit unions that serve agricultural markets traditionally experience seasonal lending activity in the fall as farmers bring in crops and repay operating loans, while preparing for the next planting cycle. But that rhythm could be upset as traditional foreign buyers of U.S. crops look to other sources in response to tariffs.

Auto Prices Increase

As reported here, in the largest gain in more than two years, new-vehicle prices moved higher in August as more model year 2026 vehicles hit dealer lots and automakers looked for ways to offset higher costs, while EV sales hit a record during the month, according to new estimates from Kelley Blue Book.

Kelley Blue Book reported that price increases accelerated in August as both key measures – average transaction price (ATP) and manufacturer’s suggested retail price (MSRP) – increased month over month and year over year. Despite higher prices, retail sales in August climbed by 2.5% versus year-ago levels.

The Q4 Forecast

The U.S. economic outlook for Q4 2025 is one of slowing growth and potential moderation, with forecasts indicating lower real GDP expansion and a possible increase in the unemployment rate.

While some sources project continued growth, like the New York Fed’s Nowcast at 2.2%, others, such as Deloitte, anticipate an entry into recession in Q4 2025, leading to significant GDP declines in 2026. Factors such as rising input costs, moderating consumer demand, and potential geopolitical shifts are key areas to watch, analysts say.

When it comes to inflation, Fannie Mae most recently forecast a slight uptick to 3.3% for 2025.

Leave-ing Nothing to Chance

Some credit unions have already launched their Autumn-related promotions.

In Maine, the $110-million Brewer FCU has introduced its “Autumn Advantage Loan.”

“The days are getting cooler and the leaves are starting to change,” the credit union said.

At Brewer FCU, we know that the fall months are a special time of year and we want you to enjoy them! With our Autumn Advantage loan, you’ll be ready!”

The Autumn Advantage Loan offers:

- Amounts up to $10,000

- A fixed rate as low as 7.99% APR

- Loan terms up to 36 months

In New Jersey, the $111-million Deepwater Industries FCU is promoting its “Pumpkin-Perfect Rates.”

“This season, Deepwater Industries FCU is excited to offer fall loan deals that will make you want to cozy up with savings,” the credit union said. “Whether you’re in the market for a new car, planning a home renovation, or looking to consolidate debt, our competitive rates will help you make the most of your financial journey.”