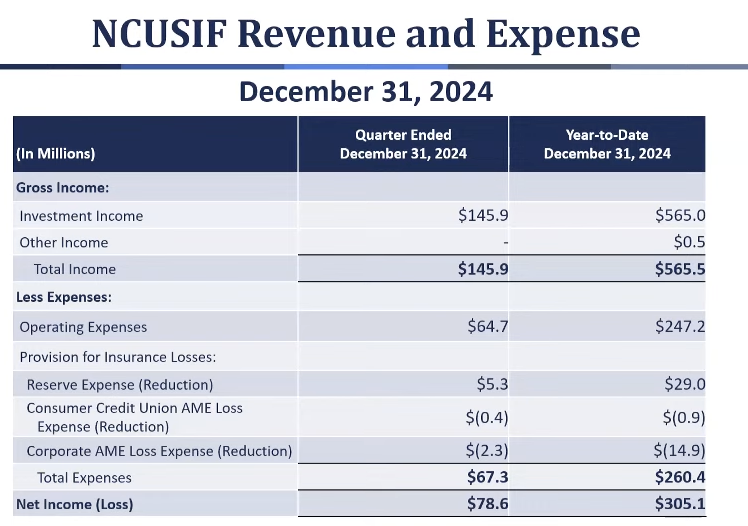

ALEXANDRIA, Va.–The NCUSIF posted $78.6-million during Q4 2024 and $305.1 million in net income for all of last year, shifts occurred among CAMELS 3, 4 and 5 CUs, and there were just three CU failures during 2024, according to a report given to the NCUA board meeting, where some of its members said the “good news” will only continue if the agency doesn’t experience cutbacks ordered by the White House.

The report on the health of the share insurance fund was given to the board by agency CFO Eugene Schied.

Schied reviewed various aspects of the NCUSIF’s performance in comments to the board the data that is shown in the slides below.

Worth Noting

Of particular note, according to Schied:

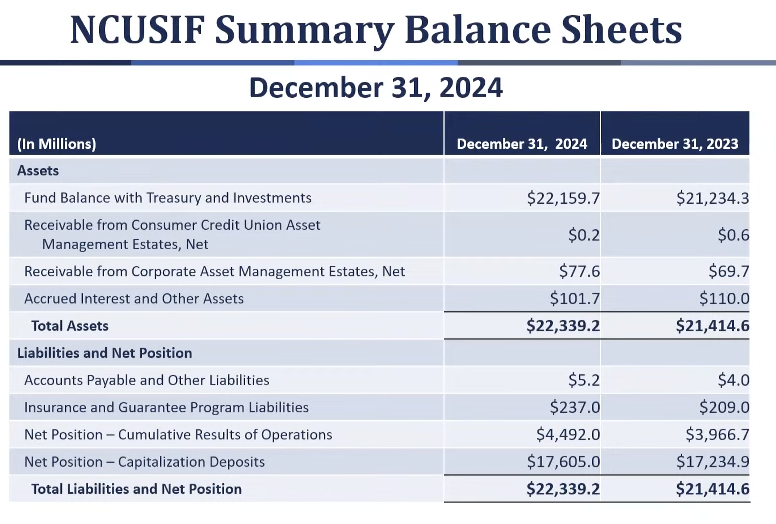

- Total NCUSIF assets were valued at $22.3 billion of which 99% were funds held with the U.S. Treasury.

- Total assets increased by $924.6 million for the year primarily due to a reduction in unrealized losses on Treasury investments, an increase in interest revenue and capitalization deposit adjustments for credit unions during the year.

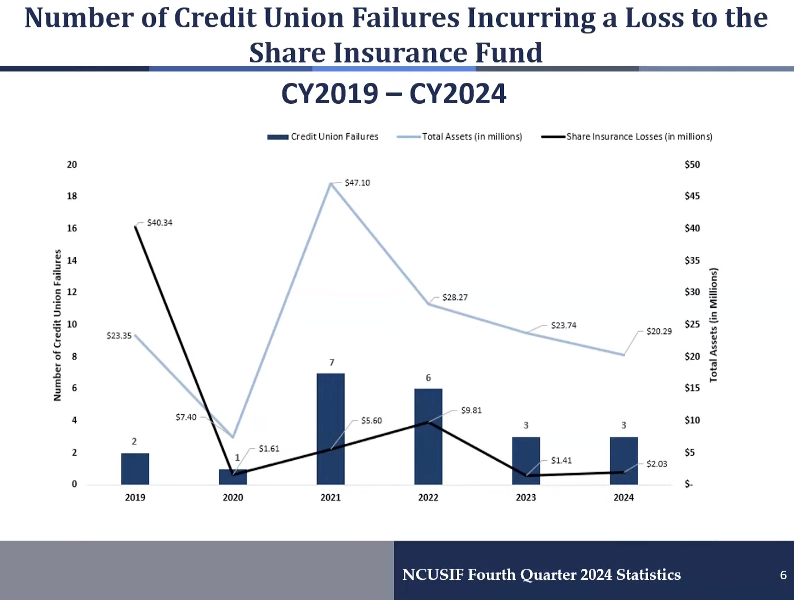

- There were three credit union failures during 2024 that causes losses to the insurance fund of $2.03 million. Fraud was not a factor in any of the losses.

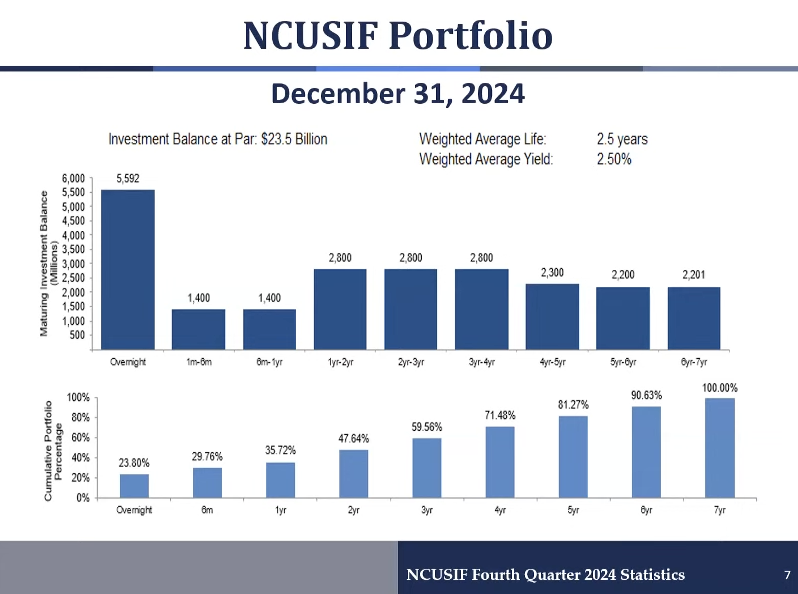

- During the fourth quarter of 2024 12 Treasury notes matured totaling $700 million. The securities had yields ranging from 0.26% to 2.34% and the proceeds have been reinvested at higher yields.

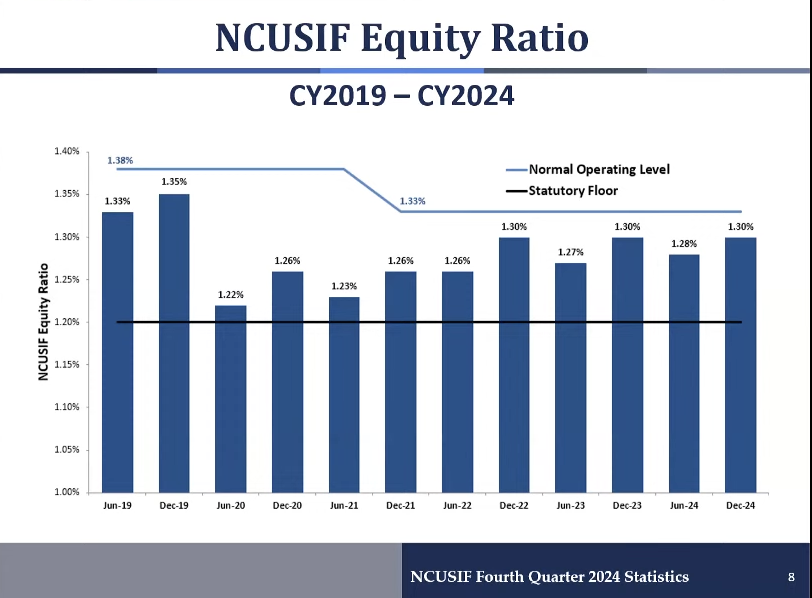

- The equity ratio of the fund remains 1.30%, where it has been for the past three years.

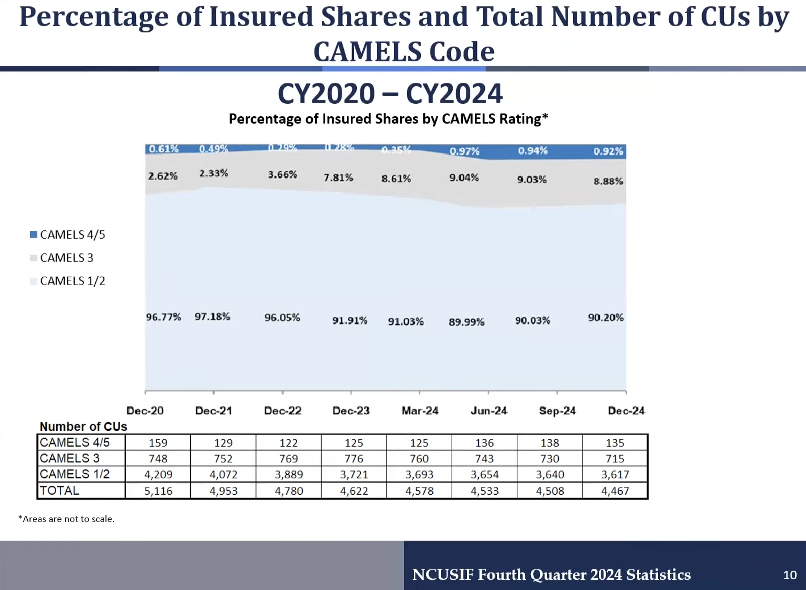

- The percentage of insured shares at credit unions CAMELS coded 3, 4 and 5 decreased slightly, while CAMELS coded 1 and 2 increased.

- The total number of federally insured credit unions as of Dec. 31st was 4467, a decrease of 41 credit unions from the prior quarter and a decrease of 155 for the year.

- Most CAMELS code 4 and 5 credit unions have assets below $150 million

Hauptman: A ‘Lot of Good News, But…’

In his comments following the report, NCUA Chairman Kyle Hauptman said there is a “lot of good news” in the report, including the 1.30 equity ratio, the slight increase in investment income, and other factors.

“And insured shares and assets in CAMELS code 3, 4, and 5 credit unions decreased slightly in the fourth quarter, said Hauptman. “We are not out of the woods, but that decrease is welcomed news as we saw increases in both categories over the last year. Yet, the number of failures for 2024 remained low with three credit union failures costing the Share Insurance Fund just over $2 million in losses. Again, all good news.”

Hauptman said NCUA will need to continue to monitor economic and market conditions, including potentially higher-than-expected inflation that could make the Fed less likely to lower the federal funds target rate.

Harper: Trends to Watch & More

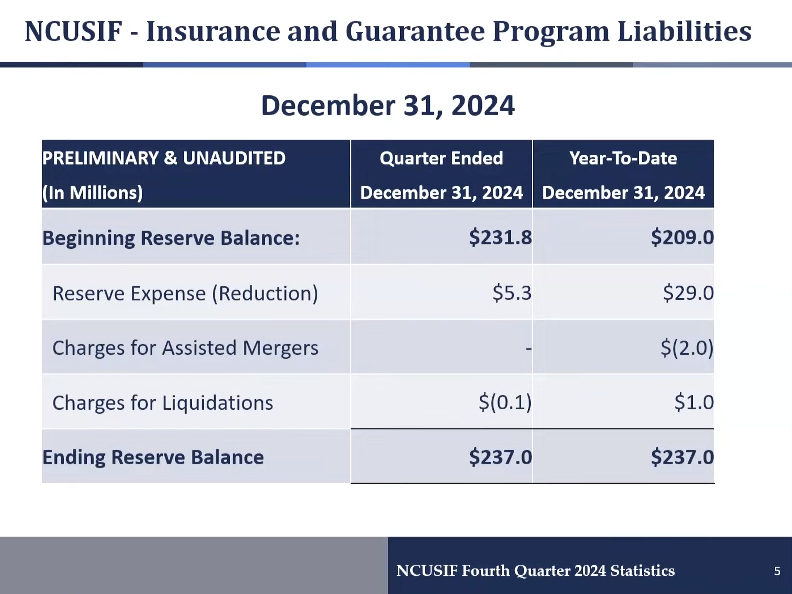

NCUA Board Member Todd Harper also cited the “good news” to be found in the numbers, but also cited downward trends in macroeconomic factors and composite CAMELS ratings that have also led to a $38 million increase in NCUSIF reserves.

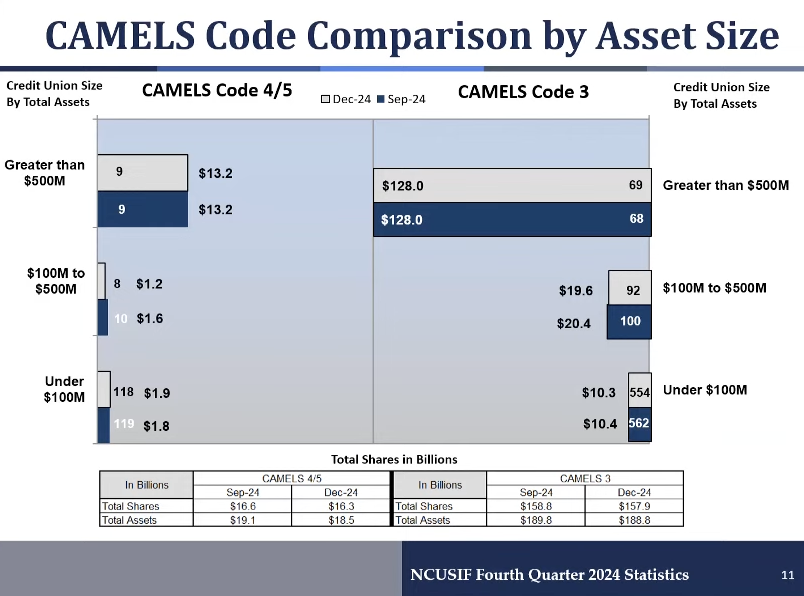

“What’s more, one year ago we had just two complex credit unions with $500 million or more in assets with composite CAMELS code 4 or 5 ratings,” Harper said. “But, as shown on slide 11, we now have nine complex credit unions with $13.2 billion in assets in this category. That’s $11.4 billion higher than one year ago.

“Moreover, the number of complex credit unions with a composite CAMELS code rating of 3 has also modestly grown over the last year. As a group, these credit unions have $128 billion in assets,” Harper continued. “Complex credit unions pose the greatest risks to the Share Insurance Fund. And, with 78 complex credit unions holding $141.2 billion in assets rated as a composite CAMELS code 3, 4, or 5, we must ensure that we have sufficient resources in place to prevent these institutions from causing losses in the future.”

Concerns for Agency

While not addressed specifically, there are concerns new White House directives will lead to layoffs at NCUA, with Harper stating, “We must recognize that if exam and supervision staffing levels are lowered, we may need to increase the Share Insurance Fund’s normal operating level to maintain sufficient reserves for potential losses. That’s because less frequent supervisory contacts, less comprehensive exams, and less oversight will likely lead to more credit union failures and increased Share Insurance Fund losses.

“Alternatively, we may need to alter our recordkeeping and reporting requirements to create a real-time monitoring system using innovative technology to identify risks,” Harper added. “Regardless of the path we choose, I am committed to working with my fellow board members to find the right balance to all these questions.”

Otsuka: Concern Over CAMEL 3 CUs

In her comments, NCUA Board Member Tanya Otsuka said she is worried about trends and growth among credit unions with CAMES Code 3 ratings, “especially as we see how new market stressors affect consumers and businesses across the country, So, we need to ensure that these credit unions are being properly managed and mitigating their various risks so their rapid growth doesn’t make problems worse.

“While the percentage of shares helping CAMELS 3 rated credit unions decreased slightly last quarter, it’s still at one of the highest levels we’ve seen since 2017,” Otsuka continued. “So, we need to watch out for that because it could pose a risk to the share insurance fund.”

The Future of NCUA

Like Harper, Otsuka also addressed concerns over what might lie ahead for NCUA.

“The ability to (monitor risk) depends on an independent agency and strong government workforce,” said Otsuka. “The independence of the NCUA is critical to maintaining confidence and stability in the credit union system and we cannot meet our statutory mandate without the NCAA staff across the country who faithfully execute their duties with integrity…”