Editor’s Note: The author has requested anonymity but is known to the CU Daily.

By Anonymous

This is my favorite part of my quarterly musings, sharing what I see and hear from others. This quarter, I’m going to share tales from your community banking relatives – the ones who manage to prosper despite the burden of federal income taxes (and don’t take that as a dig on credit unions – it should be a tale of what others are able to overcome).

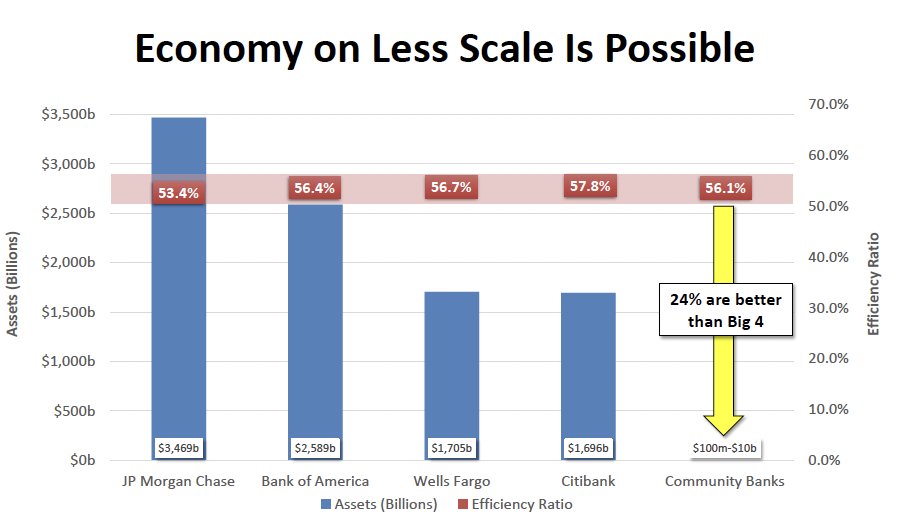

First stop is debunking the “chasing scale” message that credit unions are being fed like the dystopian future portrayed in the 1984 Apple commercial introducing the Macintosh computer (i.e., scale or die). The four largest banks in the US are JP Morgan/Chase, Bank of America, Citi, and Wells Fargo. Each has assets equal to or larger than the sum of all credit unions. The efficiency ratio of each of these banks ranges from 54% to 56% (a tight band, no outliers).

Better Ratios

There are just over 2,700 community banks with assets between $100 million and $1 billion. Of that group, 22% have an efficiency ratio better than the largest four banks. Do you think they wake up every morning and say, “We need to reach $10 billion in assets or else we won’t be here in 10 years?” Of course not. They wake up and ask the question, “What should we do to stay relevant to our customers and how can we serve them in a cost effective manner?”

This cohort of community banks sounds more like credit unions – they are scrappy and won’t bow to the largest competitors – rather, they welcome an alley fight on their turf, where they know the needs of their customers (members) better than someone from afar.

Some Context

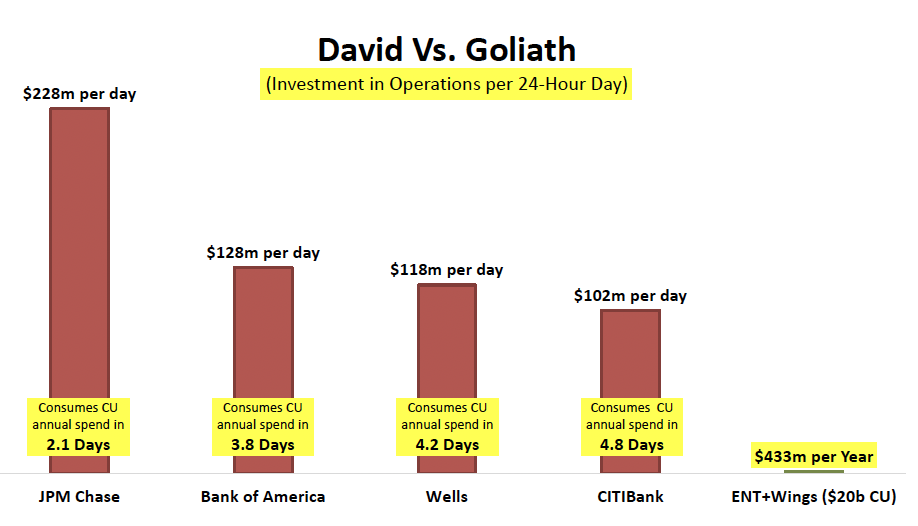

For context, ENT Credit Union (Colorado) and Wings Financial Credit Union (Minnesota) recently announced a merger that will make them a $20 billion credit union. JP Morgan/Chase (the largest of the big four) will surpass the annual spend of ENT + Wings in 2.1 days, while Citi (the smallest of the big four) will surpass their annual spend in 4.8 days. The lesson? At $20 billion you are still a small player. Focus on making money; profitable organizations don’t fail.

Second stop, ROGER Bank. This is a bank with a singular mission to serve military members and protect them from being preyed upon (ahem …. you know who you are). It was started by an existing bank CEO–Jill Castilla, Citizens Bank of Edmond, Oklahoma–who served in the military, and both of her children do as well. They have grown the bank to $56 million in assets in a short time with – wait for it – one FTE. Who says you can’t make a de novo work? It’s more about conviction, courage, and a thoughtful business model more than anything else – the American way.

Worth a Listen

Last stop, two great podcasts. The first builds on the de novo theme. It’s an interview with Lori Maley, who is the CEO of Bank of Bird in Hand (established 2013), and Keith Costello, who is the CEO of Locality Bank (established 2022). Here is what struck me on my 40-mile bike ride while listening to them–they started with zero scale. Last place. Zippo. Nada. Yet, they managed to build profitable enterprises without worrying about scale. If we serve our communities better than anyone can, the market will demand we get bigger.

The next podcast I want to share is Proven Strategies to Help Community Banks Win Against Larger Competitors. Caleb Stevens of SouthState Bank discusses the role marketing plays in community banking and how the roles of marketing and sales can work to stay competitive.

As an aside, Caleb is in his early 30’s but when you listen to him, he sounds like a seasoned veteran – not his voice, but rather his experience, context, and perspective. As a community sized credit union (which all of you are) there is no excuse for not giving this a listen.

I realize my tone is firm and direct. There are plenty of success stories out there – they just don’t make the news like the flameouts do.