AUSTIN, Texas— Credit unions are entering 2026 with a far more execution-focused agenda than the broader banking industry, according to a new report that examines the retail banking trends and priorities that are likely to shape the financial services industry this year and that also identifies what sets apart the 7% who reach their transformation goals apart from the 93% who don’t

Q2’s 2026 Retail Banking Trends & Priorities found that when financial institution executives compare 2025 to their expectations for 2026, the contrast shows an industry shifting from defensive stances to offensive strategies.

“The data tells a story of organizations that spent the past year fighting competitive threats, only to realize the real victory comes through internal transformation and technological progress,” the analysis, authored by Jim Marous, publisher of The Financial Brand, states in the preface to the report.

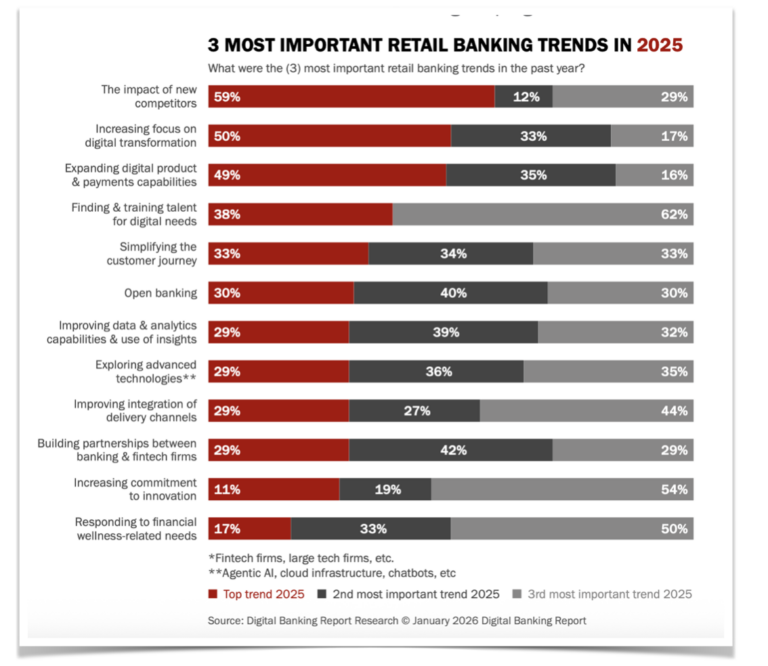

According to Q2, the most notable change for this year uncovered in its research is the sharp decline in concern about new competitors. In 2025, 59% of institutions viewed the impact of fintech firms, big tech players, and digital-first challengers as their top trend. By 2026, this concern drops to just 17%.

“This isn’t complacency. It’s evolution,” the report states. “Banks and credit unions have learned an important lesson: you can’t outperform competitors solely by obsessing over them. Instead, developing technological skills provides much better protection against disruption than always trying to catch up.”

‘Energizing Finding’

Q2 said that what is perhaps the most encouraging finding is the rise in prioritizing advanced technologies, from 29% in 2025 to leading at 49% in 2026.

“This signals a fundamental shift in mindset from viewing emerging tech as experimental to considering it essential.

After years of pilot programs and cautious exploration of AI, institutions are now ready to fully commit,” Q2 said. “The difference between experimenting with advanced technologies and deploying them at scale will separate winners from also-rans.”

The report’s analysis added that this growing confidence is backed by a significant increase in the focus on innovation, jumping from 28% to 40% as a top priority.”

The Credit Union Marketplace Differentiation

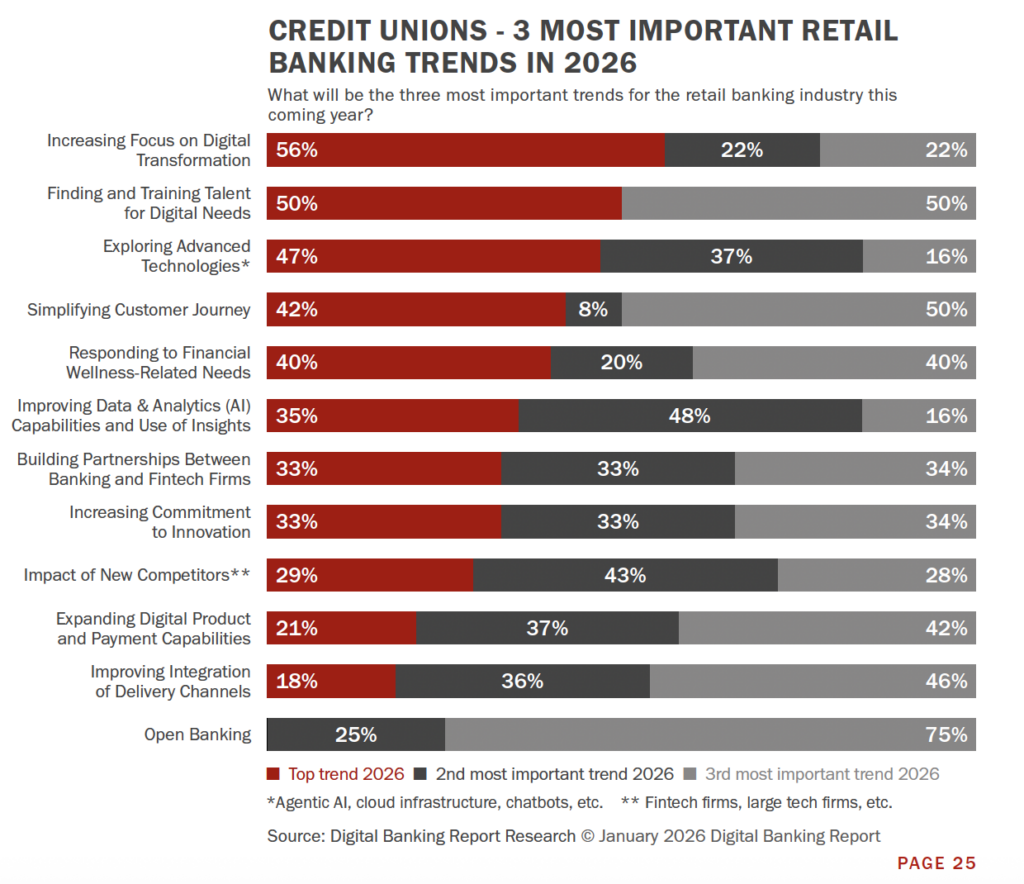

In looking specifically to credit unions, Q2 said the industry is entering 2026 with a “far more execution-focused agenda than the broader banking industry.

“For credit unions, digital transformation ranks as the top priority, cited by 56% of respondents, compared to 46% across banks and credit unions overall,” the report survey said. “Talent development is nearly as critical, with 50% of credit unions ranking finding and training digital talent as a top trend, compared to just 9% in the broader industry.

“Think about that gap for a second. The industry keeps piling on technology initiatives, while credit unions recognize they don’t have the people to execute it,” the analysis continued.

The report found credit unions also demonstrate greater customer focus, with 42% of those surveyed prioritizing simplified journeys compared to 35% overall, and 40% emphasizing financial wellness versus just 25% industry-wide.

“Interestingly, open banking ranks dead last for credit unions, with no responding organization seeing it as a top priority (75% put it third), compared with 12% of the industry overall viewing it as critical,” Q2 stated. “Is it possible that credit unions are underestimating the competitive threat from embedded finance players?”

Credit Union Priorities for 2026

Q2 said credit unions’ 2026 strategic priorities reinforce what the company has observed in the trends data, which is that credit union are focused on execution rather than experimentation.

Among the findings:

- Updating legacy operating systems remains a top priority for 56% of credit unions, compared to only 42% across banks and credit unions overall, underscoring the continued focus on modernization in CU agendas.

- Additionally, credit unions are more proactive in pursuing fintech partnerships, with 50% citing them as a top priority, compared with 29% overall, indicating that credit unions recognize they need outside help to compete.

A ‘Contradiction’

“There is a contradiction when we look at credit union trends versus the strategic priorities mentioned,” Q2 stated. “While 50% of credit unions ranked finding and training talent as a top trend compared to 9% across all institutions, only 10% of credit unions make recruiting and retaining talent a top priority, compared to 20% for the industry overall.”

What finished “dead last” among credit unions in terms of priorities? “Building an innovation culture,” the Q2 survey found. Just 13% of credit unions listed an innovation culture as a priority, compared with 24% overall, “suggesting that most credit unions would rather buy or partner for innovative solutions rather than build internal capabilities. Time will tell if this is a solid decision or a long-term strategic mistake,” the analysis stated.

State of Digital Transformation Progress

Q2 said that as it looked at the state of digital transformation for credit unions compared to the overall industry, the differences are relatively modest, ranging from three to eight percentage points.

“The real story is that credit unions stated that digital transformation is their top priority at 56% versus 46% industry-wide, yet a combined 60% are either in early stages or have no clear goals and measures,” the report states. “That’s the same pattern we see across the entire industry.”

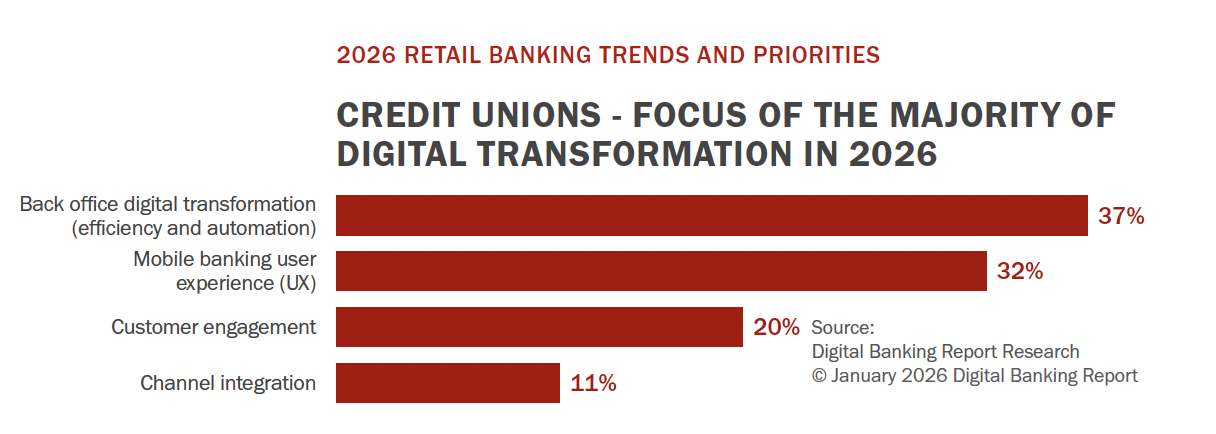

In general, where credit unions see challenges aligns with other industries, the report states. But when the focus is on digital transformation efforts, the Q2 analysis found credit unions are far more concentrated on back-office digital transformation than the industry as a whole, with 37% of credit unions stating that efficiency and automation will be the primary focus of their efforts in 2026, compared to 33% across the broader industry.

Credit unions also place a noticeably heavier emphasis on mobile banking UX, the survey found.

‘Significant Divergence’

“The most significant divergence appears in customer engagement, where only 20% of credit unions cite engagement as their primary focus, compared to 25% industry-wide,” according to Q2. “That gap mirrors our findings, in which banks placed greater emphasis on advanced technologies, analytics, and engagement-driven growth. In other words, banks are using transformation to deepen relationships and scale insight, while credit unions are using it to stabilize operations and improve core digital experiences.”

Additional Analysis

Other subjects examined in the report:

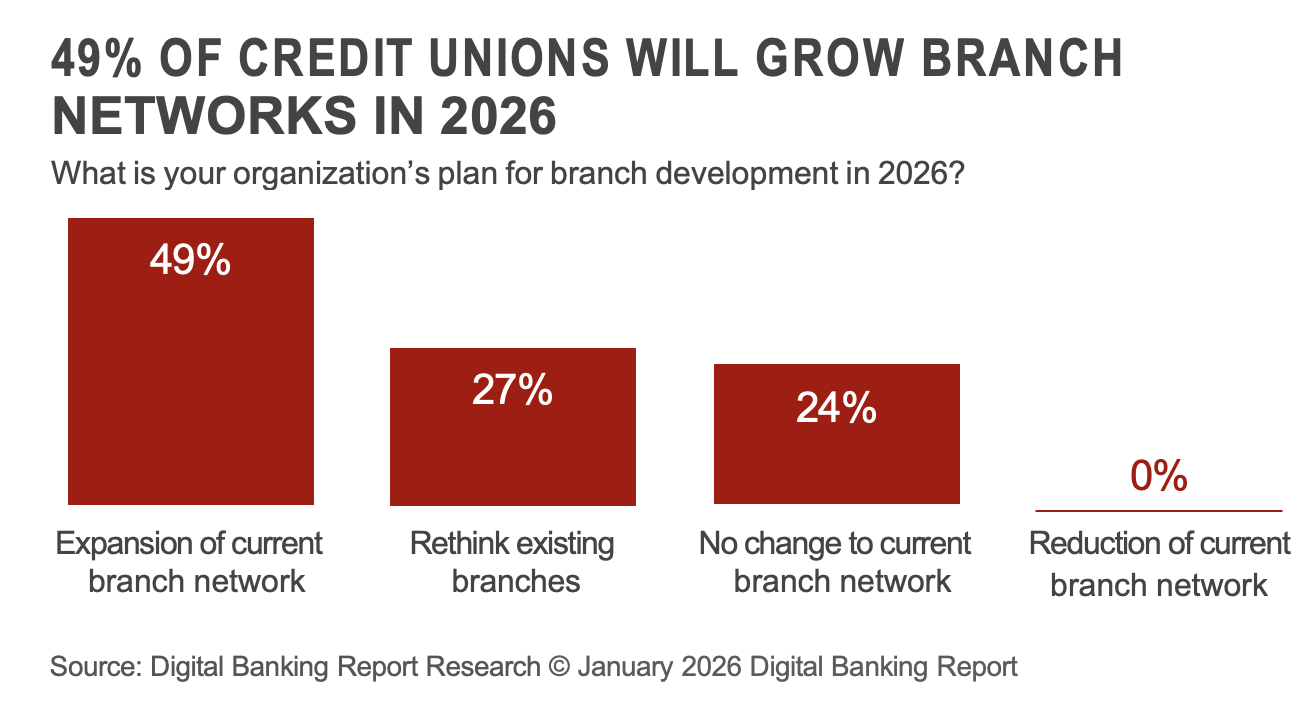

Branch Strategies for 2026

The biggest contradiction for the banking industry overall, especially for credit unions, is that credit unions prioritize digital transformation at 56% compared to 46% industry-wide, yet 49% of credit unions plan to expand their branch networks in 2026, compared to just 42% of the broader industry, Q2 stated in its analysis.

“What’s even more notable is that NO credit unions are reducing branches, while 6% of the overall industry is actually closing locations. Are credit unions trying to win on every front simultaneously?” the report asks. “They are expanding branches, upgrading technology, partnering with fintechs, fixing back office systems, and improving mobile UX.

Could this be a strategic decision for the future, where footprint expansion leads to market share growth?”

Deposit Acquisition Strategies

Credit unions are far more aggressive in using data and analytics tactically, with 67% targeting special deposit offers to existing members and 57% targeting prospects, compared to 56% and 46% across the broader industry, respectively, the survey found.

“This reflects a practical use of data to drive near-term growth. Credit unions also rely more heavily on rate-driven and product-led tactics, with 45% creating new short-term deposit products and 35% paying higher marketplace rates, versus 38% and 26% overall,” the analysis states. “ Unfortunately, the data-led strategies are not reflected in the generation of deposits from small businesses, as only 33% of credit unions report building small-business

deposit strategies, compared to 48% overall. What exactly are the new branches for if not relationship-based business banking?”

Building Third-Party Partnerships

Q2 said it found responses to its questions about third-party solution providers clearly show how differently credit unions are approaching transformation compared to the broader industry. The use of collaborations also aligns with the trends data collected.

Credit unions overwhelmingly prioritize ecosystem integration, with 60% ranking fintech ecosystem integration as a top partnership priority, compared to just 29% at banks and credit unions overall, the report stated.

“That gap reflects the structural reality that credit unions are using partners to compensate for core limitations and to accelerate execution … not to layer on incremental capabilities,” according to the analysis. “The same pattern appears in the development of unified digital banking platforms, where 54% of credit unions cite it as a top priority, compared with 45% overall, reinforcing the emphasis on consolidation and simplification rather than modular experimentation.”

Positioning for the Future

Q2 said it found the credit union sector is much more resilient and adaptable than it’s often perceived.

“Our research indicates that many leadership teams are willing to embrace change, take calculated risks, and make difficult investment decisions across technology, partnerships, talent, and physical presence, demonstrating this resilience,” Q2 reported.

Conclusion: A Leadership Crisis, Not a Capability Gap

The Q2 report states that overall, the banking industry stands at an inflection point that it hasn’t fully recognized.

“For the first time in decades, the tools required for genuine transformation are democratized, affordable, and proven. AI capabilities are available from dozens of providers to financial institutions of all sizes.”

It added that the “opportunities are also clearer than ever.”

“The shift from viewing competitors as threats to focusing on internal capabilities represents genuine strategic maturity. The rise in the prioritization of advanced technology from 29% to 49% signals readiness to move beyond pilot programs,” the analysis states. “The 67% already engaged in fintech partnerships have access to innovation that would have required hundreds of millions in R&D investment just five years ago.

It Takes ‘Courage’

What sets the 7% who reach their transformation goals apart from the 93% who don’t isn’t budget size or market position, according to the Q2 report.

“It’s decision-making courage,” the analysis states. “The winners stop expanding branches when digital is the main focus. They shift partnership strategies from parity to differentiation. They use AI where customers can see the impact, not just where internal metrics improve. They align infrastructure investments with their strategic priorities instead of taking the easy route.”