LAS VEGAS–A diverse group of credit union leaders is sharing thoughts, strategies, predictions and more on everything from mergers to fintech partnerships to the love of technology and more.

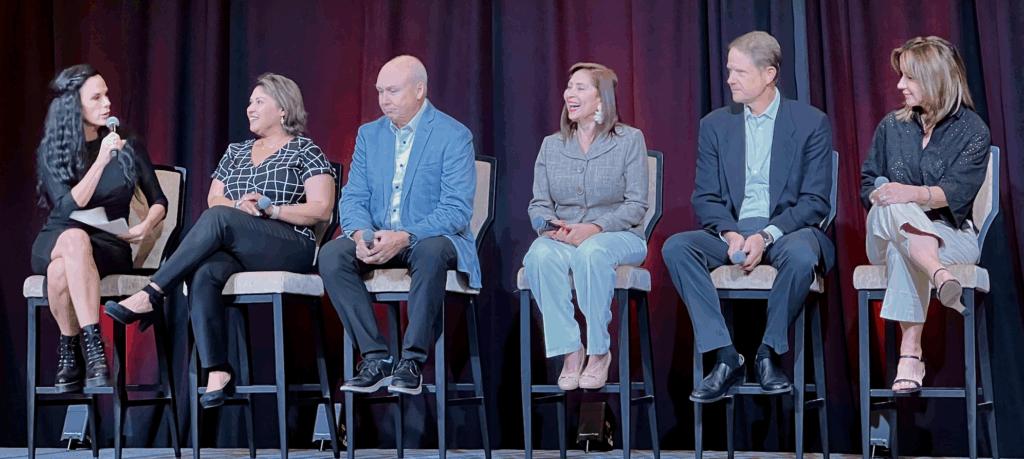

The insights were shared during a session titled “Unlocking the Ecosystem” at an Underground Collision meeting here hosted by Mitchell Stankovic Associates.

The session was moderated by Dr. Brandi Stankovic. Participating as panelists:

• Caroline Willard, president and CEO of the Cornerstone League

• Keith Sultemeier, president and CEO of Kinecta FCU

• Maria Martinez, president and CEO of Border FCU

• Nick Evens, president and CEO of Curql Collective

• Shazia Manus, chief data and analytics officer of TruStage

Here’s a look at some of what was discussed.

Stankovic: Why are these various associations within credit unions crucial?

Martinez: When you put a program out there, it’s because there is a need. One thing we saw in our industry was that when we went to conferences, there was a need for a discussion around issues affecting the Hispanic community. That was how the National Association of Latino Credit Unions and Professionals was formed. The same thing is true with the Credit Union Women’s Leadership Alliance. We saw the need for a safe place and for small credit unions.

One of the things we sometimes get asked is why there aren’t any men in the club. It’s not a club; it’s an association. But the reason is we were looking for a safe space. Yes, you may be small or big, but you know when people come to your credit union, they are looking for that initiative, for financial wellness.

Stankovic: Should we all merge, or do small CUs play a role?

Martinez: The mergers are going to happen. We’ve looked at merging, to be honest. But you have to be really careful. When you are looking for another credit union to merge into, or to merge into you, you have to look at the culture. One of the main reasons we didn’t merge is because the culture was not going to be there. You have to look out for your members. We have programs I know would go away if we merged.

Stankovic: You have worked at a credit union, a league, business partners. Why is that ecosystem important?

Willard: We are focused the most on advocacy. We are in five states that represent about 70 congressional seats. There will be a threat a lot of times that bubbles up at the state level where they are testing strategies. We had interchange bills in four of our states. I’m proud we were able to swat those down. We have to have intel at the state level to be more effective at the national level.

Stankovic: Are we polarized or coming together or both?

Willard: I’m seeing evidence of both. We are very much trying to lock arms. We are not a big enough industry to be separate. On advocacy, we have to have consistent messages on Capitol Hill; otherwise, it’s confusing to lawmakers and they don’t know what we want. We have to get over our own egos and be willing to collaborate.

Evens: The perfect example is stablecoin. We are of the opinion that if this entire industry doesn’t stay together on this one thing, we will not have the scale to compete. The Fed is doing more to allow fintechs to do more behind the scenes to offer stablecoins. If we don’t create scale on that one thing, we will be in trouble.

Stankovic: Why are our business partners and leagues and associations so important?

Sultemeier: It’s definitely true our long-term superpower has been collaboration. I do see some erosion in that, but we need to get over it. At the end of the day, we’re not competing with each other; we’re competing with the big FIs and the newcomers.

Because we individually lack scale, we tend to group together, and initially that was through leagues. That allowed us to punch above our weight class. We are a helluva lot stronger when together. And where we can’t do it ourselves, we form CUSOs. We have done that as an industry time and time again, and I sincerely hope we continue to do it.

It’s not sexy, but there are two big players in the mortgage servicing area and nobody likes them, but we all exclusively use them. Why can’t we do this ourselves?

In mergers, we are seeing larger institutions getting together more and more. Hopefully, the consolidation of the industry, which will continue to happen, doesn’t change the cooperation in the industry.

Q: You have gone out to the fintech arena and are introducing them to credit unions. What have been your standards for working with CUs?

Evens: You must care about the future of the credit union industry, and more importantly, taking care of the members. We have a dual-sided value prop: to serve our investors and fintechs. One thing we’re trying to do is make them more ready to come into a credit union and operate quickly, rather than draw down the resources of a credit union by taking forever to implement, for example.

There is an assumption that we are a venture capital firm. We are strategic investors. A VC will say, “Here is some money, take it and run, grow, and come see us in three years when you can return our money 10x.”

In our case, if a fintech exits the market, we lose a partner. We don’t want that. We call it “buy to die.” We aren’t investing to see them exit and see technology shelved. An example is Amount, which was just sold to FIS. We are keeping an eye on that.

We have a 10-year life, so that at the end of 10 years we might have four or six fintechs doing business. Hopefully, we can contribute a super-CUSO and distribute those shares, and they are still alive and thriving. We are looking at the afterlife for these fintechs after 10 years for how they can continue to serve the credit union industry.

We are looking today for the credit unions that can disintermediate the mortgage companies that are not serving our credit unions well. We’re looking for quicker technology to replace the legacy systems that are driving us crazy every day. We are meeting with Fiserv here at Money 20/20 about what the future looks like when you buy a company.

Stankovic: How does technology and analytics play a role in all that?

Manus: Never fall in love with technology. We don’t know what’s coming next. What is that tech there to solve for? Data is sort of like the blood flow. The question is how do you use the data to drive business outcomes and decisions quickly? The reality is because of exponential development, the ability is there to leapfrog the legacy systems. But it goes with a mindset. How do we connect the data? What data is needed? You need to know what data is valuable.

The member is the consumer. So, who is the recipient of this problem you are solving for? If not the member, you are wasting time.

Stankovic: You serve a unique demographic. How did that come about?

Martinez: One of the things that happens with credit unions is we get too complacent; we say our member is always going to be our member.

When you analyze your data, you find out they are using some of the neobanks we didn’t think they would use. And I’m talking about an underserved community. Why are they using Chime? There must be a reason. There must be needs not being met. We look at our ACH transactions and where they are going. We look at where they are spending their money. Our members are using technology we thought they would never use. We sometimes use legacy systems as an excuse.

Stankovic: Is there a similar need to fill a demographic type at the association level?

Willard: We have about 400 credit unions under $100 million in assets out of our 600-plus credit unions. We do need to serve those folks very, very well. What they need is so different from what a large credit union needs. Sometimes they surprise me and are progressive and embrace technology quickly.

Stankovic: How are you turning your tech and data into action in your CU?

Sultemeier: I’m very happy with our data capabilities. We have a sophisticated BI group. What we don’t have in our organization is a high degree of data literacy in our staff. They are not yet there. They don’t yet understand how they can leverage data to be more effective for members in their jobs. I think there is some reluctance to use it, to be frank, because they think this is going to replace them.

I underestimated the discomfort there, but it’s going to happen. The future worker is going to leverage these tools, whether here or somewhere else. Let us upskill you. We are willing to make the investment in you. We are not looking to replace you; we are looking to make you better. And it’s still a challenge.

Stankovic: You have brought fintechs to a grander audience. What about fintech literacy at credit unions?

Evens: A lot of times credit unions just don’t have the bandwidth or skill sets to evaluate a lot of this technology coming at them. That’s where we see our role. We are an R&D shop, a technology finder. The gist of it is we can fill that role and at least present it to the credit unions and say this is a really good solution and you should take a look at it.

Stankovic: Give us an action item takeaway or a challenge. What should I dedicate the rest of the year to making happen?

Manus: A system is only a system if there is trust and standards and scale to go toward a common direction. No one player can tackle this. I think we need the ecosystem to come together—fintech along with the scale provider—and we all have a role to play.

Evens: Don’t try to go it alone. The technology being brought to the forefront is transformative and you need to start looking at it. Stablecoin is really going to change the way money moves.

Martinez: Sometimes it can be something simple. We implemented a program with a QR code to call the call center or go into a chatroom with AI. When we implemented that program, our calls started coming up and we were taking care of them through the AI chat.

Sultemeier: My piece of advice is for potential partners or existing partners looking for the next piece of business: Do not write checks in the sales process that you cannot cash during implementation. Don’t make me feel like the prettiest girl at the dance and then ghost me. This ecosystem is very tight; we talk to each other. If you do a great job for one CU or do not do a great job for one, others are going to hear about it. You have to pay constant attention. We need constant care and feeding.

Willard: There is a history of collaboration in our movement. I think we’re looking for that next big thing—not the shiny object, but something that will propel our movement forward. Maybe it’s stablecoin. We are better when we collaborate and aggregate our buying power.