NEW YORK–After more than a year of tight lending and higher interest rates, there are some early signs that access to credit might be loosening, a new analysis suggests.

In particular, mortgage refinancing saw a big move last month, giving potential borrowers a reason to reengage, Benzinga reported.

The report pointed out that rejection rates dropped to 15% in June, down from 42% in February. The February figure was the highest on record going back to 2013. Auto loan rejections were also down, falling to 7% in June from 14% earlier in the year.

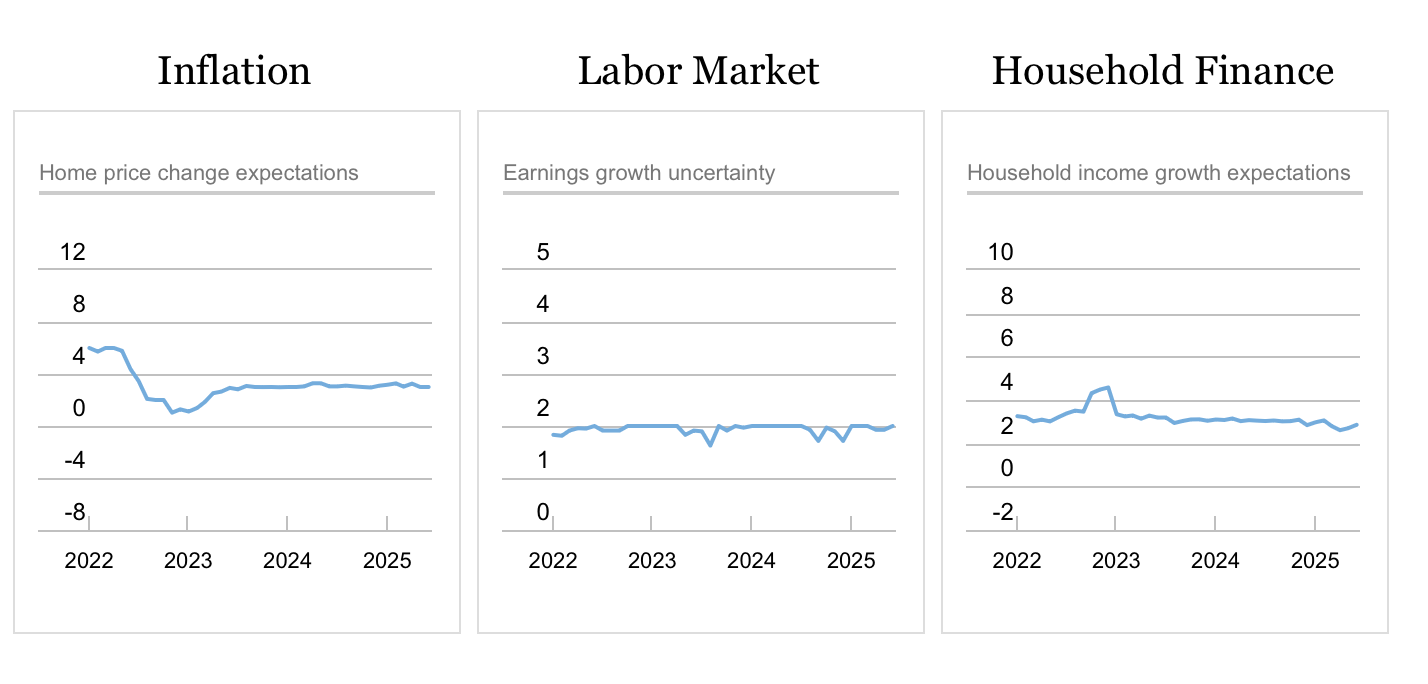

In addition, data from the Fed’s Survey of Consumer Expectations, which tracks how households feel about credit access, inflation, and their financial outlook, Reuters reported.

“Fewer people reported holding back from applying for credit because they expected to be turned down,” the report stated. “That share, often referred to as discouraged borrowers, dropped from 8.5% in February to 7.2% in June.

Overall Debt Burdens a Concern

“At the same time, people said they’d be more likely to face a surprise $2,000 expense, but also felt more capable of covering it,” the report continued. “Overall debt burdens remain a concern in other parts of the Fed’s data, but consumer financial conditions still look relatively stable, especially given the impact of elevated interest rates.”

Analysts are now waiting for the June report from the Fed to determine if the trend lines are continuing.