KENNEWICK, Wash.–What are being called “spicier results” have been relesed from a second survey of the CEOs of credit unions of less than $100 million in assets, with the results offering insights into how CU leaders view the exam process, what keeps them in the job, and how some CUs are “hovering over them like vultures.”

The survey was conducted by Endangered Small CU Defense, which said it sought to dig a little deeper into some of the findings from the previous survey, according to Doug Wadsworth, who heads the organization and who is CEO of Tri-Cities Community Credit Union in Kennewick, Wash.

The CU Daily had coverage of the initial survey here.

The Findings

According to Wadsworth, some of the findings include:

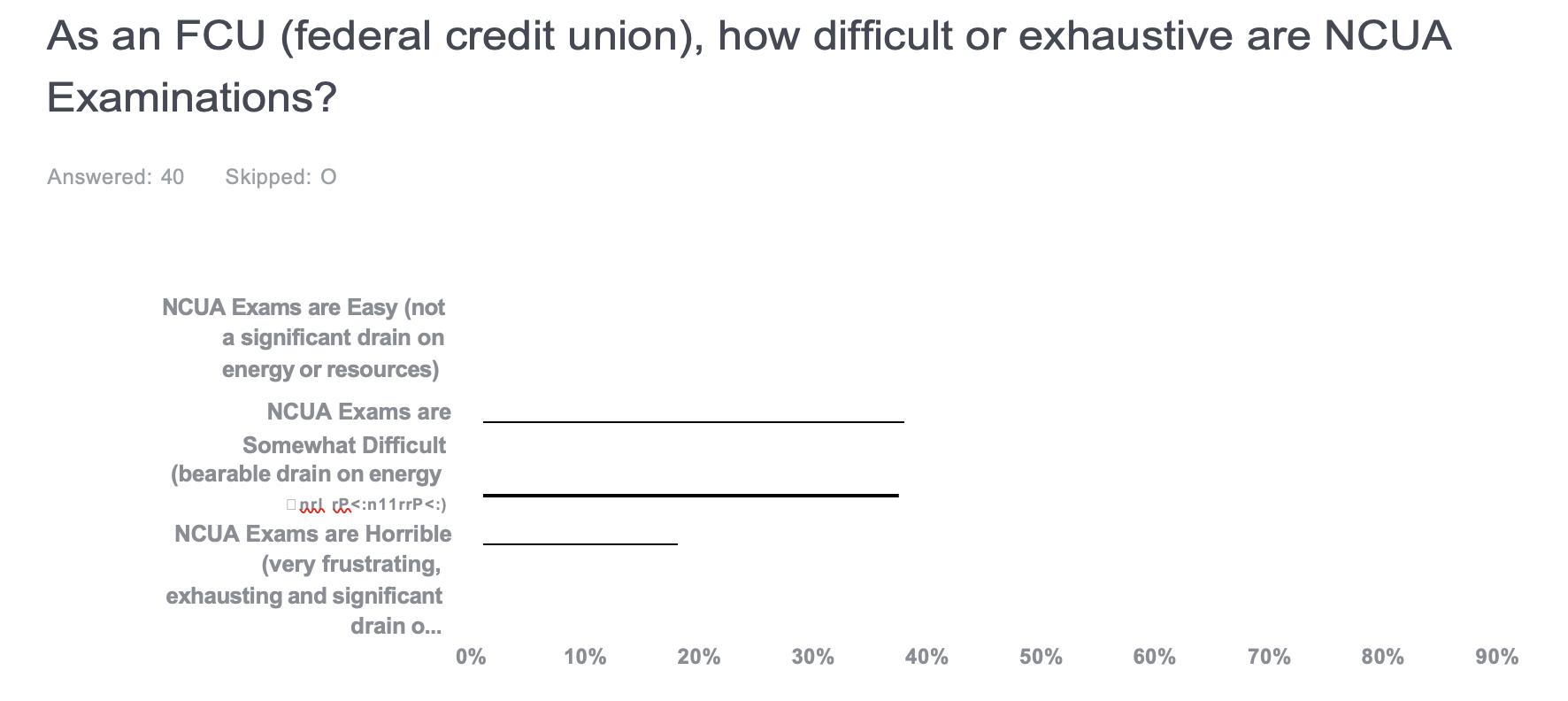

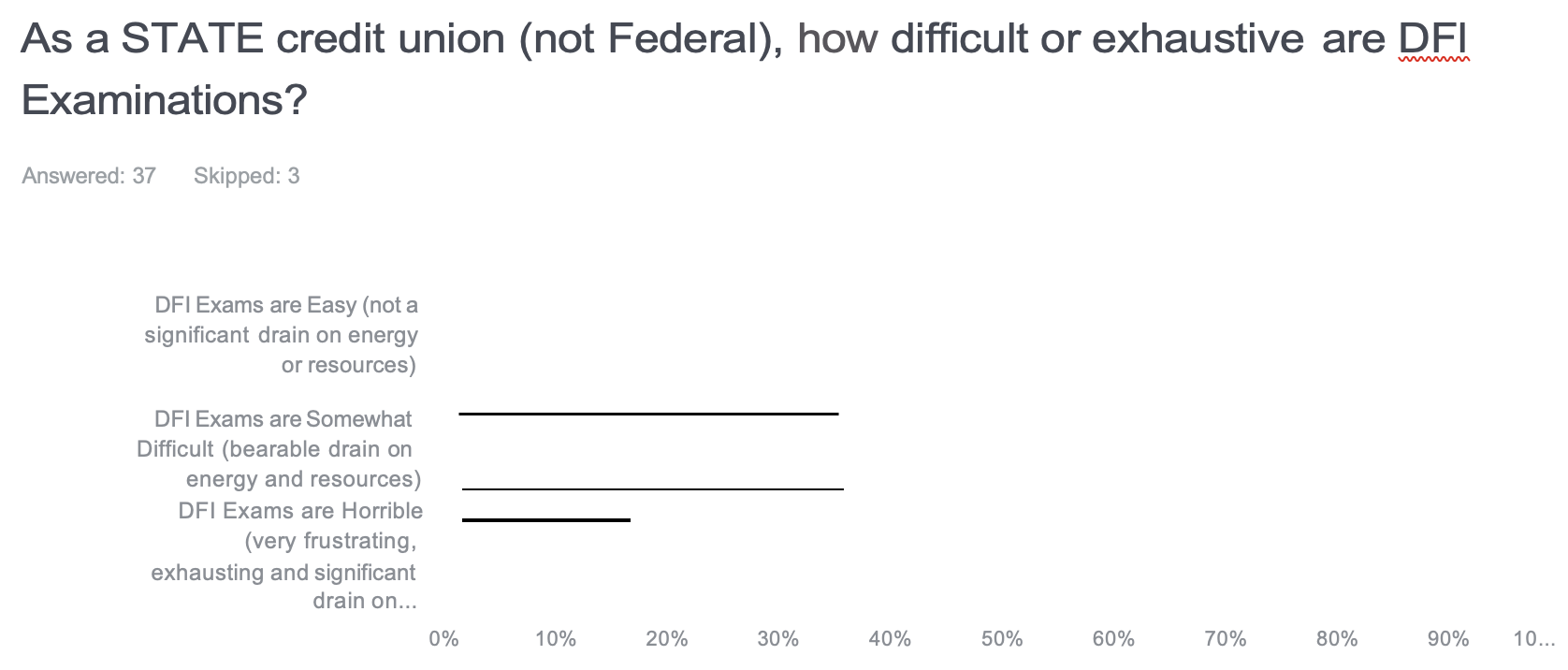

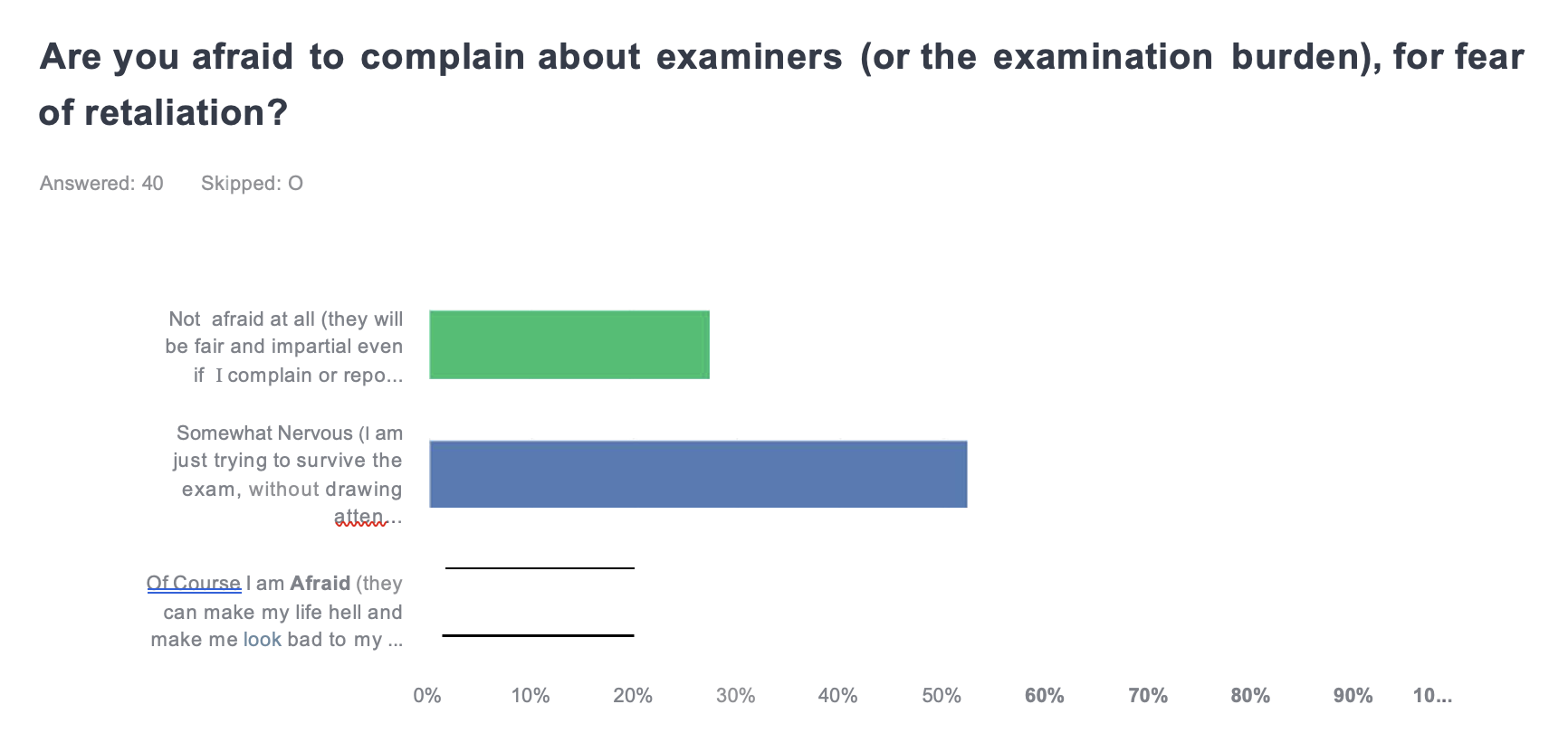

Examinations

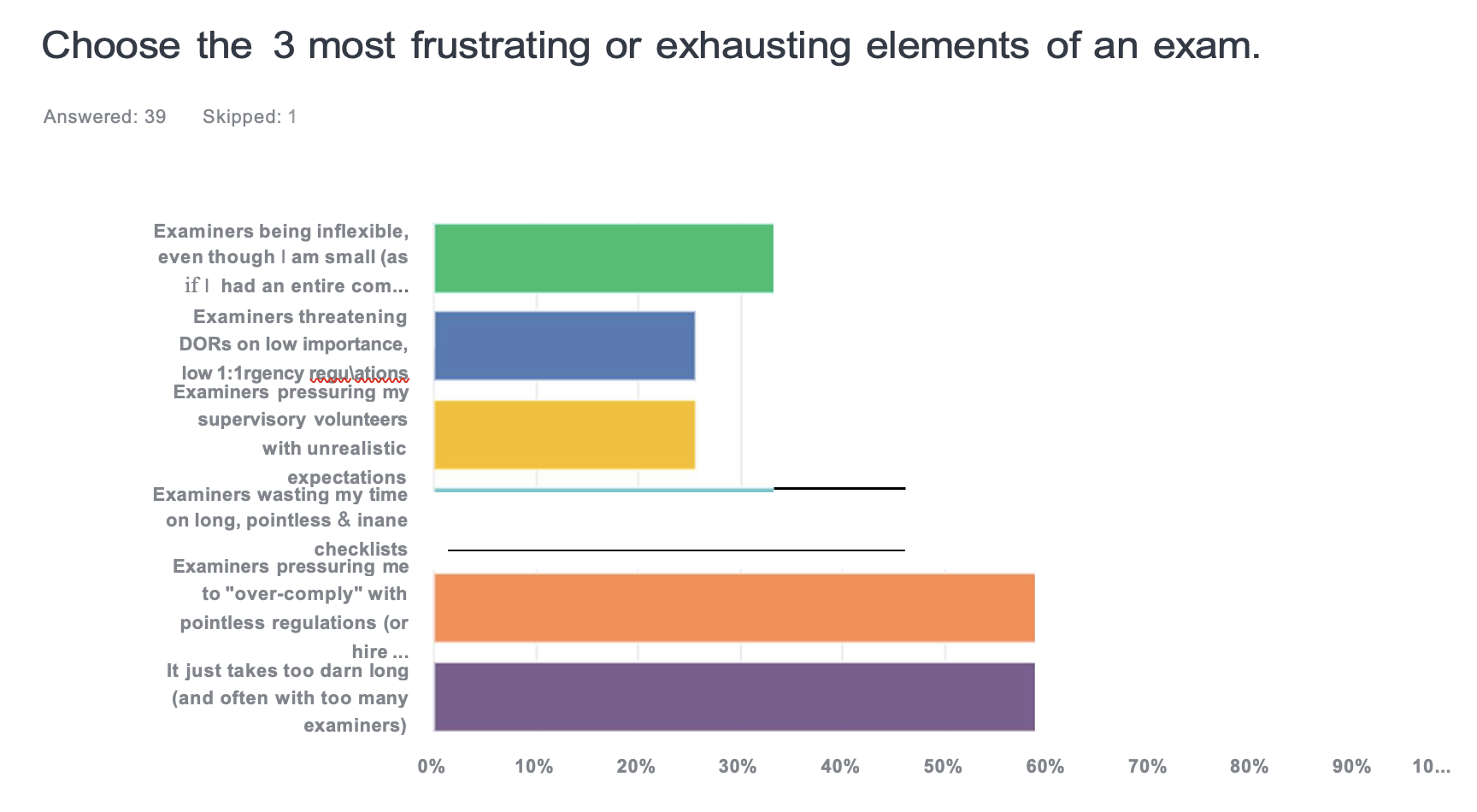

“First, CEOs seem to think that exams (whether DFI or NCUA), are equivalently difficult, nearly 20% think they are “horribly frustrating and exhausting,” while nobody finds them easy,” said Wadsworth. “What do CEOs find most frustrating and exhausting about these examinations? The length of the exam (way too long and exhausting), dealing with ‘over-compliance’ pressure, and then (further down) the wasted time dealing with long and pointless checklists (unrelated to safety or soundness). As far as ‘fear of retaliation,’ it is pretty mixed. Some are very afraid of examiner retaliation, but 50% are in the middle (that is, just keep your head down and get through it as quickly as possible, without making waves).”

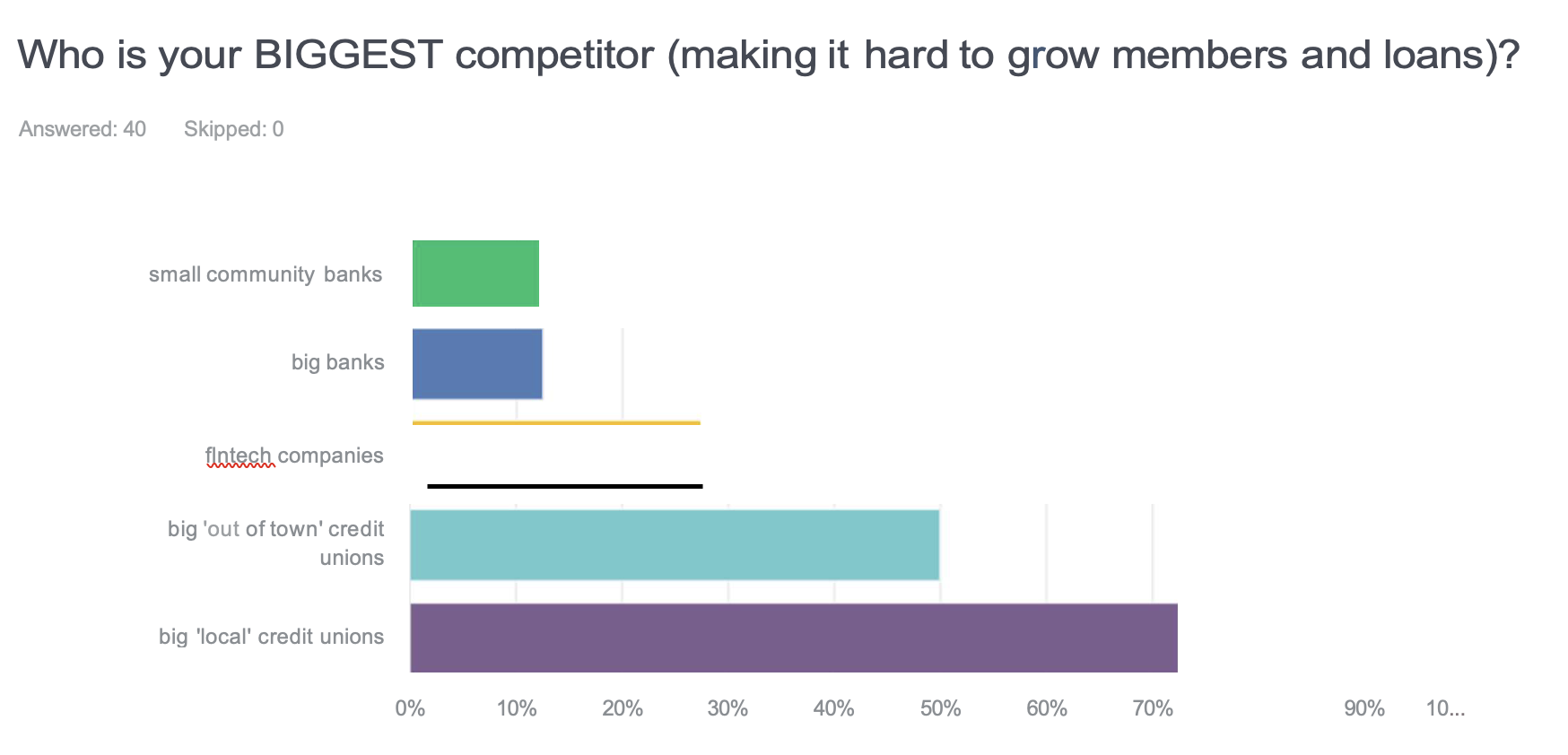

Competition (Cooperation?)

When it comes to the competitive marketplace, Wadsworth said the survey shows most small CUs consider big local CUs as their primary competitor, followed by big “out-of-town” CUs, and then fintechs.

What about banks? Those are at the bottom of the list, the survey found.

“As probably seems natural, they consider big CUs to be a “mixed bag” – some are very aggressive, some seem ‘fine’ and leave them alone,” Wadsworth said. “It should be noted that four small CU CEOs felt like big CUs were ‘hovering over them like vultures,’ trying to drive them out of business or merge them.”

In addition, the survey found 40% of the respondent were alarmed at the large numbers of “out-of-town” big CUs that had recently moved into their communities, increasing competitive pressure.

Competitive Advantage

What do these CEOs consider their “primary strengths” to be (how are they better than their big competitors)?

Wadsworth said that topping the list was “approving loans that would get denied elsewhere, and providing better helpful, personal and friendly service.”

The Incentive

That was followed by “offering better loan rates and lower fees.”

Wadsworth said that when the survey probed into what motivates these small CU CEOs, it found the answer wasn’t money or that their small CU job was a stepping-stone, except for what he called, “one honest respondent.”

“These managers overwhelmingly love making a difference for people that need it,” said Wadsworth. “They love cooperatives, and they love the challenge of wearing lots of hats.”

How to Improve the Job

Lastly, what do these CEOs wish they could change about their job, to make it better?

According to Wadsworth, “Primarily, they want help with complex regulations, hence the need for regulatory relief, followed by needing more reliable or skilled employees–yep, that’s expensive for tiny CUs.” The third highest ranking response was wishing big CUs would stop trying to take their members and loans, with 50% of those surveyed choosing this as a very high priority,

So, Now What?

Wadsworth said that the survey shows that “Clearly, it would be very helpful if examiners eased up on over-compliance pressure and exhaustive pointless checklists, while making more of an effort to be flexible with small CUs (and ensuring those CEOs feel safe from retaliation).”

“I know that both NCUA and Washington DFI have been making progress already, which we applaud,” Wadsworth said. “Perhaps some of these respondents are suffering PTSD from prior years.”

In addition, Wadsworth said it appears there are probably some “bad actor” big credit unions in the market, and the competitive pressure they are putting on the dwindling number of small CUs is a concern.

‘What Can We Do?

“What can we do about that?” asked Wadsworth. “Who is going to tell some of these big guys to ease up and leave little ones alone–to stop punching down) Perhaps peer pressure from the industry would help, a culture that values the few remaining small CUs, and helps ensure they survive and thrive?”

Wadsworth said it appears the CEOs of smaller credit unions are a “different breed” who have really “drank the cooperative Kool-Aid.”

And what might that imply?

“Perhaps the dwindling number of surviving small CUs will be more resistant to mergers?” he said. “Let’s hope so, because if small CUs are allowed to go extinct, I can’t imagine the movement’s tax exemption would endure much longer. Our Endangered Small CU Defense calls on leagues and associations across the nation, to consider these findings, and make the changes needed. Together we can help ensure our entire movements stays healthy and strong – whether big or small.”